Note: the Church Freedom and Corporation Sole Website has been removed and the links thereto are no longer valid.

Contents of this booklet (left click link to go to entry):

Chapter 1: Legal Entity Status and the Corporation Sole

Chapter 2: Analysis of “Benefits of the Corporation Sole Compared to a Traditional 501c3 Church” (Below)

Chapter 3: Analysis of “Church Establishment Affidavit”

Appendix A: What is a Corporation Sole?

Appendix B: Corporation Sole and Internal Revenue Code §§ 501(c)(3) and 508

Related articles:

- Expose And Reject The Teachings and Methods of Church Organization Con-Artists and Charlatans (050616)

- Why Understanding and Applying Church and State Law Is Important for Believers and Churches (June 3, 2012 article)

- See Comparison of Bible Trust (ordinary trust), Incorporation (includes corporation sole), and Ecclesiastical Law Center Trust for a concise chart of the differences each brings to church organization.

- A relevant and helpful article, as one who studies the above booklet out will see: Corporation: A human being without a soul

Jerald Finney

Copyright © February 2, 2015

For understanding, please read the Introduction and Chapter 1: Legal Entity Status and the Corporation Sole before studying this chapter.

This chapter will analyze the Benefits of the Corporation Sole Compared to a Traditional 501c3 Church webpage.

Quotations from the webpage Benefits of the Corporation Sole Compared to a Traditional 501c3 Church will be in red.

The analysis will be in the following order:

1. Analysis of the first sentence and the first paragraph

2. Analysis of Alleged Benefit # 1 – IT BRINGS RELIGIOUS FREEDOM OF SPEECH BACK TO THE CHURCH!

3. Analysis of Alleged Benefit #2 – Local Cities and Governments Can No Longer Impose Permits, Fines and Penalties to Churches for Helping Feed the Homeless

4. Analysis of Alleged Benefit # 3 – A Corporation Sole Requires NO BOARD OF TRUSTEE’S

5. Analysis of Alleged Benefit #4 – The Church Is Now MANDATORILY EXEMPTED From Both Taxation and Being Required to File Annual Information Return to the IRS

6. Analysis of Alleged Benefit #5 – NO BY-LAWS OR CHURCH CORPORATE CHARTER

7. Analysis of Alleged Benefit #6 – A CORPORATION SOLE CAN ISSUE PROMISSORY NOTES

8. Analysis of Alleged Benefit #7 – STATE TAX EXEMPTIONS

9. Analysis of Alleged Benefit #8 – TAX DEDUCTIBLE CONTRIBUTIONS

10. Analysis of Alleged Benefit #9 – TITLE TO REAL PROPERTY

11. Analysis of Alleged Benefit #10 – CLEAR LINE OF SUCCESSION

12. Analysis of Alleged Benefit #11 – DOES NOT REQUIRE AN ATTORNEY

13. Analysis of Alleged Benefit #12 – THE CORPORATION SOLE ACTS AS A NATURAL PERSON

1. Analysis of the first sentence and the first paragraph

The first sentence of Benefits of the Corporation Sole Compared to a Traditional 501c3 Church states:

“The benefits of the Corporation Sole are near limitless compared to every other form of a Church legally organizing itself.”

That sentence is revealing in so many ways to the knowledgeable believer. As one goes through this analysis, he will discover whether the language declaring the benefits to be limitless is accurate or false hyperbole.

First, that sentence is a clear recognition that the corporation sole organization is a legal entity which also organizes a church legally (makes the church a legal entity). As explained in the Introduction, a New Testament church cannot also be a church which is organized legally because this places the church under the authority of a head other than the Lord Jesus Christ; the legal entity status of the church makes the church a creature of the state. See also, Chapter 1: Legal Entity Status and the Corporation Sole for definition and implications of “legal entity.”

The New Testament teaches that, in order to be in God’s will, a church is to be a spiritual organism under God only; that Jesus Christ is to be her only head; that God is the highest power; and that we are to obey God rather than man when man’s law contradicts God’s law. All this is covered in some detail in The biblical doctrine of government, The biblical doctrine of the church, and The biblical doctrine of separation of church and state. Those who already agree with the Bible on this may wish to go directly to Separation of Church and State to get a quick review of what a church incorporation is. (See Incorporation of churches). Remember that the analysis of church incorporation, for the most part, can also be applied to the corporation sole church: the few differences will be obvious and both Oregon Non-Profit Corporation Law and the article being analyzed here make clear the differences.

Further down in the article, the author quotes the 2011 Oregon Revised Statutes, Oregon Non-profit Corporation Law, Volume 2 Business Organizations, Commercial Code § 65.067(1):

“Such corporation shall be a form of religious corporation and will differ from other such corporations organized hereunder only in that it shall have no board of directors, need not have officers and shall be managed by a single director who shall be the individual constituting the corporation and its incorporator or the successor of the incorporator.” – Oregon ORS § 65.067(1)

The article quotes the 2011 statute. Note that in 2013, the law was amended and can be accessed at the following link: 2013 Oregon Revised Statutes, Oregon Non-profit Corporation Law, Volume 2 Business Organizations, Commercial Code § 65.067.

The law itself makes clear that the only difference in the corporation sole and the corporation is that the corporation sole is headed by one man. Perhaps this will be of advantage to the pastor who believes that he should be an earthly dictator of a worldly or legal organization and and not a Bible ordained leader, steward, trustee, overseer, and under shepherd of a New Testament spiritual only church:

“Feed the flock of God which is among you, taking the oversight thereof, not by constraint, but willingly; not for filthy lucre, but of a ready mind; Neither as being lords over God’s heritage, but being ensamples to the flock. And when the chief Shepherd shall appear, ye shall receive a crown of glory that fadeth not away” (1 Peter 5:2-4).

After that first sentence, the article then states as it leads into alleged “Benefit # 1”:

“Let us explain each one of the benefits in great detail so you have a better understanding for how the Corporation Sole can bring legal deliverance to your ministry as a whole.”

Supposedly, according to the article, “the Corporation Sole can bring legal deliverance to your ministry as a whole.” Does it really? I thought the Lord Jesus Christ was the deliverer of the church. What about spiritual deliverance under God? How can a legal entity deliver God’s church?—I forgot, he said “deliverance to your ministry as a whole.” [Emphasis mine]. So by violating fundamental Bible principle for church organization “your ministry” can be delivered?

Notice, as you read the alleged benefits, that he gives no understanding under the so-called explanation as to “how the Corporation Sole can bring legal deliverance to your ministry as a whole.” He just says that it will do so.

2. Analysis of Alleged Benefit # 1

Then the article gets into the alleged Benefit #1 – IT BRINGS RELIGIOUS FREEDOM OF SPEECH BACK TO THE CHURCH!: One can go to the article Benefits of the Corporation Sole Compared to a Traditional 501c3 Church on the Church Freedom and the Corporation Sole website to read the alleged benefits. The corporation sole organization is the same as that of any other Oregon non-profit corporation except for very limited matters (see Oregon Revised Statutes, Chapter 2, Non-Profit Corporations.). Notice under that there is no explanation of “how” on the webpage, thus leaving several questions unanswered:

(1) How can the corporation sole bring religious freedom of speech back to the church since the corporate sole organization is to comply with all but a very few requirements of the extensive Oregon non-corporation law?

(2) How can the corporation sole bring religious freedom of speech back to the church since the corporate sole non-profit corporation renders the church a legal entity just as does any other non-profit corporate state law organization?

(3) In short, how can the corporation sole bring religious freedom of speech back to the church while at the same time putting the church under the state? (See Chapter 1: Legal Entity Status and the Corporation Sole), whereas a church which is not under state authority has all her First Amendment rights including freedom of speech.

The answer to all three questions is that the corporation sole cannot bring religious freedom of speech back to the church. It cannot do so because it takes religious freedom from a church.

Benefit number 1 is an impossibility. Nonetheless, the website, in the article, Church Establishment Affidavit, gives a ridiculous answer as to how the Corporate Sole form brings religious freedom of speech back to the church. That article states:

“The reason we emphasis that a Church must first be organized through an Church Establishment Affidavit, is because an Affidavit is the highest form of evidence a person can bring forth into a Federal courtroom. This allows your ministry to prove to the court, without a reasonable doubt, the distinct legal existence of your Church, its MANDATORY tax exemption jurisdiction under the law of 26 USC 508(c)(1)(a), creates a record that is signed under the penalties of perjury by multiple Church members and declares that your Church even adopts the IRS’s own 14 point standard to even be legally recognized as a Church! Its creation and use also allows the Church to create a legal and jurisdictional separation of responsibilities between the role of the Church itself and the isolated and incorporated office of the Corporation Sole (which the latter is under 501c3’s jurisdiction).”

As a sidenote, an Affidavit is not the highest form of evidence a person can bring forth into any courtroom (not just a Federal courtroom) in America. Live testimony is the highest form of evidence since it is subject to cross-examination and is judged by the trier of fact (the judge or the jury, as the case may be) as to its veracity. An affidavit is not acceptable evidence in a trial; only live testimony of a fact witness will be heard since the opposing side has the right to cross-examination, and it is impossible to cross-examine an affidavit. Disputes brought under the contracts created by incorporation, including corporation sole, will be heard in a courtroom in the state of incorporation.

Church Establishment Affidavit then continues with an “explanation” which is not an explanation at all, but a pure exercise in postmodernism. It is so ridiculous to the knowledgeable reader that it, as does the entirety of the website, completely discredits the “Church Freedom and the Corporation Sole” organization.

The above quoted paragraph from Church Establishment Affidavit, has many flaws, some repeated and addressed already in this analysis. The church establishes herself as a legal entity by legally executing the paperwork which created the contract between the church and the state of Oregon, the contract between the members of the church and the church, the contracts between the members themselves, and the contracts between the members and the state (See Separation of Church and State/God’s Churches: Spiritual or Legal Entities or Section VI of God Betrayed for an explanation of the law which makes this clear.). Furthermore, any church, no matter how organized, may claim 26 USC 508(c)(1)(a) tax exemption even though a New Testament church gives up her New Testament spiritual only status when she does so; the paragraph above from Church Establishment Affidavit does not explain that church 508 status brings the church under the rules that come with 501(c)(3). This is explained in detail in the article Church Internal Revenue Code § 508 Tax Exempt Status (Click link to go directly to that article.).

The creation and use of a corporation sole does not allow “the Church to create a legal and jurisdictional separation of responsibilities between the role of the Church itself and the isolated and incorporated office of the Corporation Sole.”

One church member handles all the corporate responsibilities of the corporation sole: the pastor, not several officers as in the case of other non-profit corporations which are created by the same law as the corporation sole. Remember that the corporation sole law is just part of the Oregon Non-Profit Corporation Statute. Remember Oregon Revised Statutes, Oregon Non-profit Corporation Law, Volume 2 Business Organizations, Commercial Code § 65.067(1), 2013 which reads, in relevant part:

“(1) An individual may, in conformity with the constitution, canons, rules, regulations and disciplines of a church or religious denomination, form a corporation under this section to be a corporation sole. The corporation sole is a form of religious corporation and differs from other religious corporations organized under this chapter only in that the corporation sole does not have a board of directors, does not need to have officers and is managed by a single director who is the individual who constitutes the corporation and is the corporation sole’s incorporator or the successor of the incorporator….”

Again, the church, as a legal entity, a non-profit corporation, created by the corporation sole law, is represented by one officer instead of several officers.

Go back and study Introduction and Chapter 1: Legal Entity Status and the Corporation Sole for clarification.

Furthermore, is one to believe that he can pick and choose the manners in which he is to violate God’s precepts? Is it OK with God for a church to submit herself to the state through non-profit corporation sole status, and then supposedly remove her submission to the state and submit herself to God by concocting, without understanding, a scheme which only purports to retain complete freedom when fact clearly shows that that corporation sole law which established the church as a legal entity gives the state who created her certain controls over her? Does the church want to retain their givers who give only if they get a tax deduction (not because they love the Lord) by falsely propping up this worthless scheme? Does a person lose their tax deduction for giving to a church who is totally under God as opposed to a church who is a non-profit corporation (which includes the corporation sole church)? Separation of Church and State/God’s Churches: Spiritual or Legal Entities and Section VI of God Betrayed explain these tax matters in some detail, including what the Internal Revenue Code says about the deductions.

3. Analysis of Alleged Benefit # 2

Now, let us examine supposed Benefit #2 – Local Cities and Governments Can No Longer Impose Permits, Fines and Penalties to Churches for Helping Feed the Homeless.

Again, this is so disjointed and full of false statements that it is very difficult to analyze. Of course, everyone knows that people will be moved when one alleges, against the truth, that his scheme will allow a church to help the homeless, an opportunity to gain sympathy for the deception.

“Lately, local City Governments across America have been treating traditional 501c3 incorporated Churches that feed the homeless no differently than any other corporate entity and have begun imposing sham taxes upon them in the form permits, fines and levies. The City Governments are able to accomplish this because of a little known Supreme Court ruling called Hale v. Henkle (1906) in which then US Supreme Court Chief Justice Melville Fuller stated that ALL incorporations (including incorporated Churches) are all considered to be, ‘Creatures of the State’.”

The corporation sole is a non-profit corporation under the law of the state of Oregon (in this case). Therefore, corporation sole organization will have no effect on the ability of the church to do these type of good deeds without meeting the requirements of law. (See Chapter 1: Legal Entity Status and the Corporation Sole. See the index of God Betrayed for Hale v. Hinkle.) As the article states, “ALL incorporations (including incorporated Churches) are all considered to be, ‘Creatures of the State’.” The corporation sole church is an incorporated church and a “creature of the state.” (Ibid.).

In the 1980’s the church I was saved in and a member of went downtown and fed the homeless for several years. The city tried to stop us by citing the pastor. The church was not incorporated as a non-profit corporation. Yet, after citing the pastor 80 or 100 times, the case finally went to trial and justice prevailed. The same result would have occurred had the church been a legal entity or not. The church was not charged with a crime, the pastor (who was leading the effort) was charged.

The article continues:

“Once a Church incorporates under 501c3, it instantly looses its Mandatory Tax Exemption status under the law of 26 U.S.C. 508(c)(1)(a) and opens itself to needless legal attack. Only a Church that has been properly established through both a Statutory Declaration Affidavit and a Corporation Sole are completely immune to these types of restrictions and impose taxes. The Church reformed with a Corporation Sole is now able to be completely immune from these type of penalties because it is no longer incorporated (nor considered a creature of the state) and is under the better law of 508(c)(1)(a) instead of 501c3. A Church that is under 508(c)(1)(a) is completely immune to ALL forms of state imposed taxation (this includes City permits to feed the homeless). Without a Corporation Sole, Churches across America are wide open to needlessly imposed taxes that they never had to experience in the first place!”

A church is not incorporated under 501c3. A corporation sole church is incorporated under state law, in this case Oregon Non-profit Corporation law. A church who applies for 501(c)(3) under federal law does not lose her 508(c)(1)(a) status. No church has 508(c)(1)(a) status unless she claims it; there are several ways in which churches can do this. By claiming 508 status, a church gives up her First Amendment only status. She does this by putting herself under a law as opposed to under the First Amendment. The First Amendment says, in relevant part: “Congress shall make no law respecting an establishment of religion or preventing the free exercise thereof.” 508 is a federal law respecting an establishment of religion and which prevents the free excercise thereof. When a church claims 508 status, she has put herself under a federal law, thereby revoking her First Amendment non-taxable status.

Applying for 501c3 tax exempt status and claiming 508 automatic exemption status affect the church in the same manner. Again, this is explained in the article Church Internal Revenue Code § 508 Tax Exempt Status.

The statement “The Church reformed with a Corporation Sole is now able to be completely immune from these type of penalties because it is no longer incorporated (nor considered a creature of the state) and is under the better law of 508(c)(1)(a) instead of 501c3” is utterly ridiculous, at best. Of course it is still incorporated and a creature of the state. The church applied to the state for non-profit corporation sole status as controlled by state law. And, as explained in preceding paragraphs and the linked to article, the 508 church must meet the same requirements as the 501c3 church in order to maintain her tax status.

4. Analysis of Alleged Benefit # 3

Examination of Benefit #3 – A Corporation Sole Requires NO BOARD OF TRUSTEE’S:

“Under the law of 501c3, the law states, “no part of the net earnings of which inures to the benefit of any private shareholder or individual” it is specifically due to this clause that EVERY Church in America organized under 501c3 has a polity body (aka a Board of Trustee’s, Board of Directors, Board of Elders and etc). The Corporation Sole is the ONLY EXCEPTION TO THIS RULE. In fact, States like Oregon fully recognize this difference and include it in their state law:

“Such corporation shall be a form of religious corporation and will differ from other such corporations organized hereunder only in that it shall have no board of directors, need not have officers and shall be managed by a single director who shall be the individual constituting the corporation and its incorporator or the successor of the incorporator.” – Oregon ORS § 65.067(1)

Of course, the phrase relied upon in the statute, “no part of the net earnings of which inures to the benefit of any private shareholder or individual” has nothing to do with establishing a “polity body (aka a Board of Trustee’s, Board of Directors, Board of Elders and etc.”) in a corporation. The corporation statute of the state of incorporation establishes a corporate “polity body” of corporations created thereunder. 501c3 was not enacted until 1954. The law of incorporation came long before that and provided for a Board of Trustee’s, Board of Directors, Board of Elders and etc. The Corporation Sole also has a long history, as pointed out on the website being examined at: The History of the Corporation Sole (I have not examined that article for accuracy, but the Corporation Sole does have a long history.). The clause in 501c3 had and has absolutely nothing to do with the body polity of any corporation including the corporation sole.

“This means that a Corporation Sole only has ONE director…the Senior Pastor or Overseer of the Church. Most do not understand how utterly significant this is and why it is such a blessing. You see, most of the headache for Pastors (among other things) is the fact that 501c3 forces Churches to have appropriation committees! It should not take a board to approve whether or not to provide the necessary funds the Church needs to fulfill the Holy Spirit led vision of the Senior Pastor. A Church that has a Corporation Sole does not have to deal with this issue. Now, certain individuals might raise the question, “How can you trust a Pastor with the finances of the Church?” Our reply is simple: The Lord Jesus says in Luke 16:10, “Whoever can be trusted with very little can also be trusted with much, and whoever is dishonest with very little will also be dishonest with much.” If you cannot trust your Pastor with $5, then you cannot trust them with $5 million and they do not need to be your Pastor or be a leader within the Body of Christ. For those Pastors that are Spirit led, this benefit of not having to go through a board, is a tremendous victory for the vision the Lord has laid on their heart. It cuts out any possible confusion and manipulation regarding the Churches finances.”

There is a correct way to establish the pastor as overseer of God’s money and property, and the correct way is not the establishment of any kind of church corporation including a corporation sole. This is explained in the my writings already cited.

5. Analysis of Alleged Benefit # 4

Alleged “benefit # 4” is so completely dishonest that it grieves not only the Lord, but also this author, to know that believers fall for this con.

Benefit #4 – The Church Is Now MANDATORILY EXEMPTED From Both Taxation and Being Required to File Annual Information Return to the IRS:

“Unlike a traditional 501c3 Church that has filed an IRS Form 1023 seeking their official recognition of their tax exemption status (and is mandatorily required to file their annual informational returns consecutively every three years or face an automatic revocation of their tax exemption status), A Church properly organized through the use of a Statutory Declaration Affidavit and a Corporation Sole are MANDATORILY exempted from BOTH taxation and being required to file their annual information returns. This is due to the Church now being properly established underneath the jurisdiction of two unique federal laws. First is the mandatory tax exemption law of 26 USC 508(c)(1)(a) which states,

“‘(a) New organizations must notify Secretary that they are applying for recognition of section 501(c)(3) status: Except as provided in subsection (c), an organization organized after October 9, 1969, SHALL NOT BE TREATED as an organization described in section 501(c)(3).’

“With key emphasis on the writing of the law that states, SHALL NOT BE TREATED as an organization described in section 501(c)(3).”

The above gives a portion of the law (IRC § 508, Subsection (a)), and then a few words from that portion of the law which is emphasized in the article by placing it in bold capital letters (“shall not be treated”). The article then gives that portion of the law, out of context, a false meaning. This is clear when the entirety of the relevant law is read. The entire relevant portion of section 508 (sections (a) through(c)) states:

“(a) New organizations must notify Secretary that they are applying for recognition of section 501(c)(3) status

“Except as provided in subsection (c), an organization organized after October 9, 1969, shall not be treated as an organization described in section 501 (c)(3)—

“(1) unless it has given notice to the Secretary in such manner as the Secretary may by regulations prescribe, that it is applying for recognition of such status, or

“(2) for any period before the giving of such notice, if such notice is given after the time prescribed by the Secretary by regulations for giving notice under this subsection.

“(b) Presumption that organizations are private foundations

“Except as provided in subsection (c), any organization (including an organization in existence on October 9, 1969) which is described in section 501 (c)(3) and which does not notify the Secretary, at such time and in such manner as the Secretary may by regulations prescribe, that it is not a private foundation shall be presumed to be a private foundation.

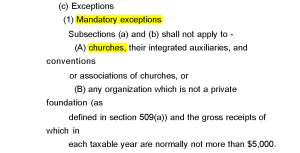

“(c) Exceptions

“(1) Mandatory exceptions

“Subsections (a) and (b) shall not apply to—

“(A) churches, their integrated auxiliaries, and conventions or associations of churches, or

“(B) any organization which is not a private foundation (as defined in section 509 (a)) and the gross receipts of which in each taxable year are normally not more than $5,000.”

–

Please notice the blatant dishonesty of the Church Freedom and the Corporation Sole website. They quote only a portion of the law and then take that portion out of context to mean something that it does not mean when taken in context. They leave out (a)(1) and (a)(2), and (c)(1)(A) which when taken together with (a), as they have to be to understand the true meaning. When the relevant sections are all considered, they make clear that churches are excepted from the (a) and (b) notice requirements of other non-church non-profit organizations.

Their ridiculous conclusion – “With key emphasis on the writing of the law that states, SHALL NOT BE TREATED as an organization described in section 501(c)(3)”- is also totally unfounded. Again, for an accurate understanding of 508 status, I urge the student to go to and study Church Internal Revenue Code § 508 Tax Exempt Status.

“Subsection (C) is for: churches, their integrated auxiliaries, and conventions or associations of churches. (source: Cornell Law)

“This means that the Church is immune to ALL forms of taxation. This includes cities that try to impose an excise tax on Churches for requiring them to obtain permits to feed the homeless and more. There are NO preconditions either (unlike 501c3’s political restrictions and conditions).”

More ridiculous statements. The quote from Subsection (c) does not mean that the church is immune to ALL forms of taxation. Subsection (c) deals with only the matters within its context. Yes, churches, no matter how organized, do not have to pay sales taxes, excise taxes, and other forms of taxes, but those matters are covered by state laws, not the Internal Revenue Code which is federal law.

The insanity continues:

The insanity continues:

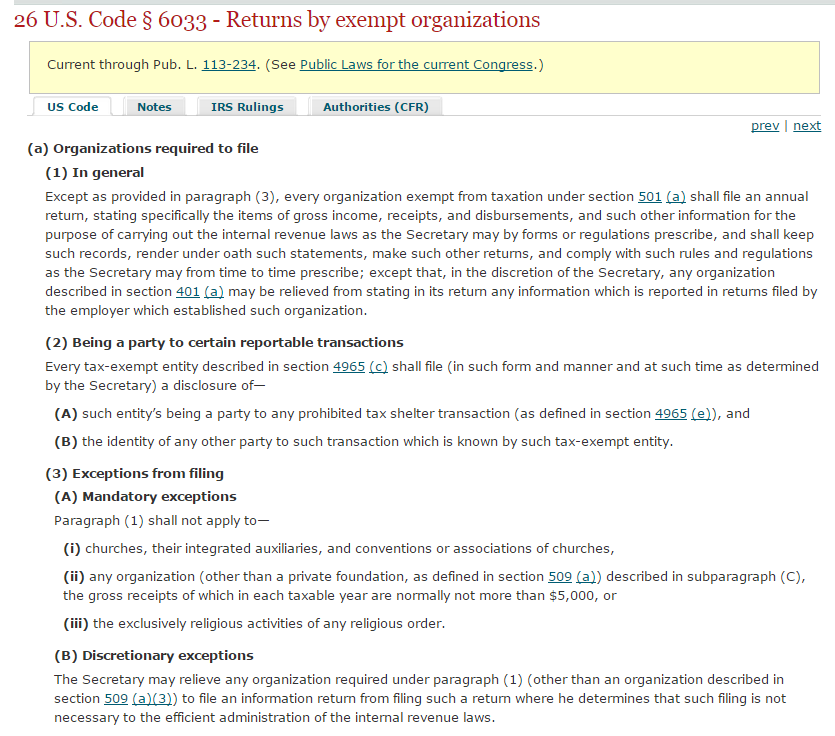

“The Church is also immune from FILING annual informational returns to the IRS. This is due to the Law of 26 USC 6033(c)(a)(1-3). This Federal law gives the Church and its subsequent Corporation Sole immunity for being required to file annual information returns. The law states,

“Except as provided in paragraph (3), every organization exempt from taxation under section 501 (a) shall file an annual return, stating specifically the items of gross income, receipts, and disbursements, and such other information for the purpose of carrying out the internal revenue laws as the Secretary may by forms or regulations prescribe, and shall keep such records, render under oath such statements, make such other returns, and comply with such rules and regulations as the Secretary may from time to time prescribe; except that, in the discretion of the Secretary, any organization described in section 401 (a) may be relieved from stating in its return any information which is reported in returns filed by the employer which established such organization.” – Source, Cornell Law University

“Parapgraph (3) excludes the following:|

“(3) Exceptions from filing

(A) MANDATORY EXCEPTIONS

Paragraph (1) shall not apply to—

(i) churches, their integrated auxiliaries, and conventions or associations of churches,

(ii) any organization (other than a private foundation, as defined in section 509 (a)) described in subparagraph (C), the gross receipts of which in each taxable year are normally not more than $5,000, or

(iii) the exclusively religious activities of any religious order.

“The church falls underneath the jurisdiction of subsection (i) while the Corporation Sole falls under the jurisdiction of subsection (iii) as it is operating and exclusively acting on the behalf of the religious order that manages the Churches assets.

“These are two ENORMOUS benefits that traditional 501c3 Churches do not get to enjoy.”

I cannot believe what I am reading. First, he gets the nomenclature of the statute wrong. He says 26 USC 6033(c)(a)(1-3) but the correct nomenclature is 26 USC 6033(a)(1-3), no big deal. However what follows in the above is a big deal. 26 USC 6033(a)(3)(i) clearly says that churches are mandatory exceptions to the filing requirement in 26 USC 6033(c)(a)(1). Thus churches, whether incorporated (corporations sole or otherwise) are subject to the same IRC rules and IRS regulations. “Traditional 501c3 churches” and corporation sole 508 churches do not have to file. Non-incorporated, non-501c3, non-508 churches (First Amendment) churches do not have to file (See Church Internal Revenue Code § 508 Tax Exempt Status for explanation.).

The statement which follows,

“The church falls underneath the jurisdiction of subsection (i) while the Corporation Sole falls under the jurisdiction of subsection (iii) as it is operating and exclusively acting on the behalf of the religious order that manages the Churches assets. These are two ENORMOUS benefits that traditional 501c3 Churches do not get to enjoy.”

is nonsensical, facetious, and false. The corporation sole is not a religious order that manages the churches assets. The law makes clear that the corporation sole is a non-profit corporation (a legal entity) and that corporation sole status makes a church a legal entity (Review, e.g., Chapter 1: Legal Entity Status and the Corporation Sole and Appendix A: What is a Corporation Sole for explanation). The above quote is saying that the law by which a church becomes a legal entity non-profit corporation for which the pastor acts as the only officer is magically transformed by the above ridiculous rhetoric. Obviously, the corporation sole church is in the same position as she would be in as any other non-profit corporation church as to these matters and the two alleged “ENORMOUS benefits” that “traditional 501c3 churches” do not get to enjoy are nonexistent.

6. Analysis of Alleged Benefit # 5

“Benefit #5 – NO BY-LAWS OR CHURCH CORPORATE CHARTER: Jesus was asked a question in Matthew 22:36-40 which states, “Teacher, which is the greatest commandment in the Law?” Jesus replied: “‘Love the Lord your God with all your heart and with all your soul and with all your mind.’ This is the first and greatest commandment. And the second is like it: ‘Love your neighbor as yourself.’ All the Law and the Prophets hang on these two commandments.”

“‘ALL the Law and the Prophets hang on these two commandments.’ -Yeshua Ha-Mashiach

“ALL other laws that govern the Church that have been made in addition to these two commandments are MAN MADE By-Laws and are NOT from the Holy Spirit. These man-made by-laws do nothing but show us someone else’s personal standard of holiness and serve to do nothing more than bring forth both condemnation and a spirit of religion. In fact, By-laws in there very nature defy the scriptures of both Romans 14:22 and Colossians 2:14-15! We’ve witnessed Churches here at The Empowerment Center that deny membership access to Christians because the husband drove a beer truck to provide income for his family! Not that he was drinking the beer, but simply because he DROVE THE TRUCK. By-Laws have directly influenced Churches across the nation to separate from the fellowship of all Christians and bring forth unnecessary doctrines. Certain denominational by-laws state that you MUST be baptized in water in order to be saved, while others claim that you need to be baptized in the fire of the Holy Spirit and speak in tongues! So, who is right and who is wrong? These By-Laws do NOTHING but create both confusion, disorder, separation and death to the fellowship (1 Timothy 1:4-7 and 2nd Timothy 2:14).

“One of the unique attributes of a Church that is properly established through both a Statutory Declaration of Church Establishment Affidavit and a Corporation Sole is that it requires absolutely no By-Laws whatsoever. In fact, the Statutory Declaration Affidavit we freely provide Church leaders is specifically written in such a manner where it lawfully fulfills ALL 14 points to the IRS’s own requirements to even be considered a Church! There are no additional needless by-laws that cause either separation nor condemnation. The Corporation Sole itself requires no by-laws whatsoever. We’ve took careful consideration to make sure that only the Statutory Declaration itself declares nothing more than the Office of the Corporation Sole’s status and the Corporation Sole’s intended successor and/or secretary’s positions and nothing more. This provides the Church will an unheard of level of freedom that other traditional 501c3 Churches do not presently have.”

The above is inaccurate. The law which the Church Freedom and the Corporation Sole utilizes to help churches organize as corporations sole, Oregon Revised Statutes, Oregon Non-profit Corporation Law, Volume 2 Business Organizations, Commercial Code § 65.067(1), 2013 states:

“65.067 Corporation sole. (1) An individual may, in conformity with the constitution, canons, rules, regulations and disciplines of a church or religious denomination, form a corporation under this section to be a corporation sole. The corporation sole is a form of religious corporation and differs from other religious corporations organized under this chapter only in that the corporation sole does not have a board of directors, does not need to have officers and is managed by a single director who is the individual who constitutes the corporation and is the corporation sole’s incorporator or the successor of the incorporator.

“(2) The name of the corporation sole is the same as the office within the church or religious denomination that the incorporator holds, followed by the words “and successors, a corporation sole.

“(3) All of the provisions of ORS 65.044 to 65.067 apply to a corporation sole. If the corporation sole has no officers, the director may perform any act that an officer may perform with the same effect and in the same manner as though one or more officers of the corporation sole performed the act.

“(4) If a corporation sole or the individual that constitutes the corporation sole is the only member of a religious corporation, the religious corporation is not required to hold an annual membership meeting under ORS 65.201 if the religious corporation is:

“(a) Incorporated under the provisions of this chapter; and

“(b) Of the same church or religious denomination as the corporation sole. [1989 c.1010 §27; 2013 c.139 §1]” [Bold emphasis which is mine is the portion relevant to this analysis.]

The bold portion of the law cited above makes clear that “All of the provisions of ORS 65.044 to 65.067 apply to a corporation sole.” Those sections are as follows:

65.044 Incorporators

65.047 Articles of incorporation

65.051 Incorporation

65.054 Liability for preincorporation transactions

65.057 Organization of corporation

65.061 Bylaws

65.064 Emergency bylaws and powers

65.067 Corporation sole

Section 65.061 which covers Bylaws states:

“(1) The incorporators or board of directors of a corporation, whichever completes the organization of the corporation at its organizational meeting, shall adopt initial bylaws for the corporation.

“(2) The bylaws may contain any provision for managing and regulating the affairs of the corporation that is not inconsistent with law or the articles of incorporation. [1989 c.1010 §25]”

Thus, to put it simply, law which creates the corporation sole clearly states that the corporation sole non-profit corporation “shall adopt initial bylaws for the corporation and that the bylaws may contain any provision for managing and regulating the affairs of the corporation that is not inconsistent with law or the articles of incorporation.”

Thus any church who adopts the corporation sole form of organization and who does not adopt bylaws is in violation of the law. The church violates the law because she becomes a legal entity by voluntarily seeking and obtaining corporation sole status. As a legal entity, she can sue, be sued, enter into contracts, etc. Again, she entered into a contract when she accepted the state non-profit corporation sole offer. (See Church Internal Revenue Code § 508 Tax Exempt Status for clarification.).

The response to the rant attributing various practices and doctrines of some “churches” to their bylaws is:

- a church who includes their beliefs in their by laws could also implement those practices and beliefs into the by laws required by corporation sole status or,

- should they not be incorporated in any way, into a church covenant, statement of faith, or written creed, or

- should they not be incorporated in any way, they could believe and practice their religion without any writing except the Bible.

Finally, a corporation sole cannot get around the law of incorporation above by using a Statutory Declaration of Church Establishment Affidavit. That is so obvious that to contend otherwise is patently absurd, as are other Church Freedom and Corporation Sole matters.

7. Analysis of Alleged Benefit # 6

Benefit #6 – A CORPORATION SOLE CAN ISSUE PROMISSORY NOTES: A Corporation Sole can issue promissory notes. A promissory note is a legal instrument (more particularly, a financial instrument), in which one party (the maker or issuer) promises in writing to pay a determinate sum of money to the other (the payee), either at a fixed or determinable future time or on demand of the payee, under specific terms. If the promissory note is unconditional and readily salable, it is called a negotiable instrument. – Source Wikipedia

Benefit #6 – A CORPORATION SOLE CAN ISSUE PROMISSORY NOTES: A Corporation Sole can issue promissory notes. A promissory note is a legal instrument (more particularly, a financial instrument), in which one party (the maker or issuer) promises in writing to pay a determinate sum of money to the other (the payee), either at a fixed or determinable future time or on demand of the payee, under specific terms. If the promissory note is unconditional and readily salable, it is called a negotiable instrument. – Source Wikipedia

The above is all that is said about this alleged benefit. One would suppose that the alleged benefit of this “legal instrument” for the corporation sole is to provide capital or to act as a source of finance to the creditors of the corporation sole. This author is not going to waste his time explaining all the ways in which this scheme violates New Testament church principle since any believer who has read his Bible should be able to figure this out.

8. Analysis of Alleged Benefit # 7

“Benefit #7 – STATE TAX EXEMPTIONS: A Corporation Sole is awarded ALL current state 501c3 tax exemptions. This can include property tax exemptions and more. Since the Corporation Sole is considered a 501c3 (because it is incorporated), it is qualified to seek any current state tax exemptions. It’s also important to note that even if you live in a state that does not have a current Corporation Sole (like here in Oregon) that you can still seek this exemption by having our Church, The Empowerment Center freely represent your Corporation Sole as a registered agent here in Oregon. In this case, your home state WILL fully recognize the tax exemption status of your Oregon based Corporation Sole (this is due to the commerce clause in the US Constitution). We’ve currently helped teach nearly 22,000+ Churches across America about the Corporation Sole and not a single Church has been denied an exemption from their home state.”

“Benefit #7 – STATE TAX EXEMPTIONS: A Corporation Sole is awarded ALL current state 501c3 tax exemptions. This can include property tax exemptions and more. Since the Corporation Sole is considered a 501c3 (because it is incorporated), it is qualified to seek any current state tax exemptions. It’s also important to note that even if you live in a state that does not have a current Corporation Sole (like here in Oregon) that you can still seek this exemption by having our Church, The Empowerment Center freely represent your Corporation Sole as a registered agent here in Oregon. In this case, your home state WILL fully recognize the tax exemption status of your Oregon based Corporation Sole (this is due to the commerce clause in the US Constitution). We’ve currently helped teach nearly 22,000+ Churches across America about the Corporation Sole and not a single Church has been denied an exemption from their home state.”

Property tax exemptions, sales tax exemptions, and what ever the “and more” tax exemptions are are all the product of state law. 501c3 is a federal law. 501c3 has nothing to do with state tax law provisions. Any church, whether a legal entity or not, is granted property tax exemptions “and more.” Churches who are not legal entities are granted such exemptions—this author has personal knowledge of this and knows of many churches who are not legal entities and who do not pay sales taxes, property taxes, etc.. Of course, an incorporated church such as a corporation sole church pays no such taxes. So this benefit is no benefit all. The Church Freedom and the Corporation Sole website does here recognize that the Corporation Sole “is considered a 501c3 because it is incorporated“), which contradicts teachings covered above which state that the corporation sole church is a IRC section 508 church.

9. Analysis of Alleged Benefit # 8

“Benefit #8 – TAX DEDUCTIBLE CONTRIBUTIONS: A Church that has a Corporation Sole CAN receive tax deductible contributions from any member that gives a gift. The Corporation Sole is also immune from being required by law to give the donor a receipt acknowledging their gift! In this case, it is the responsibility of the donor to keep their records and NOT the Church or Corporation Sole. If your Church chooses to do so, it may voluntarily and freely (out of the kindness of its heart) give the donor a receipt acknowledging their contribution or donation.”

No church has to give a receipt acknowledging their gift. The law requires no church to give an acknowledgement for gifts. If you disagree, I challenge you to show me that law – there is none. I deal with this issue often in discussing the right way for a church to organize according to the New Testament (and the right way is not any kind of non-profit corporation including the corporation sole.). The sad thing about this alleged benefit is that the corporation sole church has no reason not to give an acknowledgement since, if she claims 508 status, she is a legal entity who is subject to the rules of 501c3. See “5. Analysis of Alleged Benefit # 4” above, Corporation Sole and Internal Revenue Code §§ 501(c)(3) and 508, and Church Internal Revenue Code § 508 Tax Exempt Status.

10. Analysis of Alleged Benefit # 9

“Benefit #9 – TITLE TO REAL PROPERTY: Other Advantages of a Corporation Sole, it can claim title to real property. This is especially great for possible State Property Tax Exemptions.”

Any corporation, including any non-profit corporation such as a corporation sole, can buy and sell property. That is one of the attributes of being a legal entity. Since the corporation sole church becomes a legal entity by means of the corporation sole statute, the church is the legal owner of the property, although only one church member acts to fill all offices of the corporation sole.

11. Analysis of Alleged Benefit # 10

“Benefit #10 – CLEAR LINE OF SUCCESSION: Property and powers of a corporation sole are transferred on the death of an incumbent to successors in the office, “not to heirs or through executors”. This is especially nice for married couples that would like their spouse to continue leading their home based Church/Ministry. If the spouse in question is appointed the position of being the successor for the Corporation Sole, it is done through the unanimous consent of the entire Church and is lawfully declared through the Statutory Declaration of Church Establishment Affidavit. Currently, there is no Federal Law that prohibits this type of assignment within a Corporation Sole. This is due to the 1st Amendment to the Constitution which states the following:

“Congress shall make no law respecting an establishment of religion” – 1st Amendment to the United States Constitution (the Supreme Law of the Land).”

Let me first deal with the recitation of the First Amendment in this context. As any believer who understands the history of that Amendment knows, it came about as a result of 17 centuries of persecution (including hanging, burning at the stake, beheading, drowning, live burial, cruel torture) of martyrs who refused to profane God’s truths. This alleged benefit desecrates the holy as does this entire Church Freedom and the Corporation Sole website.

Church Freedom and the Corporation Sole website is here advising people to dishonor God’s precepts for the ordered church and also to use “religion” to protect their personal assets. People may declare themselves to be a “church” according to the 14 Internal Revenue Code criteria, but meeting the requirements of those criteria may be difficult for one who is just concocting a scheme to avoid probate law. Instead of keeping the church pure under God, as any believer who loves the Lord wants to do, this scheme uses man’s law to define their “church” and their motivation is to protect assets while dishonoring God.

Can anyone so motivated actually operate their “church” in conformity to Internal Revenue Code requirements? They may be called on the carpet by the IRS to prove that they have done so. Let’s look at those requirements. In attempting to define “church,” the IRS has “given certain characteristics [14 criteria] which are generally attributed to churches.” (S Publication 1828 (2007), p. 23) The court has recognized that 14-part test in determining whether a religious organization was a church. The 14 criteria are:

“(1) a distinct legal existence;

“(2) a recognized creed and form of worship;

“(3) a definite and distinct ecclesiastical government;

“(4) a formal code of doctrine and discipline;

“(5) a distinct religious history;

“(6) a membership not associated with any other church or denomination;

“(7) an organization of ordained ministers;

“(8) ordained ministers selected after completing prescribed studies;

“(9) a literature of its own;

“(10) established places of worship;

“(11) regular congregations;

“(12) regular religious services;

“(13) Sunday schools for religious instruction of the young;

“(14) schools for the preparation of its ministers.”

(American Guidance Foundation, Inc. v. United States, 490 F. Supp. 304 (D.D.C. 1980)).

“In addition to the 14 criteria enumerated above, the IRS will consider ‘[a]ny other facts and circumstances which may bear upon the organization’s claim for church status.’ Internal Revenue Manual 7(10)69, Exempt Organizations Examination Guidelines Handbook 321.3(3) (Apr. 5, 1982).” (88 T.C. at 1358).

Again, another alleged benefit profanes the holy, and actually testing this benefit may result in bad IRS consequences.

12. Analysis of Alleged Benefit # 11

“Benefit #11 – DOES NOT REQUIRE AN ATTORNEY: A Corporate Sole can Sue and be sued, and defend, in all courts, and places, in all matters and proceedings wherever. It represents itself because it acts and behaves as a Natural Person.”

They give the attributes of any legal entity, including those of a corporation sole which is a non-profit corporation.

Who will represent the corporation sole? The pastor, as the one officer? One of the church members?

Anyone can represent themselves in court. However, a person cannot represent another person in court. Furthermore, legal matters can be very complicated substantively and procedurally. The old adage “he who represents himself in court has a fool for a client” should be considered.

13, Analysis of Alleged Benefit # 12

“Benefit #12 – THE CORPORATION SOLE ACTS AS A NATURAL PERSON: A Corporation Sole is recognized by the IRS as a Natural Person in ALL business related transactions for the Church. A Natural person is legally defined pursuant to the United States Supreme Court ruling of Hale v Henkle in which former United States Supreme Court Chief Justice Melville Fuller states,

“‘The individual may stand upon his constitutional Rights as a citizen. He is entitled to carry on his private business in his own way. His power to contract is unlimited. He owes no such duty [to submit his books and papers for an examination] to the State, since he receives nothing therefrom, beyond the protection of his life and property. His Rights are such as existed by the law of the land [Common Law] long antecedent to the organization of the State, and can only be taken from him by due process of law, and in accordance with the Constitution. Among his Rights are a refusal to incriminate himself, and the immunity of himself and his property from arrest or seizure except under a warrant of the law. He owes nothing to the public so long as he does not trespass upon their Rights.” – United States Supreme Court Chief Justice Melville Fuller’

I must interject a comment here. The above Church Freedom and the Corporation Sole website leaves out the first sentence of the above quote from Have v. Henkle. I quoted the entire paragraph in God Betrayed in 2008, which is reproduced below. The first sentence says, “[T]here is a clear distinction in this particular between an individual and a corporation, and that the latter has no right to refuse to submit its books and papers for an examination at the suit of the State.”

“Its also important to note that a ‘Natural Person” is legally defined by Blacks Law Dictionary as,

“A “natural person” and an “individual” are defined by Blacks Law Dictionary 9th Edition as:

“Person (Be) 1. A human being. Also termed natural person.

“Individual, adj. (I5c) 1. Existing as an indivisible entity. 2. For relating to a single person or thing, as opposed to a group. – Blacks Law Dictionary 9th Edition

“There is a possible legal argument to be made that even though a Corporation Sole is registered with a Secretary of State as a corporation, that it in fact has the same rights as individual rights, which supersede corporate law. It is the only known corporation in American law to do this. It is also important to note that this argument has not been used in Federal Court as a defense (because they have not thought to do so).”

The legal argument proposed in the last paragraph would be laughed out of court. This has already been settled. I covered this in God Betrayed/Separation of Church and State: The Biblical Principles and the American Application (2008)(Click here to go to the online PDF of the book.). The following is from pages 375-376 of that book.

The incorporated church [such as a non-profit corporation sole church] is an artificial person and a separate legal entity. This has many ramifications.

- “The corporate personality is a fiction but is intended to be acted upon as though it were a fact. A corporation is a separate legal entity, distinct from its individual members or stockholders.

- “The basic purpose of incorporation is to create a distinct legal entity, with legal rights, obligations, powers, and privileges different from those of the natural individuals who created it, own it, or whom it employs….

- “A corporate owner/employee, who is a natural person, is distinct, therefore, from the corporation itself. An employee and the corporation for which the employee works are different persons, even where the employee is the corporation’s sole owner…. The corporation also remains unchanged and unaffected in its identity by changes in its individual membership.

- “In no legal sense can the business of a corporation be said to be that of its individual stockholders or officers.”

(18 AM. JUR. 2D Corporations § 44 (2007)).

“A corporation is a person within the meaning of the due process and equal protection clauses of the Fourteenth Amendment to the United States Constitution and similar provisions of state constitutions and within the meaning of state statutes.” (Johnson v. Goodyear, 127 Cal. 4 (1899). “However, a corporation is not considered as a person under the First Amendment to the United States Constitution (religious liberty clause) or under the Fifth Amendment to the United States Constitution.”

Hale v. Hinkle, 201 U.S. 43, 74-75; 26 S. Ct. 370; 50 L. Ed. 652; 1906 U.S. LEXIS 1815 (1906) stated:

- “[T]here is a clear distinction in this particular between an individual and a corporation, and that the latter has no right to refuse to submit its books and papers for an examination at the suit of the State. The individual may stand upon his constitutional rights as a citizen. He is entitled to carry on his private business in his own way. His power to contract is unlimited. He owes no duty to the State or to his neighbors to divulge his business, or to open his doors to an investigation, so far as it may tend to criminate him. He owes no such duty to the State, since he receives nothing therefrom, beyond the protection of his life and property. His rights are such as existed by the law of the land long antecedent to the organization of the State, and can only be taken from him by due process of law, and in accordance with the Constitution. Among his rights are a refusal to incriminate himself, and the immunity of himself and his property from arrest or seizure except under a warrant of the law. He owes nothing to the public so long as he does not trespass upon their rights.

- “Upon the other hand, the corporation is a creature of the State. It is presumed to be incorporated for the benefit of the public. It receives certain special privileges and franchises, and holds them subject to the laws of the State and the limitations of its charter. Its powers are limited by law. It can make no contract not authorized by its charter. Its rights to act as a corporation are only preserved to it so long as it obeys the laws of its creation. There is a reserved right in the legislature to investigate its contracts and find out whether it has exceeded its powers. It would be a strange anomaly to hold that a State, having chartered a corporation to make use of certain franchises, could not in the exercise of its sovereignty inquire how these franchises had been employed, and whether they had been abused, and demand the production of the corporate books and papers for that purpose.”

When a church incorporates or becomes a legal entity, that church contracts with the state gaining certain “protections” but gives up certain constitutional rights. She takes herself partially out from under First Amendment protection, and puts herself, for some purposes, under the Fourteenth Amendment. While a corporation must “obey the laws of its creation,” it also has constitutionally protected rights. (See Ibid., pp. 74-75). Only the church who is not satisfied with the freedom and provisions afforded the church by God (which, by the way, are implemented by the First Amendment) seeks incorporation. For the incorporated church, God’s provisions are not adequate. Although perhaps the individual church member seeks incorporation for protection by civil government as opposed to protection by God, that member forgets that God is a far more strong and benevolent protector than the state. Furthermore, when a church is not a legal entity, that church cannot be sued. One can sue a legal entity such as a corporation, but how does one sue a church who is “a spiritual house made up of spiritual beings offering up spiritual sacrifices, and not a physical house made by man?” (See Section II of God Betrayed). Individuals, including members of a New Testament church, can be sued for tortious actions or tried for criminal acts, but a New Testament church cannot be sued or tried for criminal acts.

End