As shown in Appendix A, a corporation sole church is a non-profit corporation, a creature of the state. Let us look at the 501(c)(3) ramifications of this.

Internal Revenue Code Section 501(c)(3). Click image above to go directly to 501(c)(3)

An organization described in subsection (c) or (d) or section 401(a) shall be exempt from taxation under this subtitle unless such exemption is denied under section 502 or 503.

…

“(c)List of exempt organizations

The following organizations are referred to in subsection (a):

…

“(3)Corporations, and any community chest, fund, or foundation, organized and operated exclusively for religious, charitable, scientific, testing for public safety, literary, or educational purposes, or to foster national or international amateur sports competition (but only if no part of its activities involve the provision of athletic facilities or equipment), or for the prevention of cruelty to children or animals, no part of the net earnings of which inures to the benefit of any private shareholder or individual, no substantial part of the activities of which is carrying on propaganda, or otherwise attempting, to influence legislation (except as otherwise provided in subsection (h)), and which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public office.”

Thus, according toInternal Revenue Code § 501(c)(3), corporations are exempt from taxation. A corporation sole is a corporation and therefore may apply for 501(c)(3) tax exempt status. (See Appendix A.).

Some corporation sole churches do not like the rules that go with 501(c)(3) status. Therefore, they make the argument that, since they are not corporations, they may obtain Internal Revenue Code § 508(c)(1)(A) status, become automatically exempt, and not be subject to the rules that come with 501(c)(3). Their arguments are untenable because they are non-profit corporations. Yes, they, like any other church, may claim § 508 status; yes, they may become exempt under § 508; no, they, as § 508(c)(1)(A) churches, do not avoid the 501(c)(3) rules thereby. § 508(c)(1)(A) churches are subject to 501(c)(3) rules.

Corporation sole churches know that they may have to go to court to defend their position. This is an admission that they are legal entities who are under the authority of the state of incorporation and the federal government as to Internal Revenue Code matters. Whether they admit this or not, it is a fact established when they accepted the state’s offer for state, non-profit corporation status and when they claim § 508 status. Since they are legal entities, creatures of the state, their only challenge to rules they do not like is through action in state or federal court. Should they be taken to court, for example by the Internal Revenue Service, they have agreed that the state is the final judge of the issue being litigated.

The issue is one of authority. Those who love the Lord are willing to give their all if necessary as they refuse to follow lower laws when those laws conflict with the highest law. Millions of martyrs have followed the example of the apostles who said, when the authority of the Lord Jesus Christ was at issue, “We ought to obey God rather than men” (Acts 5:29).

Internal Revenue Code Section 508. Click image above to go directly to 508.

Some corporation sole churches try to argue that they are not corporations and therefore that they may claim Internal Revenue Code § 508(c)(1)(A) status which insulates them from following the requirements of 501(c)(3). They do not mind being a creature of the state under the corporation sole law, but they try to avoid being under the rules that come with 501(c)(3). What they are trying to do is attain government approved tax exempt status (as opposed to First Amendment non-taxable status) without submitting to the rules of 501(c)(3). They do not mind the fact that they are not organized according to God’s rules in the New Testament and that they are a creature of the state of incorporation. They wish to twist the law in order to get what they falsely perceive to be benefits without the rules that come with the “benefits.” Their effort is not according to knowledge. The IRS has already covered this matter. 508 churches are held to be subject to the rules that come with 501(c)(3). (See Church Internal Revenue Code § 508 Tax Exempt Status for a full explanation).

Many non-profit corporation churches claim 501(c)(3) status without filing Internal Revenue Service form 1023. They do so in various ways One way is to include the provisions of 501(c)(3) in their corporate constitutions. Another is to simply acknowledge the exemption by giving acknowledgement to those who give. Even should a church not give acknowledgement, in the event of taxpayer audit, what the IRS wants to know is “what was given,” “did the taxpayer give in a manner prescribed by the IRS Code,” and “was the deduction given to a church (whether a legal entity or not.)”.

Corporation sole churches who try to twist the law to keep their deductible status while avoiding the rules that go with exempt status show their true colors to God and to those who take the time to examine what they are doing. Perhaps they act and speak ignorantly because of lack of both Bible and legal study which renders the subject outside their field of expertise.

What is a corporation sole? Who creates the corporation sole? The creator of the corporation sole defines its creation, just as God defines that which He creates, ordains, or establishes. The corporation sole is a creation of state law.

Just as human beings are creatures of God, so corporations sole are creatures of the state. The proof?—the Oregon corporation sole statutes (reproduced below) which allow churches to accept the state of Oregon’s offer to churches to place themselves under state law and become corporations sole. Those statutes make clear that the corporation sole is a non-profit corporation which is under the law which creates it. Keep in mind that a few other states also create corporations sole.

After studying this analysis, one who is heretofore unfamiliar with delving into this issue will be prepared to examine the corporation sole statutes of other states.

“(1) An individual may, in conformity with the constitution, canons, rules, regulations and disciplines of a church or religious denomination, form a corporation under this section to be a corporation sole. The corporation sole is a form of religious corporation and differs from other religious corporations organized under this chapter only in that the corporation sole does not have a board of directors, does not need to have officers and is managed by a single director who is the individual who constitutes the corporation and is the corporation sole’s incorporator or the successor of the incorporator.

“2) The name of the corporation sole is the same as the office within the church or religious denomination that the incorporator holds, followed by the words ‘and successors, a corporation sole.’

“(3) All of the provisions of ORS 65.044 to 65.067 apply to a corporation sole. If the corporation sole has no officers, the director may perform any act that an officer may perform with the same effect and in the same manner as though one or more officers of the corporation sole performed the act.

“(4) If a corporation sole or the individual that constitutes the corporation sole is the only member of a religious corporation, the religious corporation is not required to hold an annual membership meeting under ORS 65.201 if the religious corporation is: (a) Incorporated under the provisions of this chapter; and (b) Of the same church or religious denomination as the corporation sole.

“Approved by the Governor May 16, 2013 Filed in the office of Secretary of State May 17, 2013 Effective date January 1, 2014.”

Notice the first sentence of the above statute: “An individual may, in conformity with the constitution, canons, rules, regulations and disciplines of a church or religious denomination, form a corporation under this section to be a corporation sole.” A church may, as in the case of all non-profit corporation laws in America, form what? A corporation. The law says an individual “may form a corporation … under this section to be a corporation sole.” [Empahsis mine.] Under what? Under this section of the law, not under God. In conformity to what?–In comformity to the “constitution, canons, rules, regulations of a church or religious denomination;” not in conformity to Bible principle. A church corporation sole may be in conformity to the “constitution, canons, rules, regulations of a church or religious denomination” but it is not in conformity to New Testament church guidelines.

The next sentence says: “The corporation sole is a form of religious corporation and differs from other religious corporations organized under this chapter only in that the corporation sole does not have a board of directors, does not need to have officers and is managed by a single director who is the individual who constitutes the corporation and is the corporation sole’s incorporator or the successor of the incorporator.”

Because a church may form a corporation sole under the statute, the state is only extending an offer which a church may accept. If the church accepts the offer, she has entered into a contract with the state.

The basic components of a contract are offer, acceptance, and consideration. Consideration means that each party to the contract must receive a benefit. The state receives a benefit—control over the accepting church to the degree laid out in the statute. The accepting church believes that she receives a benefit—the contractual protections she perceives she gets from the law of contract. Never mind that she is no longer under the Lord Jesus Christ only—His power, principles, laws, judgment, and benefits are not enough for the corporate church. In fact, some of the laws of the state are deemed to be superior to the laws of God; this must be the case because the corporate church agrees to enter into a contract forbidden by the New Testament principles and many of whose conditions directly contradict those principles. Corporation sole churches and all other corporate churches should thank the Lord for his permissive will since they are no longer in His perfect will.

All law has a hierarchy (a line of authority). The authority of a given law depends upon its place in the hierarchy. For example, God’s law is the highest law. In America, the next highest law is the United States Constitution. Below that are state, county, and city, constitutions and laws, in that order. Oregon Revised Statutes,Oregon Non-profit Corporation Law, Volume 2 Business Organizations, Commercial Code§ 65.067, 2013 is not the highest law of the State of Oregon. It falls below the Oregon Constitution, United States Constitution, all of which are under God’s law. One can challenge a lower law in the United States Federal or in the Oregon courts should he believe it is unconstitutional. Of course, as applied to churches, Oregon Revised Statutes,Oregon Non-profit Corporation Law, Volume 2 Business Organizations, Commercial Code§ 65.067, 2013 violates God’s law. It also violates man’s law, the First Amendment, which is a statement of the Bible principle of separation of church and state. (See Is Separation of Church and State Found in the Constitution? and the resources cited in that article.). Instead of not accepting the state’s offer and perhaps challenging the statute on First Amendment grounds, many churches choose to accept the offer the state’s offer.

What about appealing the lawfulness of this Oregon law to the Judge of the Universe? That judge, since He knows all things, created all things, and ordained all lawful powers, does not hold court in a secular manner. He operates outside of time and outside man’s temporal procedures. He weighs all the facts and judges from His throne. In some ways, churches suffer the natural, God-ordained consequences for violation of His laws. Sometimes, God decides to judge in the here and now through temporal means. Sometimes He reserves judgment for the final judgment day.

Although the Oregon Corporation Sole church is a non-profit corporation, she is distinct from in some ways and the same as in some ways to other Oregon non-profit corporations. The law explains how she is distinct and how she is the same. The law says in Section (1):

“… The corporation sole … differs from other religious corporations organized under this chapter only in that the corporation sole does not have a board of directors, does not need to have officers and is managed by a single director who is the individual who constitutes the corporation and is the corporation sole’s incorporator or the successor of the incorporator.” [Emphasis mine.]

That is the only difference which is repeated here for emphasis—the Oregon corporation sole “does not have a board of directors, does not need to have officers and managed by a single director who is the individual who constitutes the corporation and is the corporation sole’s incorporator or the successor of the incorporator.< Section (2) applies to the name of the corporation sole.

Section (3) tells how the corporation sole is the same as other Oregon non-profit corporations: “(3) All of the provisions of ORS 65.044 to 65.067 apply to a corporation sole.” This shows that the Oregon corporation sole is a non-profit corporation and that “All of the provisions of ORS 65.044 to 65.067” apply to her.

What are those provisions? The titles are as follows:

65.044 Incorporators

65.047 Articles of incorporation

65.051 Incorporation

65.054 Liability for preincorporation transactions

65.057 Organization of corporation

65.061 Bylaws

65.064 Emergency bylaws and powers

65.067 Corporation sole

Section (3) also explains the function of the director of the corporation sole:

“If the corporation sole has no officers, the director may perform any act that an officer may perform with the same effect and in the same manner as though one or more officers of the corporation sole performed the act.””

Click to go directly to Church Establishment Affidavit Page

1. Analysis of the first two paragraphs 2. Analysis of section 1, “THE JURISDICTIONAL DISTINCTION AND DIFFERENCES BETWEEN THE LAWS OF 508C1A AND 501C3 IN THEIR RELATIONSHIP TO A CHURCH ESTABLISHMENT AFFIDAVIT” 3. Analysis of section 2 “WHY OUR CHURCH ESTABLISHMENT AFFIDAVIT IS SO IMPORTANT TO CHURCHES” 4. Analysis of “DOES THE GOVERNMENT OR IRS REALLY WANT THIS FIGHT?”

“When getting a Corporation Sole for your Church and Ministry, it is important to note that your actually creating two separate legal creatures. First, you create your Church (which is legally manifested through a Church Establishment Affidavit) and then the Churches subsequent Corporation Sole (which is nothing more than an incorporated office held within the Church for the purposes of managing all of the Churches assets and is NOT the Church itself).”

My comments. Yes, you are creating two legal creatures, but they are not separate which is made clear by the law and by the paragraph quoted above. Notice that he says, “Corporation Sole (which is nothing more than an incorporated office held within the Church for the purposes of managing all of the Churches assets and is NOT the Church itself). The incorporated sole office is held within the church for the purpose of managing all of the Church’s assets. It is also an office created by the corporation sole contract with the state, Oregon in this case. The Bible mentions no such office for a New Testament church. A church under God will comply with New Testament guidelines for the church. A church under the state, created by men, such as the church created by a Church Establishment Affidavit, will concoct its own manner of organization. Some will then publish that method and deceive others such that they contribute monetarily (of course, they are not required to donate) to the deceivers who help them profane God’s church through devices such as non-profit corporation sole and Church Establishment Affidavit which, among other things, defines the church according to the IRS defintion of a church.

“A Corporation Sole CANNOT be established unless your Church is first created through the use of a Church Establishment Affidavit that needs to be signed by both you as the Pastor of the Church but also two Church member witnesses and your Churches eventual Corporation Sole’s Successor and/or Secretary. If a Corporation Sole were to be established prior to you signing, witnessing and having notarized the Church Affidavit, then your Corporation Sole can be out of statutory compliance and potentially deemed a sham organization by the IRS.”

This man, Joshua Kenny-Greenwood, Overseer of The Empowerment Center Church, just makes stuff up, as I have pointed out over and over in this booklet. Hundreds of thousands of churches alone have been established under God, in Bible order, without a church establishment affidavit. Sadly, most American churches chose, against the will of God according to His word, to become legal entities such as non-profit corporations (which, as explained in prior chapters, includes the corporation sole non-profit corporation), unincorporated associations, charitable trusts, and business trusts; the vast majority of those went on to become 501(c)(3) churches. There is a significant remnant of churches in America who are doing things God’s way.

“The reason we emphasis that a Church must first be organized through an Church Establishment Affidavit, is because an Affidavit is the highest form of evidence a person can bring forth into a Federal courtroom. This allows your ministry to prove to the court,without a reasonable doubt, the distinct legal existence of your Church, its MANDATORY tax exemption jurisdiction under the law of 26 USC 508(c)(1)(a), creates a record that is signed under the penalties of perjury by multiple Church members and declares that your Church even adopts the IRS’s own 14 point standard to even be legally recognized as a Church! Its creation and use also allows the Church to create a legal and jurisdictional separation of responsibilities between the role of the Church itself and the isolated and incorporated office of the Corporation Sole (which the latter is under 501c3’s jurisdiction).”

Click to go directly to code.

Should the IRS target a church which is a legal entity, such as a corporation sole church, for some reason, the church will have to first go through the agency process, perhaps a hearing. The IRS Code § 7611 covers church tax inquiries and examinations. § 7611 says:

IRS personnel must observe the restrictions imposed by IRC § 7611 in any inquiry or examination of a church. Such inquiry or examination must be limited to determining whether:

The organization is exempt from tax under IRC § 501(a),

The organization is a church under IRC §§ 509(a)(1) and 170(b)(1)(A)(i),

The church is carrying on an unrelated trade or business as defined in IRC § 513,

The church is otherwise engaged in activities subject to federal tax, or

The church has engaged in an excess benefit transaction (See procedures in IRM 7.27.30.8).

The term “church” includes

Any organization claiming to be a church. However, see ,IRM 4.76.7.4.2(4), and

Any convention or association of churches.

Should the IRS begin an inquiry and examination of a corporation sole church, or any other church which is a legal entity, they must abide by § 7611. Should the church lose in the agency process, she can appeal to Federal Court. Affidavits are not acceptable evidence in many agency and court proceedings. Generally, the adversary has the right to cross-examination. If a trial is required, affidavits will not be accepted. Witness evidence under oath and subject to cross-examination is the highest form of evidence and witness evidence will be required. Even should a church corporation sole be supported by affidavit, an affidavit is not subject to cross-examination and the IRS can subpoena the signers of the affidavit and place them under cross-examination. Since the signers have already displayed their ignorance by falling for the corporation sole scheme, they most assuredly would not look good under cross-examination by an experienced and studied government attorney. The IRS can also bring in other witnesses. See § 7611 for the areas the IRS can inquire into.

2. Analysis of section 1, “THE JURISDICTIONAL DISTINCTION AND DIFFERENCES BETWEEN THE LAWS OF 508C1A AND 501C3 IN THEIR RELATIONSHIP TO A CHURCH ESTABLISHMENT AFFIDAVIT”

This section is like the writing on this entire website, a disgrace in the eyes of man and God. It is similar to a written Frankenstein in that its author, Joshua Kenny-Greenwood, grabs quotes from all kinds of sources, out of contest, puts them together in a chaotic mess, adds hyperbole and falsehoods and presents it to the world as though he has created something beautiful. He is either a brilliant con man or an unknowledgeable person who does not have the requisite skills to understand what he is doing. The sad thing is, apparently, some pastors and churches fall for his scheme.

“In order to better understand everything, let’s first discuss the IRS’s Jurisdiction over both 508c1a and 501c3. You’ll begin to see WHY creating your Church with a Church Establishment Affidavit and then organizing its finances through a subsequent Corporation Sole is the only viable way to creating a Church here in America.”

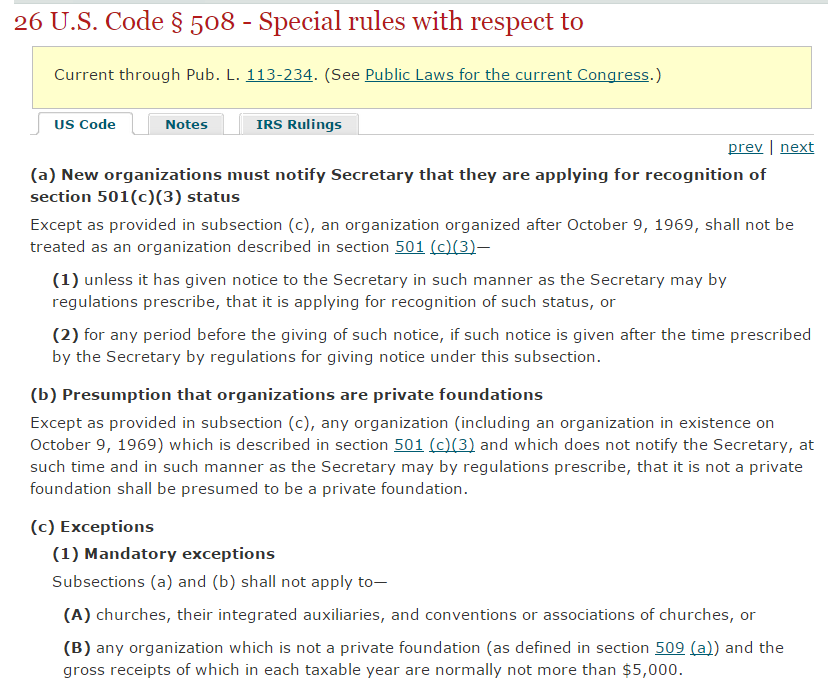

“First lets look at the law of 508c1a and what entities it has jurisdiction over:

“26 USC 508(c)(1)(a) gives MANDATORY Tax Exemption to Churches without any pre-conditions (Unlike 501c3’s stipulations of barring religious organizations from all political activity).

“Therefor, 508c1a has Jurisdiction over: Churches, their integrated auxiliaries, and conventions or associations of churches and any organization which is not a private foundation and the gross receipts of which in each taxable year are normally not more than $5,000.

“A Church organized with the use of a Statutory Declaration Affidavit is underneath the jurisdiction of 508c1a.

“While 501c3 only has Jurisdiction over: Corporations, Certain Trusts, Community Chests, Funds and Foundations. Source, Cornell Law University. You notice that the word CHURCH is completely absent from this list? Thats because Churches are NOT subject 501c3 rules, they are only mentioned in under the jurisdiction of 508c1a. It is generally misunderstood by most law professors that Churches are generally always under the classification of 501c3. This is a misconception because nearly 99% of all Churches are fully incorporated (thus fall under the Corporate designation of 501c3). Since a Church being formed through an affidavit and being declared under 508(c)(1)(a) is neither considered a Corporation, community chest, religious trust, fund or foundation, the same designation of a Church generally being under 501c3 DOES NOT APPLY.

“Now, unlike 508c1a that gives the Church mandatory tax exemption, 501c3’s tax exemption status is only guaranteed if the religious organization meets the conditions set forth in 501c3.

“These Restrictions for Churches Include:

…“

Click the above to read “1,000 Pastors who pledge to defy IRS and preach politics from pulpit ahead of election misunderstand the law and the hierarchy of law.”

The government has jurisdiction over incorporated churches (including corporation sole churches). The same rules are applied by the IRS to both 501c3 and 508 churches. I have covered this in Church Internal Revenue Code § 508 Tax Exempt Status. You can go directly to the article, of course, by left clicking the link in the last sentence. The IRS makes clear that the 508 church is subject to the same rules as the 501c3 church. Some 501c3 churches are publically proclaiming that they are breaking the rules of 501c3 and the IRS usually has not taken action against them. I wish the IRS had the resources to confront all 501c3 and 508 churches who break the rules. Why? Because all churches who are legal entities such as incorporated churches (including non-profit corporation sole churches) and all 501c3 and 508 churches grieve our Lord by operating under man’s laws rather than under God’s law. I covered the activities of the “Pulpit Initiative” churches several years ago in the article 1,000 Pastors who pledge to defy IRS and preach politics from pulpit ahead of election misunderstand the law and the hierarchy of law. That article will serve as my further comments here.

“To disprove skeptics that would claim otherwise, let me prove to you that a Corporation Sole is immune to this 501c3 requirement. Please allow me present to you an active Oregon State Law § 65.067 (1) which states,

“1.) Any individual may, in conformity with the constitution, canons, rules, regulations and disciplines of any church or religious denomination, form a corporation hereunder to be a corporation sole. Such corporation shall be a form of religious corporation and will differ from other such corporations organized hereunder only in that it shall have no board of directors, need not have officers and shall be managed by a single director who shall be the individual constituting the corporation and its incorporator or the successor of the incorporator.

“All other religious organizations, religious trusts, community chests funds and foundations are subjected to this IRS rule and are legally required to have a board.”

Oregon Revised Statutes Section 65.067. Click the above image to go directly to statute.

He says an active Oregon State Law § 65.067 (1) law, but quotes the 2011, as opposed to the 2013 amended law. Notice that the law he quotes does not require a Church Establishment Affidavit. Then, he adds his own statement: “All other religious organizations, religious trusts, community chests funds and foundations are subjected to this IRS rule and are legally required to have a board.” That does not prove that the corporation sole is immune to the 501c3 requirement. 501c3 has no such rule which requires any church to have a board. The Oregon Non-Profit Corporation Law can be accessed at the following link: 2013 Oregon Revised Statutes,Oregon Non-profit Corporation Law, Volume 2 Business Organizations, Commercial Code§ 65.067. Read it for yourself. You will see that Joshua Kenny-Greenwood is wrong (to be kind).

Greenwood continues:

“#2. No substantial part of the activities of which is carrying on propaganda and which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public office:

“This absolutely satanic law means your incorporated Church or religious trust CANNOT engage in or influence any aspect of public policy for any reason whatsoever. Completely defeating the intent of the Church achieving its purpose of fulfillingRomans 8:20-21.

“This is why the Church Establishment Affidavit is so important. Only Corporations (that means ANY incorporated Church or religious organization), Trusts (that means ANY form of a religious trust), community chests, funds and/or foundations are under the jurisdiction of 501c3. Since the Statutory Declaration is neither one of things listed above, it is completely immune to 501c3 and is allows your Church to be under the law of 508c1a. Without this jurisdictional distinction between the Church itself (created under the affidavit) and the office of the Corporation Sole (which is incorporated as a 501c3 for banking purposes) then it would be impossible under current US law to organize a ministry using any other method without the Church itself fully coming under the law of 501c3.”

As has been shown and as is obvious from the law relied upon by the promoters of the church corporation sole, the corporation sole is a corporation provided for by state law. As such, it is subject to the rules that come with 501(c)(3) when it in any way appeals to either 501(c)(3) or 508. One cannot simply override reality by concocted rhetoric as the writings of Church Freedom and the Corporation Sole website purport to do.

3. Analysis of “WHY OUR CHURCH ESTABLISHMENT AFFIDAVIT IS SO IMPORTANT TO CHURCHES”

“We should note that the Church Establishment Affidavit we’ve created here at The Empowerment Center was crafted in such a manner that it accomplishes the following:

It lawfully fulfills ALL 14 Points both the IRS and courts require Churches to have in order to be legally recognized as a Church by the Federal Government.

It distinctly declares the difference between the Church itself and isolated Office of the Corporation Sole (including the different responsibilities of each office).

It uniquely declares your Corporation Sole’s intended future Successor and it defines who fulfills the role of its Secretary.

It allows for two additional witness Church members to declare and affirm the existence of this said Church/Ministry.

It declares its recognition of being under the law of 508c1a.

It declares that it does NOT find it advantageous to seek official recognition from the IRS for the Churches tax exemption status and rejects the IRS’s form 1023.

It removes all doubts and puts an end to any conflicting decision regarding your Churches existence.

The Bank will use it to validate the role of the Successor in the event of the Corporation Sole’s demise and or resignation.“

My comments. I have already covered everything of importance here in other portions of the booklet, but I will add a few comments here. Notice that the Affidavit defines the church according to IRS criteria, not Bible doctrine, so that the IRS will recognize the religious organization as being a church. In other parts of the website, the Empowerment Center recognizes that corporation sole status makes the church a legal entity, not a spiritual New Testament entity only. Hence, the corporation sole church obviously violates Bible principles for New Testament church organization. All church members of a New Testament church will affirm the existence of the New Testament church. In fact, the Lord Jesus Christ will affirm the existence of the New Testament Church; He will be pleased with the New Testament church. His precepts show that the corporation sole church is a religious organization, not a New Testament church and that He is grieved when a church organizes as any kind of corporation, including a corporation sole. The corporation sole status removes any doubts that the church is a worldly religious organization, not a New Testament church. When a church claims 508 status, that church does not fill out IRS form 1023. The 508 church is subject, as explained elsewhere, to the same rules and the 501(c)(3). In other words, the 508 church is under the authority of the Internal Revenue Service as to the rules which come with 501(c)(3) status.

4. Analysis of “DOES THE GOVERNMENT OR IRS REALLY WANT THIS FIGHT?”

The Corporation Sole Scheme chains a church to the government, then she invites a fight with the government.

“Prior to our Church writing the Book and setting the record straight on the Corporation Sole, no one had ever thought to use an unincorporated Church Affidavit to both manifest the Church but also outline the jurisdictional distinction between the Church itself and the isolated office of the Corporation Sole. Then use the Church that is under the law of 26 USC 508(c)(1)(a) and NOT the 501c3 Corporation Sole to conduct operations that could influence public policy.”

No wonder no one had thought to do so. Obviously, the Lord Jesus Christ did not have Joshua Kenny-Greenwood around to help him build his church. The Lord established a reasonable order for His churches, not a chaotic order such as that proposed by Kenny-Greenwood. The Lord inspired the Apostle Paul as he, under the inspiration of God, laid out the ordered doctrine of the New Testament church. No wonder no one else thought of Kenny-Greenwood’s sham. It is so riddled with legal and spiritual error that only one with a fertile imagination and knowledge of neither relevant Bible principles nor law would have implemented it had they thought of it.

“There is an argument to be made that a Church can perform and operate in this manner and not become subjected to 501c3 political restrictions (since the affidavit clearly outlines the different jurisdictions). In fact, it would be the only argument the Church could legally make since every other method a Church uses to incorporate or manage its finances places it underneath 501c3’s jurisdiction.”

This method also, as I have explained over and over in this booklet, places the corporation sole church of Joshua Kenny-Greenwood under the rules of 501c3. Furthermore, he again concedes that the corporation sole church is a legal entity (a non-profit corporation) since only a legal entity can be taken to court. Since she can be taken to court, the state (through the court) is her authority. She is bound to abide by the decision of her authority, the court.

“We understand that this puts us in a position where there is no prior legal precedence for this type of legal claim. That is good for several reasons:

“If the IRS really wanted that fight and wanted to disprove that the said Church in this claim (Lets use our Church, The Empowerment Center, as an example) is in fact NOT a Church, they are going to need to be able to disprove our affidavit (which is vital to our argument that our Church is indeed a Church) is false. They would have several problems in this area. First, they would need to prove that everyone on the affidavit was lying (and thus committed the penalties of perjury). This would be especially difficult since it is VERY difficult for any Judge or IRS official to have the proper regulatory authority to even legally define a Church (one might even say to legally define a Church is unconstitutional in and of itself)! Now, the IRS has in place what they consider a 14 point test to see whether or not a Church is a legitimate Church. The principles of this test are used by the IRS and courts to determine if a Church is just that, a Church. Never mind that in the very same report the authors make the very wise statement that we will HEAVILY be using in any defense,

“‘Given the variety of religious practice, the determination of what constitutes a church is inherently unquantifiable. Attempts to use a dogmatic numerical approach might unconstitutionally favor established churches at the expense of newer, less traditional institutions.” –IRS 14 point rule guide.’”

I have already covered the evidence needed in federal court above. Your church members could testify that the church meets the 14 IRS criteria. That is not the problem. They would hold your church to be a church. I know that the Lord Jesus Christ in His word proves that an Empowerment Center church is not a New Testament church. The problem is that your church is under and recognizes the authority of the state to decide questions brought to them. You have a hybrid church, with two heads – er, maybe only one head, the state. After all, you have defined your church according to the IRS rule book, not God’s rule book.

“Here at The Empowerment Center and ChurchFreedom.org, we recognized this opening and took all 14 points to the IRS’s own preferences and applied them within the framework of our affidavit. Its important that we did this, as this should be enough to satisfy their very own discrepancies since a minimum of 4-5 people are coming together and attesting to these facts under the penalty of perjury, facts that any lawful Church could easily prove. This leaves only the isolated Corporation Sole as the lone bearer of the 501c3 status and not the Church itself. This means the Corporation Sole (which is the only entity underneath 501c3’s jurisdiction) needs to be the sole party responsible for any alleged violations to the 501c3 principle (which again, should only be limited to the 501c3 Corporate Sole and NOT the 508c1a Church). In addition, we would also take a play from the Alliance Defending Freedom’s Pulpit Freedom Sundays playbook as well and argue a secondary point that in their words,

“‘For instance, if a church loses its tax-exempt status for the pastor speaking from the pulpit, there is an argument to be made that because the church is automatically exempt under section 508(c)(1) (A) of the Internal Revenue Code, the tax-exempt status is only lost for the day the sermon was preached, and any contributions made at other times would still be deductible. It is important to note that this argument has not been tested and taxpayers should seek professional advice before claiming any such deduction for itemization.” –From, Pulpit Freedom Sunday and The Alliance Defending Freedom

Here, as in many other places, Joshua Kenny-Greenwood contradicts himself. Read it and figure it out for yourself. Kenny-Greenwood’s writings on this website are so ill-conceived and crazy that reading them leaves a knowledgeable believer who understands these matters with a spiritual headache. I would not continue this booklet if not for the Lord’s admonitions to his children to stand for truth, to fight the spiritual warfare that He has called us to fight. As to the quote from the ADF Pulpit Freedom Sunday’s, I again refer the reader to the article 1,000 Pastors who pledge to defy IRS and preach politics from pulpit ahead of election misunderstand the law and the hierarchy of law.

The argument he then refers to is ridiculous in light of the truths I have presented in this booklet. The argument is for the person who is denied the tax deduction for gifts to a church and not for the church and the church corporation (corporation sole in this instance). Remember what Joshua Kenny-Greenwood wrote in

“Benefit #8 – TAX DEDUCTIBLE CONTRIBUTIONS: A Church that has a Corporation Sole CAN receive tax deductible contributions from any member that gives a gift. The Corporation Sole is also immune from being required by law to give the donor a receipt acknowledging their gift! In this case, it is the responsibility of the donor to keep their records and NOT the Church or Corporation Sole. If your Church chooses to do so, it may voluntarily and freely (out of the kindness of its heart) give the donor a receipt acknowledging their contribution or donation.”

He did not seem to be concerned about the giver when he wrote Benefit #8. I analyzed Alleged Benefit # 8 in Chapter 2: Analysis of “Benefits of the Corporation Sole Comparedto a Traditional 501c3. Furthermore, the corporation sole church has no reason not to give an acknowledgement. It, as has been explained in this booklet several times, is a 508 church which is required to abide by the rules of 501c3.

“Making such bold argument(s) for legitimate Churches could potentially set a VERY REAL and VERY SERIOUS precedence if the Federal Government failed to make their case to a Judge or Jury. If they challenge our argument that Churches operating under the law of 26 USC 508(c)(1)(a), not the Churches subsequent and isolated Corporation Sole, can influence politics, have the Church body vote for or against political candidates, have the Church lobby congress or have the Church distribute political propaganda on behalf or against any political candidate for office (once again, the Church and NOT the 501c3 isolated Corporation Sole) and they lose, then they will potentially open the door WIDE OPEN for EVERY SINGLE CHURCH IN AMERICA to RUN to get their Corporation Sole and be FREE from the political restrictions that have plagued our Nations Churches. If they win such an argument, by the time they win we would have already freely given away our Corporation Sole support to TENS OF THOUSANDS of CHURCHES that already HATE 501c3 with a passion and are already bold enough to speak unfiltered truth behind the pulpit. This could mean EXTREME backlash from potentially millions of registered voters from members of those congregations (many of whom are EXTREMELY influential Christian business men and politicians themselves) that we’ve been training Pastors in how to lead in influencing intended Christian reforms. To make enemies with the Church as well in a political season such as this with the IRS already embroiled in scandal after scandal (from Lois Lerner lying to Congress to the IRS ‘accidentally’ destroying all hard drive evidence) or a Justice Department that fails to enforce current laws or investigate any Government agency of any wrongdoing, it would leave a VERY bad taste in the mouth of Christian voters in these Churches and would propel us to the National Spotlight (which is EXACTLY what we want, so we can make our case to Christians everywhere). It would also be extremely unwise timing as they would have underestimated the Jury’s potential disdain for the Government and their routine MANY failures, coverups and current violations to oaths of office perceived by the American public by officials in the Federal Government (this is in addition to the fact, that we will call upon the several hundred eye witnesses and VERY Charismatic Pastors that will first hand testify that we’re a Church). Any one person being on that Jury that is either a Republican or Christian WILL side with us. This would give the Church a HUGE edge in court. Either way, wisdom would see that such a challenge (if ever) given by the Government based on these merits would end up being a lose/lose situation for them.”

Church Freedom and the Corporation Sole has already lost because your scheme is not according to the Bible and not according to the law. Your incorporated 508 church is subject to the rules of 501c3. That has already been covered in this booket. Since the IRS does not have the resources to deal with every state church who is violating the rules of 501c3, they are not enforcing the law. You are grieving the Lord by organizing a state church (a legal entity). You did not have to so organize, but you did. You then try to twist the law to conform to your vision. The main thing is that your authority is the state. If the IRS wishes to take your church(es) to court for alleged violations of the rules that come with 501(c)(3), they can. They have authority over you. Christ does not wish His authority over His churches to be shared with anyone. Old Paths Baptist Church Separation of Church and State Law Ministry helps churches remain under God only. We can do this because we correctly understand Bible principle and law.

“This is WHY we do whatever it takes to freely give our support to as many qualified approved Churches in the shortest time as humanly possible. Officials should know and understand that while other unscrupulous Corporation Sole peddlers have fallen to greed and tried to sell the Corporation Sole away as a mere tax shelter, we have not. We ABSOLUTELY NEVER give our support to individuals or entities looking to create a tax shelter. If a person cannot get at least 4 living people over the age of 21 that are willing to sign an affidavit under the penalties of perjury that they are a bona fide Church that lives up to the IRS’s own 14 point test, then we deny their application immediately. We’ve denied more applications than anyone knows with individuals trying to offer us everything you can think of for access to our support and we’ve denied ALL OF THEIR ATTEMPTS. If we even remotely smell someone coming that gives us the impression that they are either an individual trying to evade lawful taxes owed or an undercover informant trying to entrap us with promises of money, power or prestige for giving them our ministry and Corporation Sole support, we not only deny their application but we also permanently prohibit their access to our website by blocking their unique IP address. We ONLY work with legitimate BONA FIDE Churches.”

Church Freedom and the Corporation Sole needs to study these matters out and trash their ill-conceived ideas and schemes. They are not according to knowledge, as this booklet has made perfectly clear.

“This is why we need your help to spread the word about ChurchFreedom.org! We want to freely help support EVERY SINGLE Christian Church here in America. With your help, we’ve been able to directly support over 2,000 new Christian Churches this year alone. With your help, we can help FREE America’s Churches from 501c3 entirely.”

If Church Freedom and the Corporation Sole loves the Lord, then they need to study, grow in knowledge, understanding, and wisdom and repent. They need to contact all the churches they have helped, ask forgiveness, let them know the truth, and encourage them to trash their Affidavits, dissolve their corporations and organize according to Bible principles.

The local church sanctified and cleansed by the washing of water by the word——————–A ministry of Charity Baptist Tabernacle of Amarillo, Texas led by Pastor Ben Hickam. "Would to God ye could bear with me a little in my folly: and indeed bear with me. For I am jealous over you with godly jealousy: for I have espoused you to one husband, that I may present you as a chaste virgin to Christ. But I fear, lest by any means, as the serpent beguiled Eve through his subtilty, so your minds should be corrupted from the simplicity that is in Christ" (2 Corinthians 11:1-3). ————————————Jerald Finney, a Christian Lawyer and member of Charity Baptist Tabernacle, having received this ministry in the Lord, explains how a church in America can remain under the Lord Jesus Christ and Him only. "As every man hath received the gift, even so minister the same one to another, as good stewards of the manifold grace of God. If any man speak, let him speak as the oracles of God; if any man minister, let him do it as of the ability which God giveth: that God in all things may be glorified through Jesus Christ, to whom be praise and dominion for ever and ever. Amen" (1 Peter 4:10-11; See also, Ephesians 4::1-16 and 1 Corinthians 12:1-25). "Take heed to the ministry which thou hast received in the Lord, that thou fulfil it" (Colossians 4:17). "And hath put all things under his feet, and gave him to be the head over all things to the church" (Ephesians 1.22; See also, e.g. Colossians 1:18).