Note: the Church Freedom and Corporation Sole Website has been removed and the links thereto are no longer valid.

Contents of this booklet (left click link to go to entry):

Chapter 1: Legal Entity Status and the Corporation Sole

Chapter 2: Analysis of “Benefits of the Corporation Sole Compared to a Traditional 501c3 Church”

Chapter 3: Analysis of “Church Establishment Affidavit”

Appendix A: What is a Corporation Sole?

Appendix B: Corporation Sole and Internal Revenue Code §§ 501(c)(3) and 508(c)(!)(A) (Below)

Related articles:

- Expose And Reject The Teachings and Methods of Church Organization Con-Artists and Charlatans (050616)

- Why Understanding and Applying Church and State Law Is Important for Believers and Churches (June 3, 2012 article)

- See Comparison of Bible Trust (ordinary trust), Incorporation (includes corporation sole), and Ecclesiastical Law Center Trust for a concise chart of the differences each brings to church organization.

- A relevant and helpful article, as one who studies the above booklet out will see: Corporation: A human being without a soul

Jerald Finney

Copyright © February 6, 2015

As shown in Appendix A, a corporation sole church is a non-profit corporation, a creature of the state. Let us look at the 501(c)(3) ramifications of this.

Internal Revenue Code § 501(a)(c)(3) states, in relevant part:

“(a) Exemption from taxation

An organization described in subsection (c) or (d) or section 401 (a) shall be exempt from taxation under this subtitle unless such exemption is denied under section 502 or 503.

…

“(c) List of exempt organizations

The following organizations are referred to in subsection (a):

…

“(3) Corporations, and any community chest, fund, or foundation, organized and operated exclusively for religious, charitable, scientific, testing for public safety, literary, or educational purposes, or to foster national or international amateur sports competition (but only if no part of its activities involve the provision of athletic facilities or equipment), or for the prevention of cruelty to children or animals, no part of the net earnings of which inures to the benefit of any private shareholder or individual, no substantial part of the activities of which is carrying on propaganda, or otherwise attempting, to influence legislation (except as otherwise provided in subsection (h)), and which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public office.”

Thus, according to Internal Revenue Code § 501(c)(3), corporations are exempt from taxation. A corporation sole is a corporation and therefore may apply for 501(c)(3) tax exempt status. (See Appendix A.).

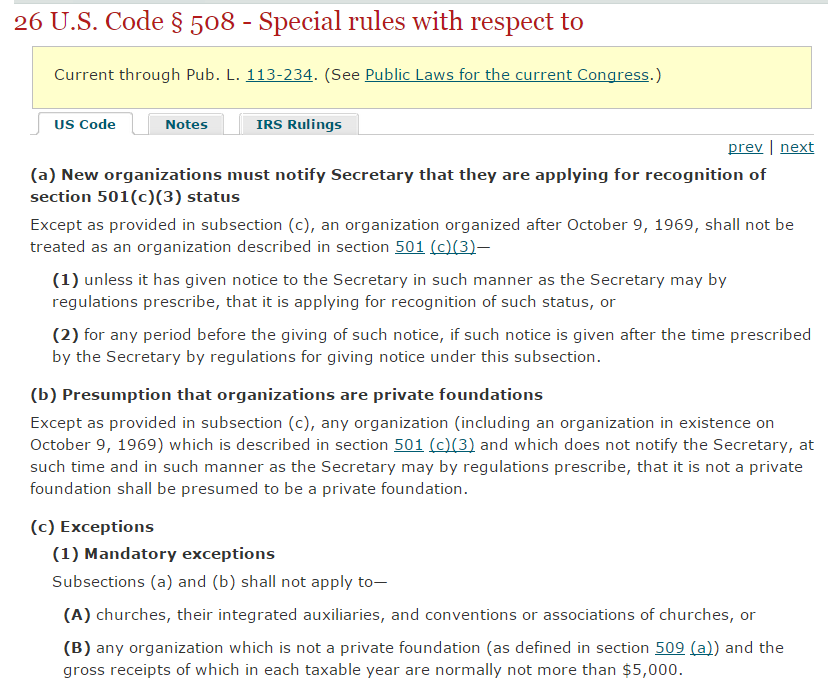

Some corporation sole churches do not like the rules that go with 501(c)(3) status. Therefore, they make the argument that, since they are not corporations, they may obtain Internal Revenue Code § 508(c)(1)(A) status, become automatically exempt, and not be subject to the rules that come with 501(c)(3). Their arguments are untenable because they are non-profit corporations. Yes, they, like any other church, may claim § 508 status; yes, they may become exempt under § 508; no, they, as § 508(c)(1)(A) churches, do not avoid the 501(c)(3) rules thereby. § 508(c)(1)(A) churches are subject to 501(c)(3) rules.

Corporation sole churches know that they may have to go to court to defend their position. This is an admission that they are legal entities who are under the authority of the state of incorporation and the federal government as to Internal Revenue Code matters. Whether they admit this or not, it is a fact established when they accepted the state’s offer for state, non-profit corporation status and when they claim § 508 status. Since they are legal entities, creatures of the state, their only challenge to rules they do not like is through action in state or federal court. Should they be taken to court, for example by the Internal Revenue Service, they have agreed that the state is the final judge of the issue being litigated.

The issue is one of authority. Those who love the Lord are willing to give their all if necessary as they refuse to follow lower laws when those laws conflict with the highest law. Millions of martyrs have followed the example of the apostles who said, when the authority of the Lord Jesus Christ was at issue, “We ought to obey God rather than men” (Acts 5:29).

Some corporation sole churches try to argue that they are not corporations and therefore that they may claim Internal Revenue Code § 508(c)(1)(A) status which insulates them from following the requirements of 501(c)(3). They do not mind being a creature of the state under the corporation sole law, but they try to avoid being under the rules that come with 501(c)(3). What they are trying to do is attain government approved tax exempt status (as opposed to First Amendment non-taxable status) without submitting to the rules of 501(c)(3). They do not mind the fact that they are not organized according to God’s rules in the New Testament and that they are a creature of the state of incorporation. They wish to twist the law in order to get what they falsely perceive to be benefits without the rules that come with the “benefits.” Their effort is not according to knowledge. The IRS has already covered this matter. 508 churches are held to be subject to the rules that come with 501(c)(3). (See Church Internal Revenue Code § 508 Tax Exempt Status for a full explanation).

Many non-profit corporation churches claim 501(c)(3) status without filing Internal Revenue Service form 1023. They do so in various ways One way is to include the provisions of 501(c)(3) in their corporate constitutions. Another is to simply acknowledge the exemption by giving acknowledgement to those who give. Even should a church not give acknowledgement, in the event of taxpayer audit, what the IRS wants to know is “what was given,” “did the taxpayer give in a manner prescribed by the IRS Code,” and “was the deduction given to a church (whether a legal entity or not.)”.

Corporation sole churches who try to twist the law to keep their deductible status while avoiding the rules that go with exempt status show their true colors to God and to those who take the time to examine what they are doing. Perhaps they act and speak ignorantly because of lack of both Bible and legal study which renders the subject outside their field of expertise.