As shown in Appendix A, a corporation sole church is a non-profit corporation, a creature of the state. Let us look at the 501(c)(3) ramifications of this.

Internal Revenue Code Section 501(c)(3). Click image above to go directly to 501(c)(3)

An organization described in subsection (c) or (d) or section 401(a) shall be exempt from taxation under this subtitle unless such exemption is denied under section 502 or 503.

…

“(c)List of exempt organizations

The following organizations are referred to in subsection (a):

…

“(3)Corporations, and any community chest, fund, or foundation, organized and operated exclusively for religious, charitable, scientific, testing for public safety, literary, or educational purposes, or to foster national or international amateur sports competition (but only if no part of its activities involve the provision of athletic facilities or equipment), or for the prevention of cruelty to children or animals, no part of the net earnings of which inures to the benefit of any private shareholder or individual, no substantial part of the activities of which is carrying on propaganda, or otherwise attempting, to influence legislation (except as otherwise provided in subsection (h)), and which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public office.”

Thus, according toInternal Revenue Code § 501(c)(3), corporations are exempt from taxation. A corporation sole is a corporation and therefore may apply for 501(c)(3) tax exempt status. (See Appendix A.).

Some corporation sole churches do not like the rules that go with 501(c)(3) status. Therefore, they make the argument that, since they are not corporations, they may obtain Internal Revenue Code § 508(c)(1)(A) status, become automatically exempt, and not be subject to the rules that come with 501(c)(3). Their arguments are untenable because they are non-profit corporations. Yes, they, like any other church, may claim § 508 status; yes, they may become exempt under § 508; no, they, as § 508(c)(1)(A) churches, do not avoid the 501(c)(3) rules thereby. § 508(c)(1)(A) churches are subject to 501(c)(3) rules.

Corporation sole churches know that they may have to go to court to defend their position. This is an admission that they are legal entities who are under the authority of the state of incorporation and the federal government as to Internal Revenue Code matters. Whether they admit this or not, it is a fact established when they accepted the state’s offer for state, non-profit corporation status and when they claim § 508 status. Since they are legal entities, creatures of the state, their only challenge to rules they do not like is through action in state or federal court. Should they be taken to court, for example by the Internal Revenue Service, they have agreed that the state is the final judge of the issue being litigated.

The issue is one of authority. Those who love the Lord are willing to give their all if necessary as they refuse to follow lower laws when those laws conflict with the highest law. Millions of martyrs have followed the example of the apostles who said, when the authority of the Lord Jesus Christ was at issue, “We ought to obey God rather than men” (Acts 5:29).

Internal Revenue Code Section 508. Click image above to go directly to 508.

Some corporation sole churches try to argue that they are not corporations and therefore that they may claim Internal Revenue Code § 508(c)(1)(A) status which insulates them from following the requirements of 501(c)(3). They do not mind being a creature of the state under the corporation sole law, but they try to avoid being under the rules that come with 501(c)(3). What they are trying to do is attain government approved tax exempt status (as opposed to First Amendment non-taxable status) without submitting to the rules of 501(c)(3). They do not mind the fact that they are not organized according to God’s rules in the New Testament and that they are a creature of the state of incorporation. They wish to twist the law in order to get what they falsely perceive to be benefits without the rules that come with the “benefits.” Their effort is not according to knowledge. The IRS has already covered this matter. 508 churches are held to be subject to the rules that come with 501(c)(3). (See Church Internal Revenue Code § 508 Tax Exempt Status for a full explanation).

Many non-profit corporation churches claim 501(c)(3) status without filing Internal Revenue Service form 1023. They do so in various ways One way is to include the provisions of 501(c)(3) in their corporate constitutions. Another is to simply acknowledge the exemption by giving acknowledgement to those who give. Even should a church not give acknowledgement, in the event of taxpayer audit, what the IRS wants to know is “what was given,” “did the taxpayer give in a manner prescribed by the IRS Code,” and “was the deduction given to a church (whether a legal entity or not.)”.

Corporation sole churches who try to twist the law to keep their deductible status while avoiding the rules that go with exempt status show their true colors to God and to those who take the time to examine what they are doing. Perhaps they act and speak ignorantly because of lack of both Bible and legal study which renders the subject outside their field of expertise.

Click to go directly to Church Establishment Affidavit Page

1. Analysis of the first two paragraphs 2. Analysis of section 1, “THE JURISDICTIONAL DISTINCTION AND DIFFERENCES BETWEEN THE LAWS OF 508C1A AND 501C3 IN THEIR RELATIONSHIP TO A CHURCH ESTABLISHMENT AFFIDAVIT” 3. Analysis of section 2 “WHY OUR CHURCH ESTABLISHMENT AFFIDAVIT IS SO IMPORTANT TO CHURCHES” 4. Analysis of “DOES THE GOVERNMENT OR IRS REALLY WANT THIS FIGHT?”

“When getting a Corporation Sole for your Church and Ministry, it is important to note that your actually creating two separate legal creatures. First, you create your Church (which is legally manifested through a Church Establishment Affidavit) and then the Churches subsequent Corporation Sole (which is nothing more than an incorporated office held within the Church for the purposes of managing all of the Churches assets and is NOT the Church itself).”

My comments. Yes, you are creating two legal creatures, but they are not separate which is made clear by the law and by the paragraph quoted above. Notice that he says, “Corporation Sole (which is nothing more than an incorporated office held within the Church for the purposes of managing all of the Churches assets and is NOT the Church itself). The incorporated sole office is held within the church for the purpose of managing all of the Church’s assets. It is also an office created by the corporation sole contract with the state, Oregon in this case. The Bible mentions no such office for a New Testament church. A church under God will comply with New Testament guidelines for the church. A church under the state, created by men, such as the church created by a Church Establishment Affidavit, will concoct its own manner of organization. Some will then publish that method and deceive others such that they contribute monetarily (of course, they are not required to donate) to the deceivers who help them profane God’s church through devices such as non-profit corporation sole and Church Establishment Affidavit which, among other things, defines the church according to the IRS defintion of a church.

“A Corporation Sole CANNOT be established unless your Church is first created through the use of a Church Establishment Affidavit that needs to be signed by both you as the Pastor of the Church but also two Church member witnesses and your Churches eventual Corporation Sole’s Successor and/or Secretary. If a Corporation Sole were to be established prior to you signing, witnessing and having notarized the Church Affidavit, then your Corporation Sole can be out of statutory compliance and potentially deemed a sham organization by the IRS.”

This man, Joshua Kenny-Greenwood, Overseer of The Empowerment Center Church, just makes stuff up, as I have pointed out over and over in this booklet. Hundreds of thousands of churches alone have been established under God, in Bible order, without a church establishment affidavit. Sadly, most American churches chose, against the will of God according to His word, to become legal entities such as non-profit corporations (which, as explained in prior chapters, includes the corporation sole non-profit corporation), unincorporated associations, charitable trusts, and business trusts; the vast majority of those went on to become 501(c)(3) churches. There is a significant remnant of churches in America who are doing things God’s way.

“The reason we emphasis that a Church must first be organized through an Church Establishment Affidavit, is because an Affidavit is the highest form of evidence a person can bring forth into a Federal courtroom. This allows your ministry to prove to the court,without a reasonable doubt, the distinct legal existence of your Church, its MANDATORY tax exemption jurisdiction under the law of 26 USC 508(c)(1)(a), creates a record that is signed under the penalties of perjury by multiple Church members and declares that your Church even adopts the IRS’s own 14 point standard to even be legally recognized as a Church! Its creation and use also allows the Church to create a legal and jurisdictional separation of responsibilities between the role of the Church itself and the isolated and incorporated office of the Corporation Sole (which the latter is under 501c3’s jurisdiction).”

Click to go directly to code.

Should the IRS target a church which is a legal entity, such as a corporation sole church, for some reason, the church will have to first go through the agency process, perhaps a hearing. The IRS Code § 7611 covers church tax inquiries and examinations. § 7611 says:

IRS personnel must observe the restrictions imposed by IRC § 7611 in any inquiry or examination of a church. Such inquiry or examination must be limited to determining whether:

The organization is exempt from tax under IRC § 501(a),

The organization is a church under IRC §§ 509(a)(1) and 170(b)(1)(A)(i),

The church is carrying on an unrelated trade or business as defined in IRC § 513,

The church is otherwise engaged in activities subject to federal tax, or

The church has engaged in an excess benefit transaction (See procedures in IRM 7.27.30.8).

The term “church” includes

Any organization claiming to be a church. However, see ,IRM 4.76.7.4.2(4), and

Any convention or association of churches.

Should the IRS begin an inquiry and examination of a corporation sole church, or any other church which is a legal entity, they must abide by § 7611. Should the church lose in the agency process, she can appeal to Federal Court. Affidavits are not acceptable evidence in many agency and court proceedings. Generally, the adversary has the right to cross-examination. If a trial is required, affidavits will not be accepted. Witness evidence under oath and subject to cross-examination is the highest form of evidence and witness evidence will be required. Even should a church corporation sole be supported by affidavit, an affidavit is not subject to cross-examination and the IRS can subpoena the signers of the affidavit and place them under cross-examination. Since the signers have already displayed their ignorance by falling for the corporation sole scheme, they most assuredly would not look good under cross-examination by an experienced and studied government attorney. The IRS can also bring in other witnesses. See § 7611 for the areas the IRS can inquire into.

2. Analysis of section 1, “THE JURISDICTIONAL DISTINCTION AND DIFFERENCES BETWEEN THE LAWS OF 508C1A AND 501C3 IN THEIR RELATIONSHIP TO A CHURCH ESTABLISHMENT AFFIDAVIT”

This section is like the writing on this entire website, a disgrace in the eyes of man and God. It is similar to a written Frankenstein in that its author, Joshua Kenny-Greenwood, grabs quotes from all kinds of sources, out of contest, puts them together in a chaotic mess, adds hyperbole and falsehoods and presents it to the world as though he has created something beautiful. He is either a brilliant con man or an unknowledgeable person who does not have the requisite skills to understand what he is doing. The sad thing is, apparently, some pastors and churches fall for his scheme.

“In order to better understand everything, let’s first discuss the IRS’s Jurisdiction over both 508c1a and 501c3. You’ll begin to see WHY creating your Church with a Church Establishment Affidavit and then organizing its finances through a subsequent Corporation Sole is the only viable way to creating a Church here in America.”

“First lets look at the law of 508c1a and what entities it has jurisdiction over:

“26 USC 508(c)(1)(a) gives MANDATORY Tax Exemption to Churches without any pre-conditions (Unlike 501c3’s stipulations of barring religious organizations from all political activity).

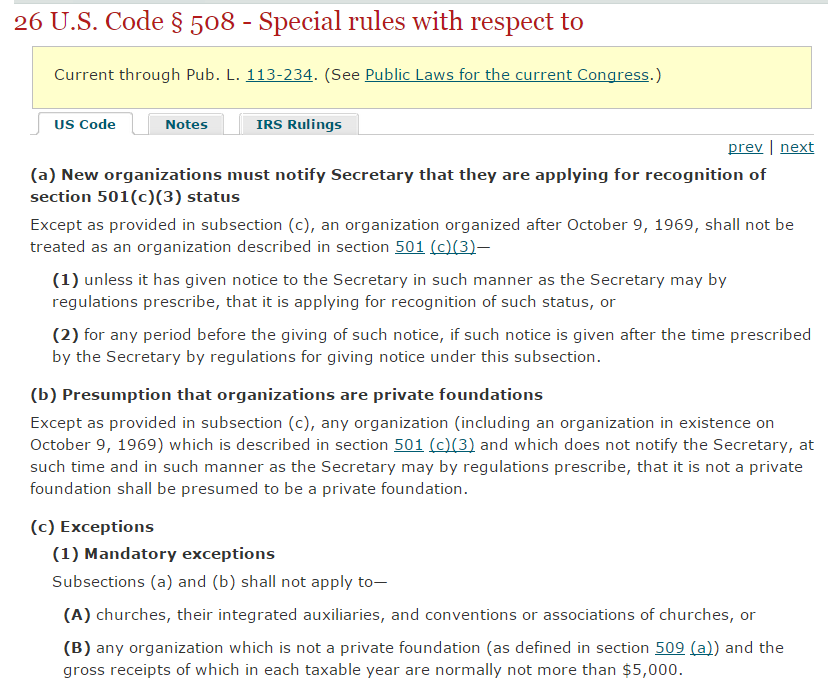

“Therefor, 508c1a has Jurisdiction over: Churches, their integrated auxiliaries, and conventions or associations of churches and any organization which is not a private foundation and the gross receipts of which in each taxable year are normally not more than $5,000.

“A Church organized with the use of a Statutory Declaration Affidavit is underneath the jurisdiction of 508c1a.

“While 501c3 only has Jurisdiction over: Corporations, Certain Trusts, Community Chests, Funds and Foundations. Source, Cornell Law University. You notice that the word CHURCH is completely absent from this list? Thats because Churches are NOT subject 501c3 rules, they are only mentioned in under the jurisdiction of 508c1a. It is generally misunderstood by most law professors that Churches are generally always under the classification of 501c3. This is a misconception because nearly 99% of all Churches are fully incorporated (thus fall under the Corporate designation of 501c3). Since a Church being formed through an affidavit and being declared under 508(c)(1)(a) is neither considered a Corporation, community chest, religious trust, fund or foundation, the same designation of a Church generally being under 501c3 DOES NOT APPLY.

“Now, unlike 508c1a that gives the Church mandatory tax exemption, 501c3’s tax exemption status is only guaranteed if the religious organization meets the conditions set forth in 501c3.

“These Restrictions for Churches Include:

…“

Click the above to read “1,000 Pastors who pledge to defy IRS and preach politics from pulpit ahead of election misunderstand the law and the hierarchy of law.”

The government has jurisdiction over incorporated churches (including corporation sole churches). The same rules are applied by the IRS to both 501c3 and 508 churches. I have covered this in Church Internal Revenue Code § 508 Tax Exempt Status. You can go directly to the article, of course, by left clicking the link in the last sentence. The IRS makes clear that the 508 church is subject to the same rules as the 501c3 church. Some 501c3 churches are publically proclaiming that they are breaking the rules of 501c3 and the IRS usually has not taken action against them. I wish the IRS had the resources to confront all 501c3 and 508 churches who break the rules. Why? Because all churches who are legal entities such as incorporated churches (including non-profit corporation sole churches) and all 501c3 and 508 churches grieve our Lord by operating under man’s laws rather than under God’s law. I covered the activities of the “Pulpit Initiative” churches several years ago in the article 1,000 Pastors who pledge to defy IRS and preach politics from pulpit ahead of election misunderstand the law and the hierarchy of law. That article will serve as my further comments here.

“To disprove skeptics that would claim otherwise, let me prove to you that a Corporation Sole is immune to this 501c3 requirement. Please allow me present to you an active Oregon State Law § 65.067 (1) which states,

“1.) Any individual may, in conformity with the constitution, canons, rules, regulations and disciplines of any church or religious denomination, form a corporation hereunder to be a corporation sole. Such corporation shall be a form of religious corporation and will differ from other such corporations organized hereunder only in that it shall have no board of directors, need not have officers and shall be managed by a single director who shall be the individual constituting the corporation and its incorporator or the successor of the incorporator.

“All other religious organizations, religious trusts, community chests funds and foundations are subjected to this IRS rule and are legally required to have a board.”

Oregon Revised Statutes Section 65.067. Click the above image to go directly to statute.

He says an active Oregon State Law § 65.067 (1) law, but quotes the 2011, as opposed to the 2013 amended law. Notice that the law he quotes does not require a Church Establishment Affidavit. Then, he adds his own statement: “All other religious organizations, religious trusts, community chests funds and foundations are subjected to this IRS rule and are legally required to have a board.” That does not prove that the corporation sole is immune to the 501c3 requirement. 501c3 has no such rule which requires any church to have a board. The Oregon Non-Profit Corporation Law can be accessed at the following link: 2013 Oregon Revised Statutes,Oregon Non-profit Corporation Law, Volume 2 Business Organizations, Commercial Code§ 65.067. Read it for yourself. You will see that Joshua Kenny-Greenwood is wrong (to be kind).

Greenwood continues:

“#2. No substantial part of the activities of which is carrying on propaganda and which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public office:

“This absolutely satanic law means your incorporated Church or religious trust CANNOT engage in or influence any aspect of public policy for any reason whatsoever. Completely defeating the intent of the Church achieving its purpose of fulfillingRomans 8:20-21.

“This is why the Church Establishment Affidavit is so important. Only Corporations (that means ANY incorporated Church or religious organization), Trusts (that means ANY form of a religious trust), community chests, funds and/or foundations are under the jurisdiction of 501c3. Since the Statutory Declaration is neither one of things listed above, it is completely immune to 501c3 and is allows your Church to be under the law of 508c1a. Without this jurisdictional distinction between the Church itself (created under the affidavit) and the office of the Corporation Sole (which is incorporated as a 501c3 for banking purposes) then it would be impossible under current US law to organize a ministry using any other method without the Church itself fully coming under the law of 501c3.”

As has been shown and as is obvious from the law relied upon by the promoters of the church corporation sole, the corporation sole is a corporation provided for by state law. As such, it is subject to the rules that come with 501(c)(3) when it in any way appeals to either 501(c)(3) or 508. One cannot simply override reality by concocted rhetoric as the writings of Church Freedom and the Corporation Sole website purport to do.

3. Analysis of “WHY OUR CHURCH ESTABLISHMENT AFFIDAVIT IS SO IMPORTANT TO CHURCHES”

“We should note that the Church Establishment Affidavit we’ve created here at The Empowerment Center was crafted in such a manner that it accomplishes the following:

It lawfully fulfills ALL 14 Points both the IRS and courts require Churches to have in order to be legally recognized as a Church by the Federal Government.

It distinctly declares the difference between the Church itself and isolated Office of the Corporation Sole (including the different responsibilities of each office).

It uniquely declares your Corporation Sole’s intended future Successor and it defines who fulfills the role of its Secretary.

It allows for two additional witness Church members to declare and affirm the existence of this said Church/Ministry.

It declares its recognition of being under the law of 508c1a.

It declares that it does NOT find it advantageous to seek official recognition from the IRS for the Churches tax exemption status and rejects the IRS’s form 1023.

It removes all doubts and puts an end to any conflicting decision regarding your Churches existence.

The Bank will use it to validate the role of the Successor in the event of the Corporation Sole’s demise and or resignation.“

My comments. I have already covered everything of importance here in other portions of the booklet, but I will add a few comments here. Notice that the Affidavit defines the church according to IRS criteria, not Bible doctrine, so that the IRS will recognize the religious organization as being a church. In other parts of the website, the Empowerment Center recognizes that corporation sole status makes the church a legal entity, not a spiritual New Testament entity only. Hence, the corporation sole church obviously violates Bible principles for New Testament church organization. All church members of a New Testament church will affirm the existence of the New Testament church. In fact, the Lord Jesus Christ will affirm the existence of the New Testament Church; He will be pleased with the New Testament church. His precepts show that the corporation sole church is a religious organization, not a New Testament church and that He is grieved when a church organizes as any kind of corporation, including a corporation sole. The corporation sole status removes any doubts that the church is a worldly religious organization, not a New Testament church. When a church claims 508 status, that church does not fill out IRS form 1023. The 508 church is subject, as explained elsewhere, to the same rules and the 501(c)(3). In other words, the 508 church is under the authority of the Internal Revenue Service as to the rules which come with 501(c)(3) status.

4. Analysis of “DOES THE GOVERNMENT OR IRS REALLY WANT THIS FIGHT?”

The Corporation Sole Scheme chains a church to the government, then she invites a fight with the government.

“Prior to our Church writing the Book and setting the record straight on the Corporation Sole, no one had ever thought to use an unincorporated Church Affidavit to both manifest the Church but also outline the jurisdictional distinction between the Church itself and the isolated office of the Corporation Sole. Then use the Church that is under the law of 26 USC 508(c)(1)(a) and NOT the 501c3 Corporation Sole to conduct operations that could influence public policy.”

No wonder no one had thought to do so. Obviously, the Lord Jesus Christ did not have Joshua Kenny-Greenwood around to help him build his church. The Lord established a reasonable order for His churches, not a chaotic order such as that proposed by Kenny-Greenwood. The Lord inspired the Apostle Paul as he, under the inspiration of God, laid out the ordered doctrine of the New Testament church. No wonder no one else thought of Kenny-Greenwood’s sham. It is so riddled with legal and spiritual error that only one with a fertile imagination and knowledge of neither relevant Bible principles nor law would have implemented it had they thought of it.

“There is an argument to be made that a Church can perform and operate in this manner and not become subjected to 501c3 political restrictions (since the affidavit clearly outlines the different jurisdictions). In fact, it would be the only argument the Church could legally make since every other method a Church uses to incorporate or manage its finances places it underneath 501c3’s jurisdiction.”

This method also, as I have explained over and over in this booklet, places the corporation sole church of Joshua Kenny-Greenwood under the rules of 501c3. Furthermore, he again concedes that the corporation sole church is a legal entity (a non-profit corporation) since only a legal entity can be taken to court. Since she can be taken to court, the state (through the court) is her authority. She is bound to abide by the decision of her authority, the court.

“We understand that this puts us in a position where there is no prior legal precedence for this type of legal claim. That is good for several reasons:

“If the IRS really wanted that fight and wanted to disprove that the said Church in this claim (Lets use our Church, The Empowerment Center, as an example) is in fact NOT a Church, they are going to need to be able to disprove our affidavit (which is vital to our argument that our Church is indeed a Church) is false. They would have several problems in this area. First, they would need to prove that everyone on the affidavit was lying (and thus committed the penalties of perjury). This would be especially difficult since it is VERY difficult for any Judge or IRS official to have the proper regulatory authority to even legally define a Church (one might even say to legally define a Church is unconstitutional in and of itself)! Now, the IRS has in place what they consider a 14 point test to see whether or not a Church is a legitimate Church. The principles of this test are used by the IRS and courts to determine if a Church is just that, a Church. Never mind that in the very same report the authors make the very wise statement that we will HEAVILY be using in any defense,

“‘Given the variety of religious practice, the determination of what constitutes a church is inherently unquantifiable. Attempts to use a dogmatic numerical approach might unconstitutionally favor established churches at the expense of newer, less traditional institutions.” –IRS 14 point rule guide.’”

I have already covered the evidence needed in federal court above. Your church members could testify that the church meets the 14 IRS criteria. That is not the problem. They would hold your church to be a church. I know that the Lord Jesus Christ in His word proves that an Empowerment Center church is not a New Testament church. The problem is that your church is under and recognizes the authority of the state to decide questions brought to them. You have a hybrid church, with two heads – er, maybe only one head, the state. After all, you have defined your church according to the IRS rule book, not God’s rule book.

“Here at The Empowerment Center and ChurchFreedom.org, we recognized this opening and took all 14 points to the IRS’s own preferences and applied them within the framework of our affidavit. Its important that we did this, as this should be enough to satisfy their very own discrepancies since a minimum of 4-5 people are coming together and attesting to these facts under the penalty of perjury, facts that any lawful Church could easily prove. This leaves only the isolated Corporation Sole as the lone bearer of the 501c3 status and not the Church itself. This means the Corporation Sole (which is the only entity underneath 501c3’s jurisdiction) needs to be the sole party responsible for any alleged violations to the 501c3 principle (which again, should only be limited to the 501c3 Corporate Sole and NOT the 508c1a Church). In addition, we would also take a play from the Alliance Defending Freedom’s Pulpit Freedom Sundays playbook as well and argue a secondary point that in their words,

“‘For instance, if a church loses its tax-exempt status for the pastor speaking from the pulpit, there is an argument to be made that because the church is automatically exempt under section 508(c)(1) (A) of the Internal Revenue Code, the tax-exempt status is only lost for the day the sermon was preached, and any contributions made at other times would still be deductible. It is important to note that this argument has not been tested and taxpayers should seek professional advice before claiming any such deduction for itemization.” –From, Pulpit Freedom Sunday and The Alliance Defending Freedom

Here, as in many other places, Joshua Kenny-Greenwood contradicts himself. Read it and figure it out for yourself. Kenny-Greenwood’s writings on this website are so ill-conceived and crazy that reading them leaves a knowledgeable believer who understands these matters with a spiritual headache. I would not continue this booklet if not for the Lord’s admonitions to his children to stand for truth, to fight the spiritual warfare that He has called us to fight. As to the quote from the ADF Pulpit Freedom Sunday’s, I again refer the reader to the article 1,000 Pastors who pledge to defy IRS and preach politics from pulpit ahead of election misunderstand the law and the hierarchy of law.

The argument he then refers to is ridiculous in light of the truths I have presented in this booklet. The argument is for the person who is denied the tax deduction for gifts to a church and not for the church and the church corporation (corporation sole in this instance). Remember what Joshua Kenny-Greenwood wrote in

“Benefit #8 – TAX DEDUCTIBLE CONTRIBUTIONS: A Church that has a Corporation Sole CAN receive tax deductible contributions from any member that gives a gift. The Corporation Sole is also immune from being required by law to give the donor a receipt acknowledging their gift! In this case, it is the responsibility of the donor to keep their records and NOT the Church or Corporation Sole. If your Church chooses to do so, it may voluntarily and freely (out of the kindness of its heart) give the donor a receipt acknowledging their contribution or donation.”

He did not seem to be concerned about the giver when he wrote Benefit #8. I analyzed Alleged Benefit # 8 in Chapter 2: Analysis of “Benefits of the Corporation Sole Comparedto a Traditional 501c3. Furthermore, the corporation sole church has no reason not to give an acknowledgement. It, as has been explained in this booklet several times, is a 508 church which is required to abide by the rules of 501c3.

“Making such bold argument(s) for legitimate Churches could potentially set a VERY REAL and VERY SERIOUS precedence if the Federal Government failed to make their case to a Judge or Jury. If they challenge our argument that Churches operating under the law of 26 USC 508(c)(1)(a), not the Churches subsequent and isolated Corporation Sole, can influence politics, have the Church body vote for or against political candidates, have the Church lobby congress or have the Church distribute political propaganda on behalf or against any political candidate for office (once again, the Church and NOT the 501c3 isolated Corporation Sole) and they lose, then they will potentially open the door WIDE OPEN for EVERY SINGLE CHURCH IN AMERICA to RUN to get their Corporation Sole and be FREE from the political restrictions that have plagued our Nations Churches. If they win such an argument, by the time they win we would have already freely given away our Corporation Sole support to TENS OF THOUSANDS of CHURCHES that already HATE 501c3 with a passion and are already bold enough to speak unfiltered truth behind the pulpit. This could mean EXTREME backlash from potentially millions of registered voters from members of those congregations (many of whom are EXTREMELY influential Christian business men and politicians themselves) that we’ve been training Pastors in how to lead in influencing intended Christian reforms. To make enemies with the Church as well in a political season such as this with the IRS already embroiled in scandal after scandal (from Lois Lerner lying to Congress to the IRS ‘accidentally’ destroying all hard drive evidence) or a Justice Department that fails to enforce current laws or investigate any Government agency of any wrongdoing, it would leave a VERY bad taste in the mouth of Christian voters in these Churches and would propel us to the National Spotlight (which is EXACTLY what we want, so we can make our case to Christians everywhere). It would also be extremely unwise timing as they would have underestimated the Jury’s potential disdain for the Government and their routine MANY failures, coverups and current violations to oaths of office perceived by the American public by officials in the Federal Government (this is in addition to the fact, that we will call upon the several hundred eye witnesses and VERY Charismatic Pastors that will first hand testify that we’re a Church). Any one person being on that Jury that is either a Republican or Christian WILL side with us. This would give the Church a HUGE edge in court. Either way, wisdom would see that such a challenge (if ever) given by the Government based on these merits would end up being a lose/lose situation for them.”

Church Freedom and the Corporation Sole has already lost because your scheme is not according to the Bible and not according to the law. Your incorporated 508 church is subject to the rules of 501c3. That has already been covered in this booket. Since the IRS does not have the resources to deal with every state church who is violating the rules of 501c3, they are not enforcing the law. You are grieving the Lord by organizing a state church (a legal entity). You did not have to so organize, but you did. You then try to twist the law to conform to your vision. The main thing is that your authority is the state. If the IRS wishes to take your church(es) to court for alleged violations of the rules that come with 501(c)(3), they can. They have authority over you. Christ does not wish His authority over His churches to be shared with anyone. Old Paths Baptist Church Separation of Church and State Law Ministry helps churches remain under God only. We can do this because we correctly understand Bible principle and law.

“This is WHY we do whatever it takes to freely give our support to as many qualified approved Churches in the shortest time as humanly possible. Officials should know and understand that while other unscrupulous Corporation Sole peddlers have fallen to greed and tried to sell the Corporation Sole away as a mere tax shelter, we have not. We ABSOLUTELY NEVER give our support to individuals or entities looking to create a tax shelter. If a person cannot get at least 4 living people over the age of 21 that are willing to sign an affidavit under the penalties of perjury that they are a bona fide Church that lives up to the IRS’s own 14 point test, then we deny their application immediately. We’ve denied more applications than anyone knows with individuals trying to offer us everything you can think of for access to our support and we’ve denied ALL OF THEIR ATTEMPTS. If we even remotely smell someone coming that gives us the impression that they are either an individual trying to evade lawful taxes owed or an undercover informant trying to entrap us with promises of money, power or prestige for giving them our ministry and Corporation Sole support, we not only deny their application but we also permanently prohibit their access to our website by blocking their unique IP address. We ONLY work with legitimate BONA FIDE Churches.”

Church Freedom and the Corporation Sole needs to study these matters out and trash their ill-conceived ideas and schemes. They are not according to knowledge, as this booklet has made perfectly clear.

“This is why we need your help to spread the word about ChurchFreedom.org! We want to freely help support EVERY SINGLE Christian Church here in America. With your help, we’ve been able to directly support over 2,000 new Christian Churches this year alone. With your help, we can help FREE America’s Churches from 501c3 entirely.”

If Church Freedom and the Corporation Sole loves the Lord, then they need to study, grow in knowledge, understanding, and wisdom and repent. They need to contact all the churches they have helped, ask forgiveness, let them know the truth, and encourage them to trash their Affidavits, dissolve their corporations and organize according to Bible principles.

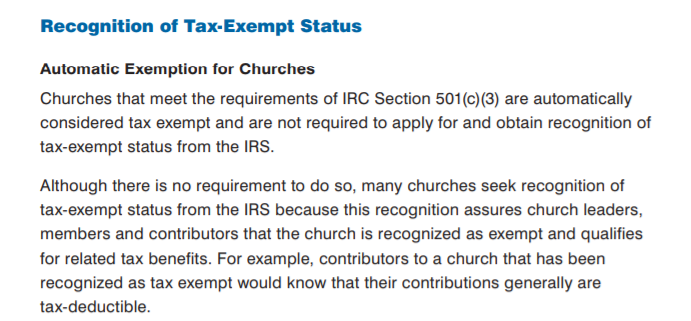

Notice that the above featured image, taken from IRS publications given below, says, “churches that meet the requirements of § 501(c)(3) are automatically considered tax exempt and are not required to apply for and obtain recognition of tax-exempt status from the IRS.” This is the correct position.

According to 508(c)(1)(A) a church can claim status without filing for 501(c)(3) status. 508(c)(1)(A) is a subsection of §508. Special rules with respect to section501(c)(3) organizations; this alone makes clear that a 508(c)(1)(A) church is a 501(c)(3) church. As such, it is subject to the requirements (the rules and regulations) that come with 501(c)(3). This conclusion is further explained in this article.

Furthermore, according to principles in the Word of God, church tax exempt status is spiritual fornication since she has submitted herself to man’s law, become a temporal legal – as opposed to spiritual eternal only – entity, and chosen to submit to an authority other than the Lord Jesus Christ as to many church matters.

A church can choose to remain under Christ only as a eternal spiritual organism as opposed to a temporal earthy organization. In America, the First Amendment and corresponding state constitutional provisions protect this choice from persecution. The essay below, and other essays, articles, and books on this website explain these matters more comprehensively.

Ignorance, and especially willful ignorance, is no excuse for dishonoring our Lord.

Click the above to go to online version of God Betrayed.

In the book God Betrayed/Separation of Church and State: The Biblical Principles and the American Application (“God Betrayed”) as well as in other books and writings, I originally taught that a New Testament church could depend upon Internal Revenue Code (“IRC”) § 508(c)(1)(A) for her non-taxable status (See Endnote 1for links to the two free versions of God Betrayed or for ordering information should you desire a softback copy as well as information on other books and resources by Jerald Finney.). I was wrong. After years of study, I have learned that a New Testament church cannot depend upon 508(c)(1)(A) for her non-taxable status because, in so doing, the church gives up her New Testament and First Amendment status; the church becomes tax exempt as opposed to non-taxable. However, I am more certain than ever of the correctness of my original biblically based conclusions that a church grieves the Lord when they intentionally, knowingly, recklessly, or negligently attain church corporate and/or 501(c)(3)/508(c)(1)(A) status or legal entity status (See Endnote 1) of any kind. I ask those who have followed my teachings to forgive me for misleading them concerning church 508 status. This brief article explains church 508 status and its effect.

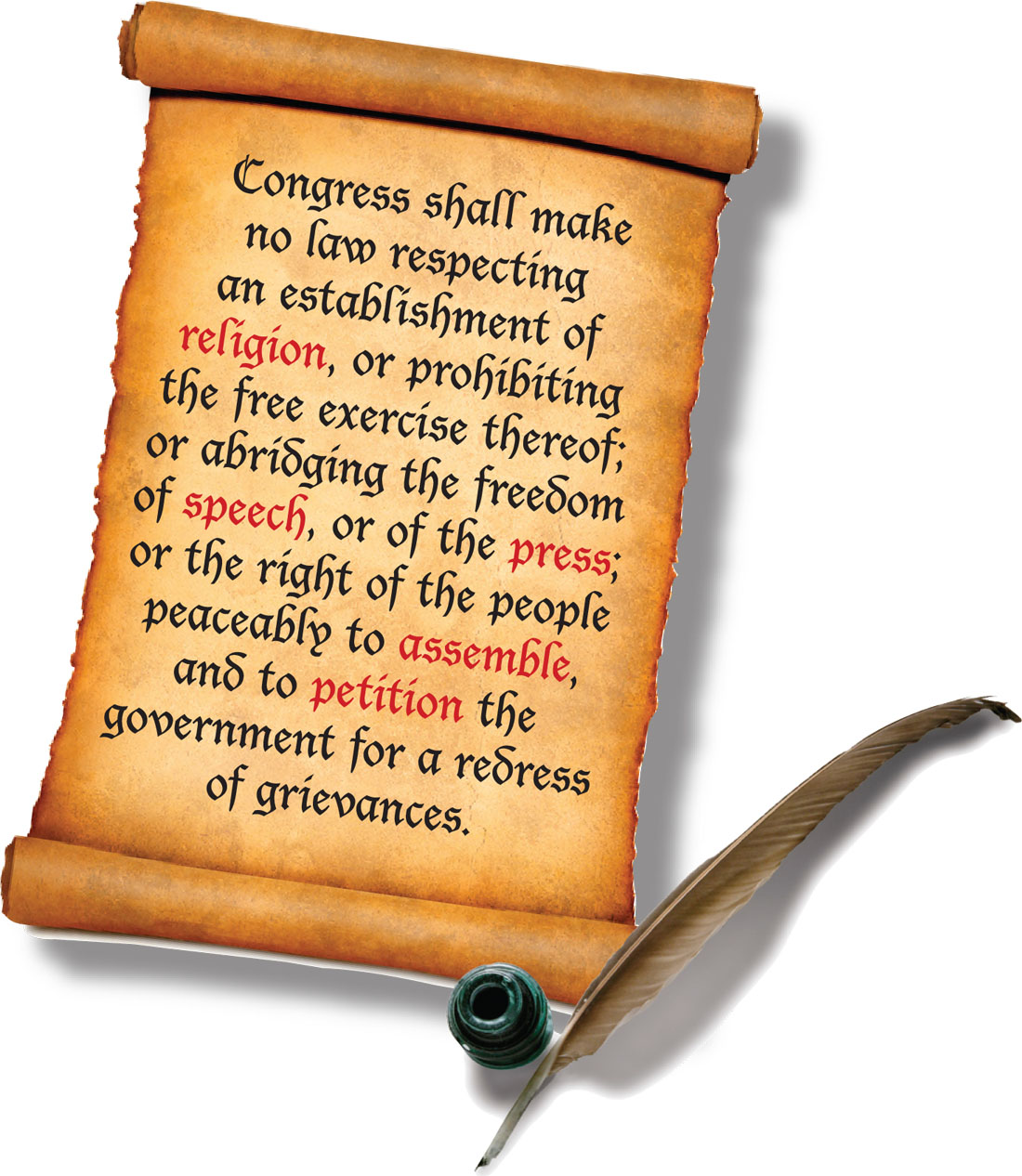

A New Testament Church is also a First Amendment Church. This is because the First Amendment is a law which corresponds with biblical principles to include freedom of religion and conscience (separation of church and state), freedom of speech, freedom of press, and freedom of association. The First Amendment is a part of the second highest law of the land, the United States Constitution.

“Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the Government for a redress of grievances.”

Notice especially that the First Amendment says, “… no law ….”

Are not those words very clear? No law means “no law.” What is IRC § 508(c)(1)(A)? It, like IRC 501(c)(3), is a law made by Congress and signed by the President. IRC § 508(c)(1)(A) and IRC 501(c)(3) are, when applied to churches, laws “respecting an establishment of religion and preventing the free exercise thereof.”

Why would a church take themselves from First Amendment status and protection to either IRC § 508(c)(1)(A) or IRC § 501(c)(3)? One reason is lack of knowledge, wisdom, and understanding. When a church claims either 508(c)(1)(A) or 501(c)(3) status, she has rejected her First Amendment non-taxable status and freely accepted the offer of the federal government to enter into an agreement (contract) for tax exempt status as provided by a law.

Let me repeat: First Amendment churches under God are non-taxable. 501(c)(3) and 508(c)(1)(A) religious organizations are tax exempt. IRC § 508 (the codification of Public Law 91-172 ratified in 1969) provides in relevant part:

A portion of Internal Revenue Code § 508. Click the above to go to § 508.

“§ 508. Special rules with respect to section 501(c)(3) organizations. “(a) New organizations must notify secretary that they are applying for recognition of section 501(c)(3) status. … “(c) Exceptions. “(1) Mandatory exceptions. Subsections (a) and (b) shall not apply to— “(A) churches, their integrated auxiliaries, and conventions or associations of churches” (26 U.S.C. § 508). [Emphasis mine.]

§ 508(c)(1)(A) says churches are excepted from applying for IRC § 501(c)(3) tax exempt status (See Endnote 2for links to articles which fully explain church IRC § 501(c)(3)) status). 508 churches are an exception to the civil government requirement that certain organizations file for 501(c)(3) tax exempt status.

A church should rely on the First Amendment to the United States Constitution, not on508(c)(1)(A) status for three reasons. First, the First Amendment is a statement of the biblical principle of separation of church and state (See, for a short explanation with links to more in depth studies, Is Separation of Church and State Found in the Constitution?). When a church relies on the First Amendment, they are relying on a biblical principle. Should the biblical principle be abused or ignored by the civil government, so be it—a church should then rely and act only on the biblical principle. Endnote 3.

A law of man which enacts some biblical principles.

Second, to rely on 508(c)(1)(A) contradicts the First Amendment. To repeat, the First Amendment religion clause states:

“Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the Government for a redress of grievances.”

IRS Publication 1828. Click the above to go directly to IRS Pub. 1828.

Obviously, 508(C)(1)(A) is a law made by Congress which regards an establishment of religion; 508(C)(1)(A) also prevents the free exercise of religion because a church which claims 508(C)(1)(A) status thereby submits themselves to some control by the federal government in that the church becomes subject to the rules that come with IRC 501(c)(3) status. 508(C)(1)(A) does not state that the First Amendment forbids Congress from making any law in violation of the First Amendment; and that, therefore, a church is non-taxable. 508(C)(1)(A) is a law made by Congress which states that Congress, by law, is declaring an exemption for churches. Thus, by a clear reading of the First Amendment, 508(C)(1)(A) is clearly unconstitutional. Most churches and pastors could care less about this technicality.

From IRS Publication 1828

The correct position which is held by the Internal Revenue Service (“IRS”) is that a church has submitted herself to IRC § 501(c)(3) regulation and ignored her First Amendment status by relying on 508(C)(1) (a law passed by Congress) instead of the First Amendment. The IRS makes this position clear. Page 3 of IRS Publication 1828 states that “churches that meet the requirements of § 501(c)(3) are automatically considered tax exempt and are not required to apply for and obtain recognition of tax-exempt status from the IRS” [Bold red emphasis mine]. The IRS repeats this on page 24 of IRS Publication 557, “Tax –Exempt Status for Your Organization.” Under Organizations Not Required To File Form 1023 churches are listed. The following sentence is included: “These organizations are exempt automatically if they meet the requirements of section 501(c)(3).” [Bold red emphasis added.]

IRS Publication 557, p. 24. Click the image to go directly to the publication.

One should also understand that the New Testament (First Amendment) church will not be involved with the IRS for several reasons: the church claims no 501(c)(3) or 508(c)(1)(A) status; is not a legal entity such as a corporation aggregate or sole, an unincorporated association, or a charitable trust; is not a business; has no income; has no employees or staff; has no constitution or by-laws; and, no matter what the particular civil government does, honors the biblical principle of separation of church and state which is reflected in the First Amendment in America.

The New Testament (First Amendment) church who loves the Lord will be prepared for the eventuality that the Internal Revenue Service, some other Federal agency, the President (recent presidential actions and orders as well as the actions of many prior presidents demonstrate what a tyrannical president can and will do), and/or the Supreme Court of the United States may someday misinterpret and apply the First Amendment; and a New Testament church, who loves the Lord and is committed to pleasing Him, will remain submitted to the higher authority. God Betrayed (see above for free links to the book) explains all this and also shows how churches are operating in America without becoming legal entities such as incorporated 501(c)(3) religious organizations thereby retaining their First Amendment and biblical status. For specifics on how to organize a church under the Bible principle of separation of church and state, one can also go to: The CUCM Bible Trust.

Third, a New Testament church (a church organized according to the principles of the New Testament), among other things, receives no income, is not a 501(c)(3) or 508 religious organization, has no constitution or by-laws, has no employees or staff, and runs no businesses (daycare controlled or licensed by the state, “Christian” schools, “Bible” colleges, seminaries, cafes, etc.). Church members of a New Testament Church give their tithes and offerings to God, not to a religious organization, for use in ways consistent with New Testament teaching. All monies given to God are disbursed in accordance to the guidelines of the New Testament, and no money is left over. Let us use our common sense, if not our biblical sense: Even a business which makes no profit pays no taxes. A church which has no income cannot be taxed. A church which does have net income should be taxed since (1) she is operating as a business and not as a New Testament church; and (2) (if she is a legal entity such as a non-profit corporation (includes corporation sole – see Critique of “Church Freedom and the Corporation Sole” Website), or unincorporated association she is set up as a non-profit religious organization and therefore violates not only biblical principles for the organization of a church but also her non-profit agreements with the state of incorporation by making a profit.

Uncle Sam Wants God’s Churches

If a church does not apply for 501(c)(3) tax exempt status or claim 508(c)(1)(A) tax exempt status, and if she is organized as a New Testament church, according to the First Amendment which agrees with the biblical principle of separation of church and state, the non-taxable status of that church must be honored. A church claims 508(c)(1)(A) status by giving IRS acknowledgements for tithes, offerings, and gifts. No matter what the civil government claims, a church who has no income cannot be taxed; she gives her tithes, offerings, and gifts to God, not to a government created religious organization. Said another way, the church (the members) give to God, not to the church, inc. or the church (an unincorporated association).

Always keep in mind matters which I cover in detail in other writings and teachings: a church who incorporates (non-profit corporation or corporation sole), or becomes a charitable trust, unincorporated association or some other type legal entity has voluntarily given up her exclusive First Amendment status in favor of partial and substantial Fourteenth Amendment status since she has become a legal entity.

There are other ways a church may violate biblical principles concerning the doctrine of the church thereby becoming some type church other than a New Testament church. Understanding these matters requires a believer to grow in knowledge, understanding, and wisdom through dedicated Bible study.

If a church successfully applies for 501(c)(3) status or claims 508(c)(1)(A) exempt status, the government is granted some jurisdiction over the church since the civil government now, by law, declares and grants an exemption.

Please, God’s dear churches, do not lose your New Testament status by becoming a legal entity of any kind. Please learn to love the Lord as he loves you and gave Himself for you;

“That he might sanctify and cleanse it with the washing of water by the word. That he might present it to himself a glorious church, not having spot or wrinkle, or any such thing; but that it should be holy and without blemish” (Ephesians 5.25-27).

Please, dear believer, learn to think Biblically (spiritually), not practically from the human perspective (fleshly). Please become more Christian than American, more heavenly than earthly. God made clear that Christ in heaven is to be the only authority (power or head) “over all things to” His churches. Put another way, a church, the body whose feet walk and work on earth, is to be connected to only one head, Christ in heaven. A church with two heads (authorities or powers) is a monstrosity.

“And what is the exceeding greatness of his power to us-ward who believe, according to the working of his mighty power, Which he wrought in Christ, when he raised him from the dead, and set him at his own right hand in the heavenly places, Far above all principality, and power, and might, and dominion, and every name that is named, not only in this world, but also in that which is to come: And hath put all things under his feet, and gave him to be the head over all things to the church, Which is his body, the fulness of him that filleth all in all” (Ep. 1.19-23).

“Now therefore ye are no more strangers and foreigners, but fellowcitizens with the saints, and of the household of God; And are built upon the foundation of the apostles and prophets, Jesus Christ himself being the chief corner stone; In whom all the building fitly framed together groweth unto an holy temple in the Lord: In whom ye also are builded together for an habitation of God through the Spirit” (Ep. 2.19-23).

“And he is the head of the body, the church: who is the beginning, the firstborn from the dead; that in all things he might have the preeminence” (Col. 1.18).

From the above verses, and many more that could be quoted, one sees that God desires his churches to be spiritual entities or bodies (See also, e.g., Ep. 4 and the whole book of Ep., Col., and 1 Co. 12 for more on churches as spiritual bodies) connected to their only God ordained Head, the Lord Jesus Christ in heaven, while walking as spiritual entities only here on the earth. Churches are to be “builded together for an habitation of God through the Spirit,” not built together as a corporate 501(c)(3) or 508 organization according to man’s earthly, legal laws.

Please repent and turn from the deceits of the god of this world to the precepts of God. Please prepare for the day when believers and churches will have to choose either to lay it all down for God and for eternal reward or to lay it all up for Satan for a perceived earthly security. That day has not yet arrived for believers and churches in America, but that day appears to be fast approaching.

Endnotes

1. For the definition of and more information on “legal entity” see the index of God Betrayed/Separation of Church and State:The Biblical Principles and the American Applicationwhich is available free in PDF, in online form (no index), or which may be ordered by clicking Order information for books by Jerald Finney.

All books, except An Abridged History of the First Amendment, by Jerald Finney are available free in both PDF and online form. One may go to Order information for books by Jerald Finney should he desire to order any of the books which are in print.

Click here to go to the article “Is Separation of Church and State Found in the Constitution?”

A biblical and historical Baptist principle is that God desires separation of church and state, not separation of God and church or separation of God and state. Study Jerald Finney’s writings and/or audio teachings to discover the truth about and how to apply the principle. Finney’s teachings prove that the revisionist view of Separation of Church and State accepted without examination by most American “Christians” is false and has done great damage to the cause of Christ and to America.

Note. See links to other informative articles on federal 501(c)(3) tax exempt status at the end of this page.

Does the Word of God teach that churches in America should get Internal Revenue Code Section 501(c)(3) (“501c3”) status? What about civil law? Does American law purportedly require that churches get 501c3 status? This article will answer those questions.

Since you will probably want to know something about Jerald Finney before you give any consideration to his positions, this article will begin by providing you with a brief profile of Finney. At the end of the article are links to important Internal Revenue Code laws concerning churches as well as an important note.

The author is a Christian first and a lawyer second. He has no motive to mislead you. In fact, his motivation is to tell you the truth about this matter, and he guards himself against temptation on this and other issues by doing all he does at no charge. He does not seek riches. His motivation is his love for God first and for others second. His goal is the Glory of God. Jerald Finney has been saved since 1982. God called him to go to law school for His Glory. In obedience, Finney entered the University of Texas School of Law in 1990, was licensed and began to practice law, for the Glory of God, in November of 1993. To learn more about the author click the following link: About Jerald Finney.

The Bible makes clear that God desires that Christians love Him and He tells them what it means to love God. The relationship between God and his children is very important to Him. Likewise, the love relationship between God and His churches is preeminent to Him. After all, “Christ loved the church and gave himself for it” (Ep. 5:25). Do you understand God’s definition of love? Jerald Finney has covered this subject in the booklet, The Most Important Thing: Loving God and/or Winning Souls? which is available on the Order Information on Books by Jerald Finney page of this website, and also free on this website at The Most Important Thing: Loving God and/or Winning Soulsin online form as well as inPDFform. Of course, if one loves God, he will win souls.

The author realizes that there are different interpretations of Scripture on any given subject—there are false interpretations and one true interpretation. Christians, including the author, should do everything possible to make sure they correctly divide Scripture since the Bible commands them to do so. In fact, the biblical way for a Christian to make sure that he is right about an issue was given to Timothy and to all Christians by Paul: “Study to shew thyself approved unto God, a workman that needeth not to be ashamed, rightly dividing the word of truth” (2 Ti. 2.15). Most Christians rely totally or heavily upon their pastors for leadership in instruction in spiritual matters. Sometimes, as is the case with the author, they rely upon their pastors and others, and are also called themselves to deal specifically with an issue.

To totally understand all the issues and sub-issues involved with the 501c3, one must not only have extensive knowledge of biblical principles, but he must also have an understanding of history and law. You see, the issue of the relationship between church and state is very important to God and His Word completely explains His desired relationship. Historically, true Christians understood the importance of this relationship, and they stood up for their relationship even though they suffered greatly for their stand on this issue—they were imprisoned, drowned, beheaded, burned at the stake, hung, tortured, etc. because they loved their Savior and were willing to do all that He asked them to do.

With that said, let us now go to the issues—first the issue of the truth about civil government requirement that churches get 501c3 status. The unabashed truth is that civil government does not require churches in America to get 501c3 status. They do so completely voluntarily, just as they incorporate on a voluntary basis. Since there is absolutely no law that requires a church to get 501c3 status, no attorney, pastor, or anyone else can show you such a law.

Click the above to go to the article, “Is Separation of Church and State Found in the Constitution?

In fact, there is a law that clearly states that you do not have to get 501c3 status: The First Amendment to the United States Constitution. The First Amendmentto the United States Constitution prohibits the making of any lawrespecting an establishment of religion, impeding the free exercise of religion, abridging the freedom of speech, infringing on the freedom of the press, interfering with the right to peaceably assemble or prohibiting the petitioning for a governmental redress of grievances. It was adopted on December 15, 1791, as one of the ten amendments that constitute the Bill of Rights. The First Amendment states, “Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the Government for a redress of grievances.“

When I first wrote this article, I stated thatInternal Revenue Code § 508 (“508”) is a law that protects churches and states that churches are an exception to getting 501c3 status. That law explicitly states that churches are an exception to the requirement that certain organizations get 501c3 status. However, after years of study, I am convinced that a church should never claim 508 status. A church should rely on the First Amendment to the United States Constitution, not on 508.

508 is a law made by the federal government that regards and establishment of religion and prevents the free exercise thereof. Therefore, a church that agrees to 508 status has agreed to place herself under a law which is unconstitutional as applied to churches (a law which violates the First Amendment when applied to churches) thereby waiving First Amendment status and also weakening the First Amendment. The federal government can also argue that churches who claim 508 status have agreed to the rules of 501c3, since the state may argue that the federal government is granting the exemption under 508 and the church chose to depend upon 508 instead of the First Amendment. The Internal Revenue Service completely understands the First Amendment implications as to churches. The Internal Revenue Service states in Internal Revenue Code Publication 1828: “Unlike churches, religious organizations that wish to be tax exempt generally must apply to the IRS for tax-exempt status unless their gross receipts do not normally exceed $5,000 annually.” One may argue that this interpretation of 508 is too explicit, but the devil is in the details, and the legal system is expert in arguing the details. See, for more thorough explanation, Church Internal Revenue Code § 508 Tax Exempt Status.

A 501c3 church also has many regulations which it is required to honor. See Publication 4221: Compliance Guide for Tax Exempt Organizations(“Federal tax law provides tax benefits to nonprofit organizations recognized as exempt from federal income tax under section 501(a) of the Internal Revenue Code (the Code). The Code requires that tax-exempt organizations comply with federal tax law to maintain tax-exempt status and avoid penalties….”).

In spite of the irrefutable fact that churches are not required to get 501c3, many Christians will tell you that Romans 13 requires that churches get 501c3 status. Of course, that is a ridiculous statement, since American law clearly gives each church a choice in the matter. No “ordinance of man” requires churches to get 501c3; therefore, churches cannot violate an ordinance which does not exist. To repeat, does God require that a church get 501c3? Of course not, and no “ordinance of man” purportedly requires man to get 501c3.

Another important question, although not at all relevant (as we have seen) to the issue of whether churches in America are required to get 501c3, is this: “If God is against a church obeying a certain civil law, even if the civil law purportedly requires churches to obey that law, is man to obey the civil law?” When one does an honest and systematic biblical study of the issues involved, the answer becomes very clear. The author has done such a study and has written and taught on this very issue. He has written four books that cover the biblical principles as well as history and law. Again, those books are available free on this website in online form as well as in PDF form or may be ordered in paperback. See Order information, free PDF, and free online version page for books by Jerald Finney.

This article will just mention a few Biblical principles and teachings. Clearly, when a man-made law conflicts with God’s law, Christians are instructed by God to obey God’s law. All the apostles, except John, were martyred for adhering to this principle. Likewise, as mentioned above, Christians down through the ages in and since the primitive church have stood on this principle.

The Bible teaches that God is sovereign over all, and that He ordained all powers that be. Thus, God established or ordained civil government. He gave civil government the responsibility for ruling over men, under Him. He also gave man free will. Since civil government is run by a man, or by men, civil government, like man, is free, under God to honor or dishonor Him and His principles. Of course, God desires that civil government honor Him, but sadly, civil governments rarely do so, and they never permanently do so in this age. This is the clear teaching of history.

To interpret Romans 13 and other verses to mean that Christians are to obey all civil laws which contradict God’s law would mean that Romans 13 is inconsistent in both the immediate and overall context of Scripture. Many Old Testament characters, the apostles, God, God’s own angels, and Christians throughout the last 2000 years who have refused to honor laws of men which require God’s children to submit to man rather than to proceed under God only in certain matters, violated the modern American interpretation of Romans 13. The author goes into all the details on this matter in Render unto God the Things that Are His: A Systematic Study of Romans 13 and Related Verses and in God Betrayed/Separation of Church and State: The Biblical Principles and the American Application (The book is in online form atRender unto God the Things that Are His: A Systematic Study of Romans 13 and Related Verses. Also, click the following links for other articles which teach on this matter: Separation of Church and God, American Abuse of Romans 13:1-2, An Abridged History of the First Amendment.

In conclusion, churches who get 501c3 dishonor the Lord and His principles concerning His desired relationship between church and state. Christians are responsible to God to study His Word and make the practical application of His Word to real life. The relationship between Christ and His churches is very important to Him: “Husbands, love your wives, even as Christ also loved the church, and gave himself for it; That he might sanctify and cleanse it with the washing of water by the word, That he might present it to himself a glorious church, not having spot, or wrinkle, or any such thing; but that it should be holy and without blemish” (Ep. 5.25-27).

That relationship has been so important to Christians since the beginning of the Church that they have been willing to die rather than to dishonor it. How important is that relationship to you and your church?

You can read the following Internal Revenue Code laws online by clicking the following links:

1.§ 501(c)(3). Exemption from tax on corporations, certain trusts, etc. 2.§ 508. Special rules with respect to section 501(c)(3) organizations 3.§ 7611. Restrictions on church tax inquiries and examinations 4.§ 1402. [Dealing with taxes on income of pastors] 5.§ 107. Rental value of parsonages 6.§ 102. Gifts and inheritances (According to Internal Revenue Code § 102tithes and offerings are gifts and, therefore, , not income) 7.§ 2503. Taxable gifts 8.§ 170. Charitable, etc., contributions and gifts

Note. Should you desire to know how your church can organize according to both biblical principles and also within the parameters of American law contact Jerald Finney, a licensed lawyer. Click here for contact information for Jerald Finney.

All conclusions in this article are opinions of the author. Please do not attempt to act in the legal system if you are not a lawyer, even if you are a born-again Christian. Many questions and finer points of the law and the interpretation of the law cannot be properly understood by a simple facial reading of a civil law. For a born-again Christian to understand American law, litigation, and the legal system as well as spiritual matters within the legal system requires years of study and practice of law as well as years of study of Biblical principles, including study of the Biblical doctrines of government, church, and separation of church and state. You can always find a lawyer or Christian who will agree with the position that an American church should become incorporated and get 501(c)(3) status. Jerald Finney will discuss the matter, as time avails, with any such person, with confidence that his position is supported by God’s Word, history, and law. He is always willing, free of charge and with love, to support his belief that for a church to submit herself to civil government in any manner grieves our Lord and ultimately results in undesirable consequences. He does not have unlimited time to talk to individuals. However, he will teach or debate groups, and will point individuals to resources which fully explain his positions.

The Truth About Frivolous Tax Arguments – Section II; Termination of Exempt Organization (“… Internal Revenue Code Section 6043(b) and Treasury Regulations Section 1.6043-3 establish rules for when a tax-exempt organization must notify the IRS that it has undergone a liquidation, dissolution, termination, or substantial contraction. Generally, most organizations must notify the IRS when they terminate. Among other things, notice to the IRS of a termination will close the organization’s account in IRS records. …)

Click the image above to go to the article “Is Separation of Church and State Found in the Constitution?”

Preliminary note. The author has made significant revisions to this article as his knowledge grows with continued study. The original title to the article, “Laws Protecting New Testament Churches: Read Them for Yourself,” was changed to “First Amendment Protection of New Testament Churches/Federal Laws Protecting State Churches (Religious Organizations)” on July 13, 2015.

You can always find a lawyer or Christian who will agree with the position that an American church should become a religious organization by becoming a legal entity such as a non-profit corporation (included corporation sole), unincorporated association, charitable trust, etc. and get 501(c)(3) or 508 status. Jerald Finney will discuss the matter, as time avails, with any such person, with confidence that his position is supported by God’s Word, history, and law. He is always willing, free of charge and with love, to support his belief that for a church to submit herself to civil government in any manner grieves our Lord and ultimately results in undesirable consequences. He does not have unlimited time to talk to individuals. However, he will teach or debate groups, and will point individuals to resources which fully explain his positions.

You may go directly to a link (letters in maroon), or, to save time, you may read only the relevant portions of a provision or law which are in the article below.

Virginia Passes Legislation Forcing Churches to Allow “Transgender” Males into Women’s Bathrooms(04720)(Of course, this will be contested in court. Regardless of the outcome of such contest(s), keep in mind that the established church (incorporated, 501(c)(3) or 501(c)(1)(A) churches have voluntarily given up much of their First Amendment protections and placed themselves under the 14th Amendment for many purposes. Churches who choose to remain under the First Amendment for all purposes are not subject to state legislation. Contact this Churches under Christ Ministry for more information.)

Contents:

Note. At the very end is an excellent Facebook comment on “What happens if we abuse liberty” by Herei Stand on October 16, 2015.

I. Introduction II. The Highest Law: God’s Law III. United States Law: Man’s Law A. The First Amendment to the United States Constitution B. The Internal Revenue Service Code 1.§ 501(c)(3). Exemption from tax on corporations, certain trusts, etc. 2.§ 508. Special rules with respect to section 501(c)(3) organizations 3.§ 7611. Restrictions on church tax inquiries and examinations 4.§ 1402. [Dealing with taxes on income of pastors] 5.§ 107. Rental value of parsonages 6.§ 102. Gifts and inheritances (According to Internal Revenue Code § 102tithes and offerings are gifts and, therefore, , not income) 7.§ 2503. Taxable gifts 8.§ 170. Charitable, etc., contributions and gifts

The author is completely aware that most “Christians” and “Christian” lawyers tell churches to incorporate, get 501(c)(3) or 508 status or to become a legal entity in some other manner. The author takes issue with those lawyers and Christians and has written and taught extensively on the God-given principles concerning church and state and the application of those principles in America.

Those of you who do not know the author cannot be expected to trust him. Therefore, in order that a Christian can see for himself what the law says, this article will lay out the law which protects New Testament (the First Amendment) churches, and the laws which allegedly protect state churches. The First Amendment (quoted below) says that Congress shall make “no law” as to certain matters. Yet, 501(c)(3) (and 508) is a law which does exactly what the First Amendment forbids, as to churches. When a church submits herself to either of those laws, she becomes a religious organization (according to the explicit words in those laws) and subjects herself to the rules that come with those laws. The federal government, specifically the Internal Revenue Service, becomes sovereign of a 501(c)(3) or 508 church for certain purposes and enforces the rules that come with 501(c)(3) at its discretion; indeed, as will be seen, the IRS can add rules, having already added one rule which was contested and upheld the Supreme Court. Having succumb to the sovereignty of the federal government for some purposes through willing submission to 501(c)(3) law, the federal government added other laws to the Internal Revenue Code to protect religious organizations to a degree from arbitrary actions by the Internal Revenue Service.

A church which is a legal entity such as in incorporated church and or which gets Internal Revenue Code Section 501(c)(3) status loses much of her First Amendment protection and places herself under the Fourteenth Amendment to a large degree; the author fully explains this in his teachings on this website. One can go directly online to the laws in their entirety by clicking the blue underlined links.

In case you are not aware of it, an American church can operate as a spiritual entity only, under the First Amendment, without persecution, under God as a non-legal entity (as a spiritual entity) instead of a legal entity such as a non-profit corporation, charitable trust, unincorporated association, or corporation sole and without Internal Revenue Code Section (“IRC”) 501(c)(3) (“501(c)(3)” or Section 508 (“508”) status.FN1

New Testament churches are protected, for the time being, by the First Amendment which is a statement of Bible principle and, therefore, in line with God’s law. State churches and other religious organizations – the protection of the First Amendment and God not being enough for them to attain their worldly temporal goals (they think) – have turned to laws which contradict the First Amendment for protection. In so doing, they have shunned the protection of God and the First Amendment for many purposes. The chickens are coming home to roost.

II. The Highest Law: God’s Law

Of course, the highest law that protects churches everywhere, including churches in America, is God’s law as laid out in His Word. Although, in many nations, churches who wish to operate under God only will suffer persecutions, including physical death, for honoring God and His principles of organization and operation, no civil government can take the life or liberty of a true Christian or destroy a true church. The author has done a complete systematic study God’s principles concerning church and state in his other works.FN2

No nation gives anyone or any church life or liberty. Nations choose whether to protect the God-given life and liberty of individuals and churches from persecution.

God, the highest authority, establishes His churches and gives life to believers only:

“And I say also unto thee, That thou art Peter, and upon this rock I will build my church; and the gates of hell shall not prevail against it” (Matthew 16:18).

“He that hath the Son hath life; and he that hath not the Son of God hath not life” (1 John 5:12).

“While we look not at the things which are seen, but at the things which are not seen: for the things which are seen are temporal; but the things which are not seen are eternal. For we know that if our earthly house of this tabernacle were dissolved, we have a building of God, an house not made with hands, eternal in the heavens. For in this we groan, earnestly desiring to be clothed upon with our house which is from heaven: If so be that being clothed we shall not be found naked. For we that are in this tabernacle do groan, being burdened: not for that we would be unclothed, but clothed upon, that mortality might be swallowed up of life. Now he that hath wrought us for the selfsame thing is God, who also hath given unto us the earnest of the Spirit. Therefore we are always confident, knowing that, whilst we are at home in the body, we are absent from the Lord: (For we walk by faith, not by sight:) We are confident, I say, and willing rather to be absent from the body, and to be present with the Lord.” (2 Corinthians 4.18; 5.1-6, 7-8; See also, Romans 8.18-25.).

Additionally, only Christ gives liberty to believers, and only to believers who continue in His Word:

“The Spirit of the Lord is upon me, because he hath anointed me to preach the gospel to the poor; he hath sent me to heal the brokenhearted, to preach deliverance to the captives, and recovering of sight to the blind, to set at liberty them that are bruised” (Luke 4:18).

“Then said Jesus to those Jews which believed on him, If ye continue in my word, thenare ye my disciples indeed; And ye shall know the truth, and the truth shall make you free” (John 8:31-32).

“If the Son therefore shall make you free, ye shall be free indeed” (John 8:36).

“Being then made free from sin, ye became the servants of righteousness” (Romans 6:18).

“But now being made free from sin, and become servants to God, ye have your fruit unto holiness, and the end everlasting life” (Romans 6:22).

“For the law of the Spirit of life in Christ Jesus hath made me free from the law of sin and death” (Romans 8:2).

“Because the creature itself also shall be delivered from the bondage of corruption into the glorious liberty of the children of God” (Romans 8:21).

“For he that is called in the Lord, being a servant, is the Lord’s freeman: likewise also he that is called, being free, is Christ’s servant” (1 Corinthians 7:22)

“For though I be free from all men, yet have I made myself servant unto all, that I might gain the more” (1 Corinthians 9:19).

“Now the Lord is that Spirit: and where the Spirit of the Lord is, there is liberty” (2 Corinthians 3:17).

“And that because of false brethren unawares brought in, who came in privily to spy out our liberty which we have in Christ Jesus, that they might bring us into bondage” (Galatians 2:4).

“So then, brethren, we are not children of the bondwoman, but of the free” (Galatians 4:31).

“Stand fast therefore in the liberty wherewith Christ hath made us free, and be not entangled again with the yoke of bondage” (Galatians 5:1).

“For, brethren, ye have been called unto liberty; only use not liberty for an occasion to the flesh, but by love serve one another” (Galatians 5:13).

“But whoso looketh into the perfect law of liberty, and continueth therein, he being not a forgetful hearer, but a doer of the work, this man shall be blessed in his deed” (James 1:25).

“While they promise them liberty, they themselves are the servants of corruption: for of whom a man is overcome, of the same is he brought in bondage” (2 Peter 2:19).

Christians are to walk in the spirit, not in the flesh.(See, e.g., 1 Corinthians 2; 3.1-3; Galatians 5, Romans 6-8). Most do not. New Testament churches are spiritual organisms, not earthly entities. Thus, an incorporated, 501(c)(3) or 508 church has violated God’s principles by placing herself, at least partially, under a head other than the Lord Jesus Christ. For systematic studies of all the arguments used to justify submission of individuals and churches to civil government see FN3.

The Martyrs of the faith clearly understood the liberty given them by Jesus Christ.

A. The First Amendment to the United States Constitution