The title to IRC § 508(c)(1)(A) makes clear that a 508 church is a 501(c)(3) church. She, like all 501(c)(3) churches, is a spiritual whore. The 508 church is an exception to the requirement for filing for tax-exempt status. She becomes tax-exempt by agreeing (whether she knows it or not) to give IRS acknowledgements for tithes, offerings, and gifts to the donors and by abiding by the other 501(c)(3) rules and regulations.

A church who claims the status and states that she is not a 501(c)(3) church, but does not abide by all the rules and regulations that come with 501(c)(3) is guilty whether she knows it or not. Ignorance of the law is no defense. The wife who commits adultery is guilty whether she gets found out or not. The church, the wife of Christ, who commits adultery is guilty, and she cannot deceive the Lord. Her Husband knows and grieves over her harlotry. The church has started to spiritually slide downward. She is also a hypocrite whether she knows it or not and whether the IRS or other government agency takes action or not.

The 501(c)(3) status of the 508(c)(1)(A) church is not hidden because it is in clear view. It is stated in the title to IRC § 508(c)(1)(A). The following statement of the law (in relevant part) can be verified by a simple google search using search terms such as “irs code 508.”

Copy and paste of 508(c)(1)(A):

Ҥ 508. Special rules with respect to section 501(c)(3) organizations.

“(a) New organizations must notify secretary that they are applying for recognition of section 501(c)(3) status.

…

“(c) Exceptions.

“(1) Mandatory exceptions. Subsections (a) and (b) shall not apply to “(A) churches, their integrated auxiliaries, and conventions or associations of churches.”[1]

[Bold emphasis in mine.]

To repeat, the title states, “§ 508. Special rules with respect to section 501(c)(3) organizations.” That should end any argument that the 508 church is not a 501(c)(3) church.

The title clearly says that 508(c)(1)(A) churches are 501(c)(3) churches. It further states that they are mandatory exceptions to the requirement for filing for 501(c)(3) status. It says that churches are excepted from filing for 501(c)(3) status in order to claim that status. That status comes with rules and regulations.

The Internal Revenue Service correctly understands church 508 status. Revenue Publication 1828 states:

“Tax-Exempt Status “Churches and religious organizations, like many other charitable organizations, qualify for exemption from federal income tax under IRC Section 501(c)(3) and are generally eligible to receive tax-deductible contributions. To qualify for tax-exempt status, the organization must meet the following requirements (covered in greater detail throughout this publication):

“the organization must be organized and operated exclusively for religious, educational, scientific or other charitable purposes;

“net earnings may not inure to the benefit of any private individual or shareholder;

“no substantial part of its activity may be attempting to influence legislation;

“the organization may not intervene in political campaigns; and

“the organization’s purposes and activities may not be illegal or violate fundamental public policy.

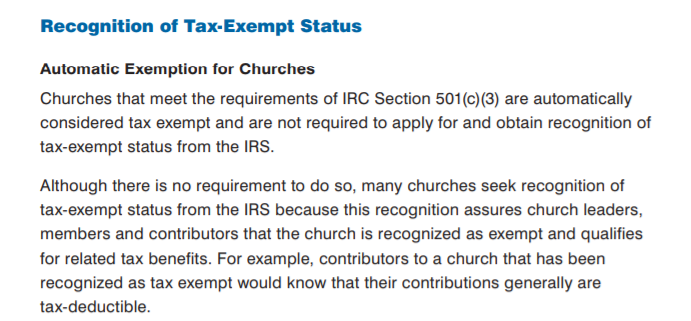

“Recognition of Tax-Exempt Status “Automatic Exemption for Churches “Churches that meet the requirements of IRC Section 501(c)(3) are automatically considered tax exempt and are not required to apply for and obtain recognition of tax-exempt status from the IRS. Although there is no requirement to do so, many churches seek recognition of tax-exempt status from the IRS because this recognition assures church leaders, members and contributors that the church is recognized as exempt and qualifies for related tax benefits. For example, contributors to a church that has been recognized as tax exempt would know that their contributions generally are tax-deductible.” [Bold italicized emphasis added].

“IRS Publication 557, Tax –Exempt Status for Your Organization.” states, in relevant part, on page 24:

“Organizations Not Required to File Form 1023 or Form 1023-EZ “Some organizations aren’t required to file Form 1023 or 1023-EZ. “These include: “Churches, interchurch organizations of local units of a church, conventions or associations of churches, or integrated auxiliaries of a church, such as a men’s or women’s organization, religious school, mission society, or youth group.

…

“These organizations are exempt automatically if they meet the requirements of section 501(c)(3). However, such organizations will not appear on the Tax-Exempt Organization Search list of organizations eligible to receive tax-de ductible contributions. These organizations also cannot obtain a written affirmation of their exempt status. To be included in the IRS database of exempt organizations and be eligible to receive a written determination or affirmation of exempt status, these organization must file Form 1023 or 1023-EZ.” [Bold italicized emphasis added].

If a church does not apply for 501(c)(3) tax-exempt status or claim 501(c)(3) tax-exempt status as a 508(c)(1)(A) tax exempt church by complying with the requirements of 501(c)(3); and if she is otherwise organized as a New Testament church, the First Amendment non-taxable status of that church must be honored. A church claims 508(c)(1)(A) status by giving IRS acknowledgements for tithes, offerings, and gifts and by agreeing that she will comply with all the other requirements of 501(c)(3).

A pastor or church member who states, “We are a 508 church, not a 501(c)(3) church” does not know what he is talking about. His church has entered into an shameful relationship with the federal government. His church is being untrue to both the Lord Jesus Christ and to her illicit lover.

501(c)(3) and 508(c)(1)(A) tax exempt status not only come with five government imposed rules, such status also invokes a myriad of regulations. See and read, e.g.,

The Truth About Frivolous Tax Arguments – Section II; Termination of Exempt Organization(“… Internal Revenue Code Section 6043(b) and Treasury Regulations Section 1.6043-3 establish rules for when a tax-exempt organization must notify the IRS that it has undergone a liquidation, dissolution, termination, or substantial contraction. Generally, most organizations must notify the IRS when they terminate. Among other things, notice to the IRS of a termination will close the organization’s account in IRS records. …)

Regardless of what one has been told or believes, an honest examination of the evidence proves that churches are not automatically tax exempt. See the essay below, and other resources linked to below, for proof of this conclusion. However, “Churches that meet the requirements of § 501(c)(3) are automatically considered tax exempt [under § 508(c)(1)(A)] and are not required to apply for and obtain recognition of tax-exempt status from the IRS.” This quote is from IRS publications and is the correct position. If a church does not meet the requirements of 501(c)(3) that church is not “tax exempt.”

Furthermore, according to principles in the Word of God, church tax exempt status is spiritual fornication since she has submitted herself to man’s law, become a temporal legal – as opposed to spiritual eternal only – entity, and chosen to submit to an authority other than the Lord Jesus Christ as to many church matters. A church can choose to remain under Christ only as a eternal spiritual organism as opposed to a temporal earthy organizaion. In America, the First Amendment and corresponding state constitutional provisions protect this choice from persecution. This essay, and the other essays and articles on this website explain these matters more comprehensively.

A church, because of the First Amendment, can choose either to be automatically non-taxable without any civil government control; or it can choose to be a 501(c)(3) or 508(c)(1)(A) tax exempt organization if … (explained below). No ifcan come with automatic status. Automatically means: “(with reference to a device or process) by itself with no human control.” According to that definition, churches definitely are not “automatically tax exempt.” Both 501(c)(3) and 508(c)(1)(A) tax exempt status come with IRS rules and regulations. See, The Rules and Regulations that Come with Church IRS Code Sections 501(c)(3) and 508(c)(1)(A) Tax-Exempt Status. Please let me explain.

“(a) New organizations must notify Secretary that they are applying for recognition of section 501(c)(3) status

…

“(c) Exceptions

“(1) Mandatory exceptions Subsections (a) and (b) shall not apply to

“(A) churches, their integrated auxiliaries, and conventions or associations of churches….”

508(c)(1)(A) does not state that churches are “automatically exempt.” Clearly, 508(c)(1)(A) states that churches are mandatory exceptions to the requirement for filing for Internal Revenue Code § (501)(c)(3) tax exempt status. “Churches, their integrated auxiliaries, and conventions or associations of churches” (not other types of other organizations) may claim 501(c)(3)tax exempt status without filing for it.

To claim tax exempt status under 508(c)(1)(A) instead of submitting IRS Form 1023 for tax exempt status under 501(c)(3), a church must, like a 501(c)(3) church, make clear to the public and to its members that the church is tax exempt (that givers may deduct their gifts on their income tax returns); and, like a 501(c)(3) church, give IRS Acknowledgements to givers.

Rules and regulations come with 501(c)(3) and 508(c)(1(A) tax exempt status. One cannot separate the status from attributes, rules, and regulations that go with it. The attributes, rules, and regulations of the status define the status. According to 508(c)(1)(A), a church may claim the status without filing for it. Contrary to unlearned “Christian” propaganda, churches who do so are to comply with the IRS rules and regulations that come with the status. The requirements of 501(c)(3) and 508(c)(1)(A) status are given in The Rules and Regulations that Come with Church IRS Code Sections 501(c)(3) and 508(c)(1)(A) Tax-Exempt Status.

The IRS understands this. Page 2 (the page may vary from year to year) of IRS Publication 1828 states, “churches that meet the requirements of § 501(c)(3) are automatically considered tax exempt and are not required to apply for and obtain recognition of tax-exempt status from the IRS” [Bold red emphasis mine]. The IRS repeats this on page 24 (the page may vary from year to year) of IRS Publication 557, “Tax –Exempt Status for Your Organization.” Under “Organizations Not Required To File Form 1023” churches are listed. The following sentence is included: “These organizations are exempt automatically if they meet the requirements of section 501(c)(3).” [Bold italicized emphasis added.].

By placing a church under a civil government law, either 501(c)(3) or 508(c)(1)(A), a church rejects her First Amendment non-taxable status and accepts the federal government offer for tax exempt status. Offer and acceptance are necessary for the agreement, the contract, to be completed. The First Amendment makes clear that a church may choose to retain religious freedom without persecution. IRS §§ 501(c)(3) and 508(c)(1)(A) give churches an alternative: give up First Amendment status as a non-legal entity in favor of Fourteenth Amendment status as a legal entity.

Most churches who obtain either 501(c)(3) or 508(c)(1)(A) status have already given up much of their First Amendment protection and status by submitting themselves to state non-profit incorporation law, charitable trust law, etc. Churches who are corporations, Internal Revenue Code Section 501(c)(3) or 508(c)(1)(A) tax exempt, or legal entities of any kind have forsaken higher law by submitting to authorities other than the Lord Jesus Christ.

With 508(c)(1)(A) the government declared in law that they trusted churches and “Christians,” of all people, to understand their actions and to honor their agreements. The government made it more convenient for churches, and for no other type of organization, to obtain tax exempt status. They falsely believed that Christians and churches were bound by a higher law and could be trusted to diligently honor their word.

As mentioned above, one requirement for 501(c)(3) or 508(c)(1)(A) tax exempt status is that the church give donors IRS Acknowledgements for tithes, offerings, and gifts. Should the IRS audit a donor who claimed a deduction for gifts to a church, the IRS will want the IRS Acknowledgment; and proof that the giver of the Acknowledgement was a church. If the church has 501(c)(3) status, the proof is on the IRS list of tax exempt churches. If the church has 508(c)(1)(A) status, the IRS may require the person claiming the exemption to prove that the gift was to a “church” even though they should have a copy of the IRS Acknowledgement for the gift.

To reject the offer of the federal government for “tax exempt” status, all a church must do is to reject all offers of state and/or federal government for combination with civil government (incorporation, charitable trust status, tax exempt status under 501(c)(3) or 508(c)(1)(A), or union with the state in any other way); refuse to give IRS Acknowledgements for tithes, offerings, and gifts; and make it known that the church is a First Amendment church solely under the authority of the Lord Jesus Christ.

Some Christians argue that they don’t care what the government requires in order for granting them the “benefits” of tax-exempt status. They know that their authority, the IRS, probably will not catch them since they do not have the resources to monitor churches and pastors. These Christians and churches take God out of the equation. The Lord knows all and does not honor such behavior by believers and churches. He expects his children to honor their word and their agreements which they voluntarily enter into. They are dishonoring God and man, and ignorance will not excuse their misdeeds:

“According as his divine power hath given unto us all things that pertain unto life and godliness, through the knowledge of him that hath called us to glory and virtue: Whereby are given unto us exceeding great and precious promises: that by these ye might be partakers of the divine nature, having escaped the corruption that is in the world through lust. And beside this, giving all diligence, add to your faith virtue; and to virtue knowledge; And to knowledge temperance; and to temperance patience; and to patience godliness; And to godliness brotherly kindness; and to brotherly kindness charity. For if these things be in you, and abound, they make you that ye shall neither be barren nor unfruitful in the knowledge of our Lord Jesus Christ. But he that lacketh these things is blind, and cannot see afar off, and hath forgotten that he was purged from his old sins. Wherefore the rather, brethren, give diligence to make your calling and election sure: for if ye do these things, ye shall never fall” (2 Peter 1:1-10).

Equality Act Creates LGBT Rights Everywhere!(102315)(Revealed: LGBT Nuclear Bomb Against Churches – Will apply to state churches, such as incorporated 501c3 churches, only. The article below explains how this applies to state churches, but not to New Testament churches.)

Virginia Passes Legislation Forcing Churches to Allow “Transgender” Males into Women’s Bathrooms(04720)(Of course, this will be contested in court. Regardless of the outcome of such contest(s), keep in mind that the established church (incorporated, 501(c)(3) or 501(c)(1)(A) churches have voluntarily given up much of their First Amendment protections and placed themselves under the 14th Amendment for many purposes. Churches who choose to remain under the First Amendment for all purposes are not subject to state legislation. Contact this Churches under Christ Ministry for more information.)

The article, “Christian schools will have no choice about gay marriage: Column,” again puts the ignorance of “Christians” on display. The author of the article, Michael Farris, laments the fact that the United States Supreme Court is posed to deny 501(c)(3)status to Christian colleges and even to churches which oppose same-sex “marriage” (Actually, any union outside that of a male and a female is not marriage. See Jerald Finney’s letter on the webpage “The Sodomite Agenda, Religious Organizations, And Government Tyranny.”). I limit this reply to that article to churches only, even though I could say much about so-called “Christian” schools and institutions of higher learning.

The author of the article, Michael Farris, is a good lawyer who has done much for the cause of homeschooling in America; but his article reveals that he, like most American “Christians,” has no clue as to the important Bible doctrines of church, state, and separation of church and state and their application in America (See the first three sections of God Betrayed/Separation of Church and State: The Biblical Principles and the American Applicationwhich is available free in bothonline and PDFform. The first three sections of the online version are updated. One may study the websiteSeparation of Church and State Law for articles, books and other resources concerning the issue of church organization.). Nor does he understand church incorporation law or Internal Revenue Code section 501(c)(3) as applied to churches.

“Christian colleges and churches need to get prepared. We must decide which is more important to us — our tax exemption or our religious convictions. Keep in mind, it is not the idea that the college itself might have to pay taxes that is the threat. Schools like Patrick Henry College, which I started, never run much of a profit. But since PHC refuses all government aid, all of our donations for scholarships and buildings come from tax deductible gifts. Cutting off that stream of revenue is effectively the end of such colleges absent a team of donors who simply don’t care if gifts are deductible.” [Bold red emphasis added]

Had the convictions of churches in America concerning the relationship of church and state been based upon Bible principles instead of misguided “convictions,” no church in America would have ever incorporated, applied for 501(c)(3) status or become a legal entity in any way; they would have all maintained their First Amendment status thereby remaining under God only. By the way, the First Amendment implements into the highest law of the land the principle of separation of church and state (See The History of the First Amendment or An Abridged History of the First Amendment; Is Separation Of Church And State Found In The Constitution?See also, TheTrail of Blood of the Martyrs of Jesuswhich explains not only the history of the First Amendment but also Christian and Secular revisonist history.)

Mr. Farris’ article points out something that I have pointed out for many years. He states:

“Keep in mind, it is not the idea that the college itself might have to pay taxes that is the threat. Schools like Patrick Henry College, which I started, never run much of a profit. But since PHC refuses all government aid, all of our donations for scholarships and buildings come from tax deductible gifts. Cutting off that stream of revenue is effectively the end of such colleges absent a team of donors who simply don’t care if gifts are deductible.”

“Patrick Henry College is a not-for-profit corporation created and authorized to operate under the laws of the Commonwealth of Virginia. Under Section 501(c)(3) of the Internal Revenue Code, the College is a qualified charitable institution and contributions to PHC are tax deductible to the full extent of the law.“

Patrick Henry College, like incorporated churches, is a creature of the state. The state of Virginia created the corporation and authorizes her to operate under and according to the laws of Virginia, not under the laws of God. PHC is further controlled by the federal government by the rules and regulations that go along with 501(c)(3) status. More rules can be added as shown in Bob Jones University, 461 U.S. 574; 103 S. Ct. 2017; 76 L. Ed. 2d 157; 1983 U.S. LEXIS 36; 51 U.S.L.W. 4593; 83-1 U.S. Tax Cas. (CCH) P9366; 52 A.F.T.R.2d (RIA) 5001 (1983)(See pp. 386-388 of God Betrayedfor an analysis of Bob Jones University). The college has turned to the state of Virginia and the federal government, specifically the Internal Revenue Service, for aid. The aid comes in the form of gifts given by donors who claim tax deductions for their gifts. People give for a tax deduction, not for the glory of God. In return for state aid, the non-profit 501(c)(3) organization agrees to abide by the rules and regulations, present and future, set unilaterally by their benefactor. Therefore, the statement that Patrick Henry College refuses all government aid is patently false. Churches who become non-profit corporate religious organizations and/or claim 501(c)(3) status have turned to state and the federal government for financial aid.

Churches who are not non-profit 501(c)(3) or 508(c)(1)(A) tax exempt religious organizations are not concerned about being taxed because they are non-taxable if they are correctly organized as spiritual entities only and have as their goal the glory of God. Furthermore, the First Amendment protects the non-legal status of New Testament churches. The First Amendment states:

“Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the government for a redress of grievances.”

Those churches who become legal entities place themselves under the Fourteenth Amendment for many purposes. The First Amendment guarantees that no church has to incorporate or place themselves under the rules of 501(c)(3). See, Does God and/or Civil Government Require Churches to Get 501(c)(3) Status?. One big change for a church who takes 501(c)(3) or 508(c)(1)(A) status is that the church becomes “tax exempt” as opposed to non-taxable; they place themselves under Internal Revenue Code Sections 501(c)(3) or 508(c)(1)(A), laws made by Congress (notice that the First Amendment says “Congress shall make no law respecting….”) and signed by the President. Before they do that, if they are not some type of legal entity such as a non-profit corporation, they are wholly protected by the First Amendment and are free to exercise their “religion” in conformity to New Testament principles.

Churches can make no profit if operated according to the principles of the New Testament. Without profit there are no taxes anyway. Even a business (something entirely different from a New Testament church but very like most American state churches) pays no taxes if it makes no profit. It is interesting that most American churches today are run like businesses, not like New Testament churches. That was another inevitable result of ordering a church according to the precepts of man, not those of God. Most are glorified social clubs or nightclubs. They are really businesses which pay no taxes because they call themselves churches and organize under state non-profit incorporation law.

What churches which become legal entities are really concerned about, since there is no need to worry about being taxed, is maximizing donations. They believed, after section 501(c)(3) was added to the Internal Revenue Code, that they would get more donations from people who were more concerned about getting a tax deduction than they were about glorifying God by honoring His precepts, from those whose motivation for giving was American “practicality” and not God’s pleasure. You see, God’s precepts often do not seem practical to most American believers. Churches cannot afford to operate the way they want without bringing in huge amounts of money and they cannot bring in that type of money through the tithes and offerings of born-again believers each of whom loves the Lord with all their heart, soul, mind, and strength because most of their members do not fit that description and would not tolerate teaching, preaching, and practice of all Bible doctrines. I explain all this and more in God Betrayed/Separation of Church and State: The Biblical Principles and the American Application and in other articles and teachings on the Separation of Church and State Law website-see Section VI of God Betrayed for a thorough study of the relevant law.

The inevitable results of proceeding without biblical knowledge, understanding, and wisdom are now coming to fruition, and the vast majority of American “Christians” are in panic mode. They fear man more than they fear God. It is a good thing for them to be in panic mode. Maybe some of them will, as a last resort, wake up and study the word of God, repent, and reorder their churches.

The June 2010 articlePreaching on Sodomy in a Hate Crime Atmosphereexplained what a both state churches (a church organized as a legal entity) and New Testament churches must do when they take issue with the civil government.

Endnote

I must mention that I believe that God has preserved his word in English. Since all English versions differ, and since there can only be one word of God, which English version is God’s word? One must answer this question or he has no Bible and no authority.

Notice that the above featured image, taken from IRS publications given below, says, “churches that meet the requirements of § 501(c)(3) are automatically considered tax exempt and are not required to apply for and obtain recognition of tax-exempt status from the IRS.” This is the correct position.

According to 508(c)(1)(A) a church can claim status without filing for 501(c)(3) status. 508(c)(1)(A) is a subsection of §508. Special rules with respect to section501(c)(3) organizations; this alone makes clear that a 508(c)(1)(A) church is a 501(c)(3) church. As such, it is subject to the requirements (the rules and regulations) that come with 501(c)(3). This conclusion is further explained in this article.

Furthermore, according to principles in the Word of God, church tax exempt status is spiritual fornication since she has submitted herself to man’s law, become a temporal legal – as opposed to spiritual eternal only – entity, and chosen to submit to an authority other than the Lord Jesus Christ as to many church matters.

A church can choose to remain under Christ only as a eternal spiritual organism as opposed to a temporal earthy organization. In America, the First Amendment and corresponding state constitutional provisions protect this choice from persecution. The essay below, and other essays, articles, and books on this website explain these matters more comprehensively.

Ignorance, and especially willful ignorance, is no excuse for dishonoring our Lord.

Click the above to go to online version of God Betrayed.

In the book God Betrayed/Separation of Church and State: The Biblical Principles and the American Application (“God Betrayed”) as well as in other books and writings, I originally taught that a New Testament church could depend upon Internal Revenue Code (“IRC”) § 508(c)(1)(A) for her non-taxable status (See Endnote 1for links to the two free versions of God Betrayed or for ordering information should you desire a softback copy as well as information on other books and resources by Jerald Finney.). I was wrong. After years of study, I have learned that a New Testament church cannot depend upon 508(c)(1)(A) for her non-taxable status because, in so doing, the church gives up her New Testament and First Amendment status; the church becomes tax exempt as opposed to non-taxable. However, I am more certain than ever of the correctness of my original biblically based conclusions that a church grieves the Lord when they intentionally, knowingly, recklessly, or negligently attain church corporate and/or 501(c)(3)/508(c)(1)(A) status or legal entity status (See Endnote 1) of any kind. I ask those who have followed my teachings to forgive me for misleading them concerning church 508 status. This brief article explains church 508 status and its effect.

A New Testament Church is also a First Amendment Church. This is because the First Amendment is a law which corresponds with biblical principles to include freedom of religion and conscience (separation of church and state), freedom of speech, freedom of press, and freedom of association. The First Amendment is a part of the second highest law of the land, the United States Constitution.

“Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the Government for a redress of grievances.”

Notice especially that the First Amendment says, “… no law ….”

Are not those words very clear? No law means “no law.” What is IRC § 508(c)(1)(A)? It, like IRC 501(c)(3), is a law made by Congress and signed by the President. IRC § 508(c)(1)(A) and IRC 501(c)(3) are, when applied to churches, laws “respecting an establishment of religion and preventing the free exercise thereof.”

Why would a church take themselves from First Amendment status and protection to either IRC § 508(c)(1)(A) or IRC § 501(c)(3)? One reason is lack of knowledge, wisdom, and understanding. When a church claims either 508(c)(1)(A) or 501(c)(3) status, she has rejected her First Amendment non-taxable status and freely accepted the offer of the federal government to enter into an agreement (contract) for tax exempt status as provided by a law.

Let me repeat: First Amendment churches under God are non-taxable. 501(c)(3) and 508(c)(1)(A) religious organizations are tax exempt. IRC § 508 (the codification of Public Law 91-172 ratified in 1969) provides in relevant part:

A portion of Internal Revenue Code § 508. Click the above to go to § 508.

“§ 508. Special rules with respect to section 501(c)(3) organizations. “(a) New organizations must notify secretary that they are applying for recognition of section 501(c)(3) status. … “(c) Exceptions. “(1) Mandatory exceptions. Subsections (a) and (b) shall not apply to— “(A) churches, their integrated auxiliaries, and conventions or associations of churches” (26 U.S.C. § 508). [Emphasis mine.]

§ 508(c)(1)(A) says churches are excepted from applying for IRC § 501(c)(3) tax exempt status (See Endnote 2for links to articles which fully explain church IRC § 501(c)(3)) status). 508 churches are an exception to the civil government requirement that certain organizations file for 501(c)(3) tax exempt status.

A church should rely on the First Amendment to the United States Constitution, not on508(c)(1)(A) status for three reasons. First, the First Amendment is a statement of the biblical principle of separation of church and state (See, for a short explanation with links to more in depth studies, Is Separation of Church and State Found in the Constitution?). When a church relies on the First Amendment, they are relying on a biblical principle. Should the biblical principle be abused or ignored by the civil government, so be it—a church should then rely and act only on the biblical principle. Endnote 3.

A law of man which enacts some biblical principles.

Second, to rely on 508(c)(1)(A) contradicts the First Amendment. To repeat, the First Amendment religion clause states:

“Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the Government for a redress of grievances.”

IRS Publication 1828. Click the above to go directly to IRS Pub. 1828.

Obviously, 508(C)(1)(A) is a law made by Congress which regards an establishment of religion; 508(C)(1)(A) also prevents the free exercise of religion because a church which claims 508(C)(1)(A) status thereby submits themselves to some control by the federal government in that the church becomes subject to the rules that come with IRC 501(c)(3) status. 508(C)(1)(A) does not state that the First Amendment forbids Congress from making any law in violation of the First Amendment; and that, therefore, a church is non-taxable. 508(C)(1)(A) is a law made by Congress which states that Congress, by law, is declaring an exemption for churches. Thus, by a clear reading of the First Amendment, 508(C)(1)(A) is clearly unconstitutional. Most churches and pastors could care less about this technicality.

From IRS Publication 1828

The correct position which is held by the Internal Revenue Service (“IRS”) is that a church has submitted herself to IRC § 501(c)(3) regulation and ignored her First Amendment status by relying on 508(C)(1) (a law passed by Congress) instead of the First Amendment. The IRS makes this position clear. Page 3 of IRS Publication 1828 states that “churches that meet the requirements of § 501(c)(3) are automatically considered tax exempt and are not required to apply for and obtain recognition of tax-exempt status from the IRS” [Bold red emphasis mine]. The IRS repeats this on page 24 of IRS Publication 557, “Tax –Exempt Status for Your Organization.” Under Organizations Not Required To File Form 1023 churches are listed. The following sentence is included: “These organizations are exempt automatically if they meet the requirements of section 501(c)(3).” [Bold red emphasis added.]

IRS Publication 557, p. 24. Click the image to go directly to the publication.

One should also understand that the New Testament (First Amendment) church will not be involved with the IRS for several reasons: the church claims no 501(c)(3) or 508(c)(1)(A) status; is not a legal entity such as a corporation aggregate or sole, an unincorporated association, or a charitable trust; is not a business; has no income; has no employees or staff; has no constitution or by-laws; and, no matter what the particular civil government does, honors the biblical principle of separation of church and state which is reflected in the First Amendment in America.

The New Testament (First Amendment) church who loves the Lord will be prepared for the eventuality that the Internal Revenue Service, some other Federal agency, the President (recent presidential actions and orders as well as the actions of many prior presidents demonstrate what a tyrannical president can and will do), and/or the Supreme Court of the United States may someday misinterpret and apply the First Amendment; and a New Testament church, who loves the Lord and is committed to pleasing Him, will remain submitted to the higher authority. God Betrayed (see above for free links to the book) explains all this and also shows how churches are operating in America without becoming legal entities such as incorporated 501(c)(3) religious organizations thereby retaining their First Amendment and biblical status. For specifics on how to organize a church under the Bible principle of separation of church and state, one can also go to: The CUCM Bible Trust.

Third, a New Testament church (a church organized according to the principles of the New Testament), among other things, receives no income, is not a 501(c)(3) or 508 religious organization, has no constitution or by-laws, has no employees or staff, and runs no businesses (daycare controlled or licensed by the state, “Christian” schools, “Bible” colleges, seminaries, cafes, etc.). Church members of a New Testament Church give their tithes and offerings to God, not to a religious organization, for use in ways consistent with New Testament teaching. All monies given to God are disbursed in accordance to the guidelines of the New Testament, and no money is left over. Let us use our common sense, if not our biblical sense: Even a business which makes no profit pays no taxes. A church which has no income cannot be taxed. A church which does have net income should be taxed since (1) she is operating as a business and not as a New Testament church; and (2) (if she is a legal entity such as a non-profit corporation (includes corporation sole – see Critique of “Church Freedom and the Corporation Sole” Website), or unincorporated association she is set up as a non-profit religious organization and therefore violates not only biblical principles for the organization of a church but also her non-profit agreements with the state of incorporation by making a profit.

Uncle Sam Wants God’s Churches

If a church does not apply for 501(c)(3) tax exempt status or claim 508(c)(1)(A) tax exempt status, and if she is organized as a New Testament church, according to the First Amendment which agrees with the biblical principle of separation of church and state, the non-taxable status of that church must be honored. A church claims 508(c)(1)(A) status by giving IRS acknowledgements for tithes, offerings, and gifts. No matter what the civil government claims, a church who has no income cannot be taxed; she gives her tithes, offerings, and gifts to God, not to a government created religious organization. Said another way, the church (the members) give to God, not to the church, inc. or the church (an unincorporated association).

Always keep in mind matters which I cover in detail in other writings and teachings: a church who incorporates (non-profit corporation or corporation sole), or becomes a charitable trust, unincorporated association or some other type legal entity has voluntarily given up her exclusive First Amendment status in favor of partial and substantial Fourteenth Amendment status since she has become a legal entity.

There are other ways a church may violate biblical principles concerning the doctrine of the church thereby becoming some type church other than a New Testament church. Understanding these matters requires a believer to grow in knowledge, understanding, and wisdom through dedicated Bible study.

If a church successfully applies for 501(c)(3) status or claims 508(c)(1)(A) exempt status, the government is granted some jurisdiction over the church since the civil government now, by law, declares and grants an exemption.

Please, God’s dear churches, do not lose your New Testament status by becoming a legal entity of any kind. Please learn to love the Lord as he loves you and gave Himself for you;

“That he might sanctify and cleanse it with the washing of water by the word. That he might present it to himself a glorious church, not having spot or wrinkle, or any such thing; but that it should be holy and without blemish” (Ephesians 5.25-27).

Please, dear believer, learn to think Biblically (spiritually), not practically from the human perspective (fleshly). Please become more Christian than American, more heavenly than earthly. God made clear that Christ in heaven is to be the only authority (power or head) “over all things to” His churches. Put another way, a church, the body whose feet walk and work on earth, is to be connected to only one head, Christ in heaven. A church with two heads (authorities or powers) is a monstrosity.

“And what is the exceeding greatness of his power to us-ward who believe, according to the working of his mighty power, Which he wrought in Christ, when he raised him from the dead, and set him at his own right hand in the heavenly places, Far above all principality, and power, and might, and dominion, and every name that is named, not only in this world, but also in that which is to come: And hath put all things under his feet, and gave him to be the head over all things to the church, Which is his body, the fulness of him that filleth all in all” (Ep. 1.19-23).

“Now therefore ye are no more strangers and foreigners, but fellowcitizens with the saints, and of the household of God; And are built upon the foundation of the apostles and prophets, Jesus Christ himself being the chief corner stone; In whom all the building fitly framed together groweth unto an holy temple in the Lord: In whom ye also are builded together for an habitation of God through the Spirit” (Ep. 2.19-23).

“And he is the head of the body, the church: who is the beginning, the firstborn from the dead; that in all things he might have the preeminence” (Col. 1.18).

From the above verses, and many more that could be quoted, one sees that God desires his churches to be spiritual entities or bodies (See also, e.g., Ep. 4 and the whole book of Ep., Col., and 1 Co. 12 for more on churches as spiritual bodies) connected to their only God ordained Head, the Lord Jesus Christ in heaven, while walking as spiritual entities only here on the earth. Churches are to be “builded together for an habitation of God through the Spirit,” not built together as a corporate 501(c)(3) or 508 organization according to man’s earthly, legal laws.

Please repent and turn from the deceits of the god of this world to the precepts of God. Please prepare for the day when believers and churches will have to choose either to lay it all down for God and for eternal reward or to lay it all up for Satan for a perceived earthly security. That day has not yet arrived for believers and churches in America, but that day appears to be fast approaching.

Endnotes

1. For the definition of and more information on “legal entity” see the index of God Betrayed/Separation of Church and State:The Biblical Principles and the American Applicationwhich is available free in PDF, in online form (no index), or which may be ordered by clicking Order information for books by Jerald Finney.

All books, except An Abridged History of the First Amendment, by Jerald Finney are available free in both PDF and online form. One may go to Order information for books by Jerald Finney should he desire to order any of the books which are in print.

Click here to go to the article “Is Separation of Church and State Found in the Constitution?”

A biblical and historical Baptist principle is that God desires separation of church and state, not separation of God and church or separation of God and state. Study Jerald Finney’s writings and/or audio teachings to discover the truth about and how to apply the principle. Finney’s teachings prove that the revisionist view of Separation of Church and State accepted without examination by most American “Christians” is false and has done great damage to the cause of Christ and to America.

The local church sanctified and cleansed by the washing of water by the word——————–A ministry of Charity Baptist Tabernacle of Amarillo, Texas led by Pastor Ben Hickam. "Would to God ye could bear with me a little in my folly: and indeed bear with me. For I am jealous over you with godly jealousy: for I have espoused you to one husband, that I may present you as a chaste virgin to Christ. But I fear, lest by any means, as the serpent beguiled Eve through his subtilty, so your minds should be corrupted from the simplicity that is in Christ" (2 Corinthians 11:1-3). ————————————Jerald Finney, a Christian Lawyer and member of Charity Baptist Tabernacle, having received this ministry in the Lord, explains how a church in America can remain under the Lord Jesus Christ and Him only. "As every man hath received the gift, even so minister the same one to another, as good stewards of the manifold grace of God. If any man speak, let him speak as the oracles of God; if any man minister, let him do it as of the ability which God giveth: that God in all things may be glorified through Jesus Christ, to whom be praise and dominion for ever and ever. Amen" (1 Peter 4:10-11; See also, Ephesians 4::1-16 and 1 Corinthians 12:1-25). "Take heed to the ministry which thou hast received in the Lord, that thou fulfil it" (Colossians 4:17). "And hath put all things under his feet, and gave him to be the head over all things to the church" (Ephesians 1.22; See also, e.g. Colossians 1:18).