Lecture entitled “Hierarchy of Law” by Attorney Jerald Finney on August 26, 2012.

Principles and Application for Organizing

A Church God’s Way

Organizing a Church According to God’s Word:

Common Law Versus Statutory Law Considerations

Case Notes

Jerald Finney, the author of this page is a licensed and actively practicing Christian lawyer who is neither going to dishonor God nor jeopardize his law license by lying to anyone.

These case notes deal with issues important in church organization (incorporation, trust, property tax exemption, 501(c)(3) and 508 tax exemption, etc.). These matters should be important to churches who wish to remain non-legal entities in accordance with New Testament Doctrine. There is a lot of misinformation being spread by pseudo-lawyers and self-proclaimed legal analysts, paralegals, etc. concerning church organization.

These notes are from actual cases and laws on the books. Anyone can look up the cases and law on a legal website or in a law library and verify that they are not being lied to. Almost all laws from city to national level are now available on websites – just google the jurisdiction and law you want to look at. Almost all law libraries in the United States now have free computer access to legal websites such as Westlaw and/or Lexis. So the case materials are not the opinions of the author, but those of the courts.

No case is cited, nor can any case be found, that states that a church must obtain corporate, 501(c)(3) status to qualify for property tax exemption; such a requirement would violate the First Amendment to the United States Constitution and corresponding state constitutional provisions. Some of the cases and other legal materials below clearly show that property tax exemption is afforded to a “church,” or “religious society” which uses “trust” organization and which otherwise meets the requirements for property tax exemption.

A local property tax board denied the religious property tax exemption on property owned by the Lord Jesus Christ and held in trust for use by a church. The trustee of the trust filed a petition in court, his only recourse. Read about this case at: Another Victory for a Church under Christ (092419). See the substance of the brief drafted by Jerald Finney and filed in that case by clicking here.

Contents:

I. Actual cases involving churches established by the Biblical Law Center (replaced by the Churches under Christ Ministry). These cases were successfully resolved in favor of the property tax exemption.

II. Some resources to help in understanding the different types of church organization.

III. Link to Powerpoint on “Trusts.”

IV. Important cases with comments concerning church use of trusts, the validity of those trusts, church incorporation, state requirements for church organization when property tax exemption is sought, and other related matters.

V. Cases dealing with “Organizations which created religious scams in order to obtain Property Tax Exemption.”

VI. Types of organizations which qualify as a “religious organization” for property tax exemption purposes. E. g., “Does an organization which has no reverecne for a deity qualify?”

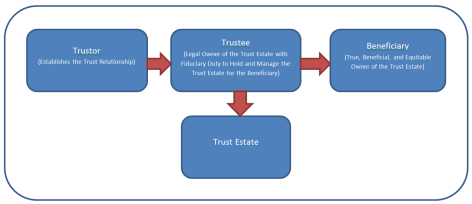

I. Actual cases involving churches who established a trust relationship with real and personal property (personal property includes money and bank accounts) whereby a trustee holds and manages property owned by the Lord Jesus Christ for the benefit of the Lord Jesus only.

a. A local property tax board denied the religious property tax exemption on property owned by the Lord Jesus Christ and held in trust for use by a church. The trustee of the trust filed a petition in court, his only recourse. Read about this case at: Another Victory for a Church under Christ (092419). See the substance of the brief drafted by Jerald Finney and filed in that case by clicking here. In Minnesota, there is no agency process. If the local assessor denies the exemption and the issue cannot be resolved, the only recourse is court action.

b. Indiana law provides an agency process for property tax disputes. Trinity Springs Baptist Church had executed a Declaration of Trust in accordance with the First Amendment to the United States Constitution and corresponding Indiana Constitutional provisions. The county tax board had honored the tax exemption on the real property held in the trust estate for some years. However, in 2013 the local property tax board denied the exemption. The trustee handled the case with the help of the Biblical Law Center. Read the details, as well as the decision of the Indiana Board of Tax Revies at: The Indiana Board of Tax Review Determines that Property Held in Trust for the Lord Jesus Christ Must Be Granted Property Tax Exemption

II. For a good overall understanding of church incorporation and 501(c)(3) and 508 status see Separation of Church and State/God’s Churches: Spiritual or Legal Entities? Chapter 7 of that book explains more about the use and definition of the “trust.” For links to more resources which explain “trust,” go to Trust Explained: Resources.

III. Powerpoint: The Basics of the Bible Principle of Trust in Church Organization Explanation of “Trust,” as opposed to “Business Trust,” “Charitable Trust,” and other kinds of trusts. How can you know who to trust for the truth about these matters? How can you know if what is presented here is the truth? Etc. Note. When you click the link, the Powerpolint should be downloaded to your Computer.

IV. Important cases with comments concerning church use of trusts, the validity of those trusts, church incorporation, state requirements for church organization when property tax exemption is sought, and other related matters.

Please notice: Some of the cases below are linked to more thorough analyses.

A. Another Victory for a Church under Christ (092419) A local property tax board in Minnesota denied the property tax exemption for real estate used as a meeting house for a church which had established a trust relationship with property. The property was used 100% for church purposes. The only recourse, after trying to reason with the local assessor and county attorney, was for the trustee to file petition in court. The trustee prevailed, after filing of Motion/brief and oral argument, and without trial. The property tax exemption was granted. The redacted Motion/brief is linked to for one to examine.

B. The Indiana Board of Tax Review Determines that Property Held in Trust for the Lord Jesus Christ Must Be Granted Property Tax Exemption (012319). This article involves a property tax exemption for a Trinity Baptist Springs Church in Trinity Baptist Springs, Indiana organized under a Declaration of Trust. The Pastor, with the help of the Biblical Law Center, represented himself. The article links to the video of the property tax hearing held by the local property tax board who decided against the exemption. The case was appealed to the Indiana Board of Tax Review who reversed and order that the tax exemption be granted.

Indiana property tax exemption law specifically recognizes the trust relationship. Indiana Code Title 6. Taxation § 6-1.1-10-21states:

Sec. 21 . (a) The following tangible property is exempt from property taxation if it is owned by, or held in trust for the use of, a church or religious society:

(1) A building that is used for religious worship.

(2) The pews and furniture contained within a building that is used for religious worship.

(3) The tract of land upon which a building that is used for religious worship is situated.

(b) The following tangible property is exempt from property taxation if it is owned by, or held in trust for the use of, a church or religious society:

(1) A building that is used as a parsonage.

(2) The tract of land, not exceeding fifteen (15) acres, upon which a building that is used as a parsonage is situated.

(c) To obtain an exemption for parsonages, a church or religious society must provide the county assessor with an affidavit at the time the church or religious society applies for the exemptions. The affidavit must state that:

(1) all parsonages are being used to house one (1) of the church’s or religious society’s rabbis, priests, preachers, ministers, or pastors; and

(2) none of the parsonages are being used to make a profit.

The affidavit shall be signed under oath by the church’s or religious society’s head rabbi, priest, preacher, minister, or pastor.

(d) Property referred to in this section shall be assessed to the extent required under IC 6-1.1-11-9

- “A valid trust need not be in writing. It can be created orally unless the language of the written conveyance excludes the existence of a trust. Sanderson v. Milligan,585 S.W.2d 573, 574 (Tenn. 1979); Linder v. Little, 490 S.W.2d 717, 723 (Tenn. Ct. App. 1972); and Adrian v. Brown, 29 Tenn. App. 236, 243, 196 S.W.2d 118, 121 (1946). However, when a party seeks to establish an oral trust, it must do so by greater than a preponderance of the evidence. Sanderson v. Milligan, 585 S.W.2d 573, 574 (Tenn. 1979); Hunt v. Hunt, 169 Tenn. 1, 9, 80 S.W.2d 666, 669 (1935); and Browder v. Hite, 602 S.W.2d 489, 493 (Tenn. Ct. App. 1980).

- “The existence of a trust requires proof of three elements: (1) a trustee who holds trust property and who is subject to the equitable duties to deal with it for the benefit of another, (2) a beneficiary to whom the trustee owes the equitable duties to deal with the trust property for his benefit, and (3) identifiable trust property. See G.G. Bogert & G.T. Bogert, The Law of Trusts and Trustees § 1, at 6 (rev. 2d ed. 1984) and Restatement (Second) of Trusts § 2 comment h (1957). We find that the Kopsombut-Myint Buddhist Center has proved the existence of each of these elements by clear and convincing evidence.” [p. 333].

The Wisconsin Supreme Court stated, in its opinion from which the above was taken that:

- The court of appeals had no obligation to look beyond the issues raised by Bible Baptist, but had the discretion to do so. The “church” was organized as a trust. The principle issue which it in its discretion addressed was the circuit court’s conclusion that for a ‘church’ to claim a tax exemption, it must be incorporated under the laws of Wisconsin or another state. The Supreme Court of Wisconsin agreed with the conclusion of the appeals court that the church need not be incorporated to claim a tax exemption.The Court stated: “We need not reiterate the excellent discussion and analysis underpinning that conclusion that appears in the court of appeals opinion. 157 Wis. 2d at 539-49” [the citation for this case].

The opinion from the court of appeals referred to by the Wisconsin Supreme Court was WAUSHARA COUNTY v. Sherri L. GRAF, 157 Wis.2d 539 (1990), 461 N.W.2d 143, Court of Appeals of Wisconsin. Submitted on briefs December 8, 1989. Decided August 2, 1990. Here are some very important points made on pp. 539-49 of that decision:

We hold … that the church was not required to show that it was incorporated as a religious society or corporation under ch. 187, Stats., or otherwise, to establish that its property is exempt from taxation under sec. 70.11(4).

The court examined the legislative history of the pertinent statutes to determine if a church or religious organization must be incorporated for its property to be tax exempt [under state law]. The court started with examination of the first exemption from taxation of the property of churches and religious organizations—in sec. 24, ch. 47, Revised Statutes of 1849. Chapter 47 prescribed the procedure by which persons belonging to a church congregation or religious society, “not already incorporated,” could incorporate. … The exemption was not limited to religious societies incorporated under ch. 47.

The court then looked at Chapter 130, Laws of 1868 which provided for the assessment of property for taxation and for exemptions therefrom. Section 2, 3d exempted “[p]ersonal property owned by any religious, scientific, literary or benevolent association, used exclusively for the purposes of such association, and the real property necessary for the location and convenience of the buildings of such association . . . not exceeding ten acres. . . .” Chapter 130 did not define “association.” The court then went to Wisconsin Statutes of 1898. Section 1038, subd. 3 was renumbered sec. 70.11(4), Stats., by sec. 16, ch. 69, Laws of 1921. Throughout its history, the exemption from taxation of property of churches and religious associations has been accorded in substantially the same language. No “linkage” has existed between the exemption statutes and those affecting the organization of churches and religious associations or societies.

Chapter 411, Laws of 1876, provided for the incorporation of religious societies. Apparently this act replaced ch. 47 of the revised statutes of 1849. Chapter 411 is silent as to the taxation or exemption of the property of religious societies incorporated thereunder.

The procedures for the incorporation of religious societies were included in ch. 91, Revised Statutes of 1878. Nash’s Wisconsin Annotations (1914), sec. 1990, ch. 91 at 753, states:

The revisers of 1878 in their note said: “Chapter 411, 1876, is taken to have been intended as a revision of the law for the incorporation of religious societies. The privilege of organizing a corporation is extended to all classes and denominations, it not being supposed the law means to be intolerant of any religious belief or to be partial in its offer of privileges.”

The same annotation at page 755 states:

“Church” and “Congregation.” A church consists of those who are communicants, have made a public profession of religion and are united by a religious bond of common spiritual welfare. It is the spiritual body, not the legal one. But a religious society or congregation, under the statute, is a voluntary association of persons, generally but not necessarily in connection with a church proper, united for the purpose of having a common place of worship and to provide a proper teacher to instruct them in doctrines and duties, etc. [Citations omitted.]

Decisions interpreting ch. 91, Revised Statutes of 1878, make plain that failure of a church or religious organization to incorporate thereunder did not affect the power of the church or religious organization to hold title to property. “Under the repeated decisions of this court, we must hold that the mere fact that [a] church or religious society had not yet been incorporated at the time of the delivery of [a] deed in no way frustrated the trust thereby created, if such trust was otherwise valid.” Fadness v. Braunborg, 73 Wis. 257, 278-79, 41 N.W. 84, 90 (1889) (emphasis in original).

In Holm v. Holm, 81 Wis. 374, 382, 51 N.W. 579, 581 (1892), the facts included that the Norwegian Evangelical Lutheran Church of Roche-a-Cree was a voluntary association until February 7, 1889. The court noted that “[p]rior to that date the title to the churches in which the members of the association worshiped was vested in trustees named in . . . deeds, and their successors in office. . . . The trusts imposed by such deeds appear to have been valid upon the principles stated by this court in Fadness v. Braunborg. . . .” Id.

In Franke v. Mann, 106 Wis. 118, 131, 81 N.W. 1014, 1018-19 (1900), the court further said that “[w]hat has been said is in harmony with the law regarding trusts for religious uses, whether the trustees be officers of a religious corporation or of an unincorporated ecclesiastical body. . . .” Id. at 131-32, 81 N.W. at 1019 (emphasis added).

It is plain from these decisions that the court did not consider that the legislature, by offering to ecclesiastical bodies the advantages of incorporation, intended to impose corporate structure upon such bodies. The property of unincorporated ecclesiastical bodies was commonly held in trust for the benefit of the members.

The Basic Bible Church established that title to the real estate subject to foreclosure was held in the name of the trustees for the benefit of the church. We conclude that the trust constituted an “entity” which could claim tax exemption under sec. 70.11(4), Stats., for the benefit of the Basic Bible Church. We further conclude that the legislative history of the pertinent statutes does not disclose a legislative intent to require that a church or religious association be incorporated before it may claim tax exemption under sec. 70.11(4).

V. Organizations which created religious scams in order to obtain Property Tax Exemption.

A. In almost all cases, such scams were organized as 501(c)(3) non-profit corporations. Some examples:

Ideal Life Church of Lake Elmo v. Washington County, 1981, 304 N.W.2d 308 (Supreme Court of Minnesota)(Click link to go to the entire case online). Purported religious organization which was organized and operated primarily for motive of tax avoidance by private individuals in control of 501(c)(3) corporation, had no formally trained or ordained ministry, had no sacraments, rituals, education classes or literature of its own, had no liturgy other than simple meetings resembling mere social gatherings or discussion groups and did not require a belief in any supreme being or other being, and whose doctrine and beliefs were intentionally vague and nonbinding upon its members and whose members freely continued to practice other religions, was not a “church” as such term was used in state’s tax exemption laws.

In re Collection of Delinquent Real Property Taxes, State of MN v. American Fundamentalist Church, 1995, 530 N.W.2d 200 (S.Ct. Minnesota) rehearing denied (Click link to go to entire case online). Threshold question in determining whether real property is “church” entitled to tax exemption is whether entity claiming exemption is “church” within meaning of statute…. The organization in this case was an incorporated 501(c)(3) church. Test for determining whether organization is “church” entitled to tax exemption is subjective one, focusing on sincerity of belief and taking into account evidence on objective issues. … Principal motivation for organizing religious corporation was tax minimization and therefore, organization was not “church” and, therefore was not entitled to real property tax exemption in view of evidence that most of financial contributions to organization came from individual founder, that most of founder’s income came from taxpayer, that founder was primary beneficiary of organization’s financial actions, and that founder and his wife, who was co-founder, dominated meetings of organization’s board of trustees.

VI. Types of organizations which qualify as a “religious organization” for property tax exemption purposes? E. g., “Does and organization which has no reverence for a deity qualify?”

–