A Publication of Churches Under Christ Ministry

Follow-up article published on December 9, 2025:

Have They Gotten Rid of the “Johnson Amendment,

as President Trump Promised?

Click here to go to All Written Course Segments

Click here to go to General Questions Answered

Click here To Go to Links to All 5 Minute Youtube Course Segments

Jerald Finney

Copyright © December 2, 2017

Speech by President Trump: We are giving our churches their voices back

President Trump, desiring to help churches and “Christians,” and according to the advice of those “Christians” and other religious leaders who surround him, pledged to eliminate the Johnson Amendment which limits all nonprofits from endorsing and opposing political candidates. See Endnote 1 for links to articles on this matter. I believe he is sincerely trying to help churches. Accordingly, he signed an executive order easing restrictions on political activity by non-profits. Of course, he cannot unilaterally change the law; but he did all he could do to help – ease but not eliminate one of the five restrictions which come with 501(c)(3) status. Just as non-profit corporation status puts the state of incorporation over a church for many matters, 501(c)(3), a man made law, still puts the federal government and the IRS agency over churches with respect to certain rules and a multitude of regulations that come with the chosen 501(c)(3) status. See Endnote 2 for list of some of the regulations that come with 501(c)(3) and links to resources which explain 501(c)(3) and 508(c)(1)(A) tax exempt status in some detail.

President Trump, desiring to help churches and “Christians,” and according to the advice of those “Christians” and other religious leaders who surround him, pledged to eliminate the Johnson Amendment which limits all nonprofits from endorsing and opposing political candidates. See Endnote 1 for links to articles on this matter. I believe he is sincerely trying to help churches. Accordingly, he signed an executive order easing restrictions on political activity by non-profits. Of course, he cannot unilaterally change the law; but he did all he could do to help – ease but not eliminate one of the five restrictions which come with 501(c)(3) status. Just as non-profit corporation status puts the state of incorporation over a church for many matters, 501(c)(3), a man made law, still puts the federal government and the IRS agency over churches with respect to certain rules and a multitude of regulations that come with the chosen 501(c)(3) status. See Endnote 2 for list of some of the regulations that come with 501(c)(3) and links to resources which explain 501(c)(3) and 508(c)(1)(A) tax exempt status in some detail.

Does this action by the President correct the problem with 501(c)(3)? No. I explain why in this article.

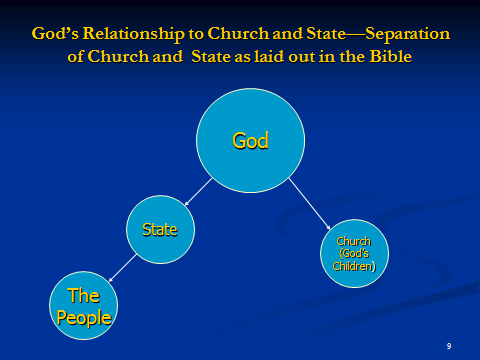

One should be aware that the highest man made law in America, the First Amendment to the United States Constitution, and corresponding state constitutional provisions make clear that churches have a choice – remain under Christ only or submit to the state and federal governments through corporate 501(c)(3) status.

Keep in mind, for example:

- Matthew 16:18 “And I say also unto thee, That thou art Peter, and upon this rock I will build my church; and the gates of hell shall not prevail against it.” Is a church built partially or wholly by man (man’s law) a church of Christ? Is such a church His church?

- Ephesians 1:22 “And hath put all things under his feet, and gave him to be the head over all things to the church.” Is Christ the head over all things to an incorporated 501(c)(3) or 508 church? The simple to comprehend answer is an emphatic, “No!”

- Colossians 1:18 “And he is the head of the body, the church: who is the beginning, the firstborn from the dead; that in all things he might have the preeminence.”

Let us first briefly examine or look at what church 501(c)(3) status really is. This will highlight the real issue. We will have to touch on incorporation since the two are intertwined.

Most churches choose to apply for both corporate and 501(c)(3) or 508(c)(1)(A) tax exempt status even though a choice not to do so is protected by the First Amendment and corresponding state constitutional provisions. 508(c)(1)(A) status puts a church in the same position as 501(c)(3) status. See, Church Internal Revenue Code § 508 Tax Exempt Status. Churches who incorporate and/or get 501(c)(3) or 508(c)(1)(A) status are established churches. They combine with civil government under man-made law. They get some perceived “benefits” and powers from civil government. In return, they agree to abide by the non-profit corporation laws of the state of incorporation and the commandments which come with the federal 501(c)(3) law they sought and agreed to. They also agree that, in the event they have issue with a commandment imposed by the law, the authority who will decide the issue is the government through its court systems. Their authority for many matters is the civil government, not the Lord Jesus Christ. One might call those churches who constantly defy and complain about the rules or commandments they agreed to “hypocrites.”

Churches who seek and obtain 501(c)(3) agree to abide by the rules and regulations that come with 501(c)(3), and also to any future rules added by the federal government though legislation, or by the Internal Revenue Service and upheld by the courts. Maybe some do not realize what they are doing when they get such status; some may proceed without knowledge, understanding, and wisdom. Nonetheless, when they get the status, they agree to the rules and commandments which come with the status and they agree that, in the event their authority who will decide the issue is the first the agency process with appeal to federal court available to the losing side, not the Word of God. Corporate 501(c)(3) churches proudly proclaim victory when their authority rules in favor of their position and moan and groan when their authority decides against them. They cannot understand that they lost no matter what their authority decides because they have put themselves under the wrong authority, according to the Word of God; and even their so-called victories are riddled with compromise.

Originally, a church who chose 501(c)(3) status agreed to 4 commandments or rules, added by legislative law. The IRS added a fifth. Prior to Bob Jones University v. United States, 461 U.S. 574 (1983), there were four rules. Bob Jones University upheld the IRS “shall not violate fundamental public policy” rule. Now there are five commandments. The fifth one has not yet been applied, as far as I know, to a church. However, many pastors do not preach of certain matters because they fear that they will be in violation of that rule—they do not wish to offend their master, their authority, by preaching certain matters covered by the Word of God. Many pastors openly preach on prohibited matters knowing that the state may exercise their authority and command them to comply or lose their status and suffer other penalty imposed by their master. The only authority to which a church can appeal, should the IRS agency rule against them, is the civil court system. By the way, the court will not allow such a church to make Bible based arguments.

As one can see, corporate 501(c)(3) status comes with the loss of many of the church’s First Amendment rights. A corporate 501(c)(3) church is a “legal entity,” an artificial person who has placed herself under the Fourteenth Amendment for many purposes thereby giving up much of her First Amendment protection. A First Amendment church cannot be sued for violation of the rules that come with 501(c)(3) or 508(c)(1)(A) because such a church has not submitted herself to the Internal Revenue Code Section 501(c)(3) or Section 508(c)(1)(A). She cannot be forced to get such status because the First Amendment religion clause says, “Congress shall make no law respecting the establishment of religion or prohibiting the free exercise thereof.”

A 501(c)(3) church also agrees to many regulations. See Endnote 2 for list of some of the regulations that come with 501(c)(3) and links to resources which explain 501(c)(3) and 508(c)(1)(A) tax exempt status in some detail.

One who does just a little study can easily understand that the governments of the state of incorporation and the federal government are the authorities, for many purposes, of a corporate 501(c)(3) church. The Lord Jesus Christ is, at most, only one of their authorities or heads. For many churches, Christ is completely eliminated from the equation and their sole authority is civil government. Churches grieve our Lord by submitting to another head. Christ is not over “over all things to” those churches. According to the Bible, this raises a very important question, “Are corporate 501(c)(3) churches of Christ, built by Christ and Him alone?” They are churches, but are they Christ’s churches? The answer is obvious.

So the main issue is one of authority. Looking beyond that, only the legislature, not the President, can eliminate the Johnson Amendment or any other rule that comes with 501(c)(3) status. It is a law, passed by Congress and signed by the President. The President, of course, is the law enforcer. Like any law enforcer, he can choose to ease or relax his efforts to enforce what he deems to be an unjust law, you might say. He cannot do away with the fact that the authority of the 501(c)(3) church, as to the rules that come with it, is the federal government through its agent, the IRS. The courts, not the President, decide unresolved clashes between 501(c)(3) churches and the IRS. Only the legislature, not the President, can repeal a law subject to his signature of approval. The legislature has taken no action to overrule the Johnson Amendment in the many months since President Trump filed his executive order nor has President Trump encouraged the legislature to do away with either 501(c)(3) status or any of the other rules that come with 501(c)(3).

Even should the Johnson Amendment be eliminated by legislative law signed by the President, there would still be four other rules that churches agreed to comply with when they chose to apply for 501(c)(3) tax exemption. It is no secret that churches and so called “Christian” lawyers have also been worried about rule number five, the fundamental public policy rule, for at least 15 or 20 years. Their advice: “pray about it.” I would like to hear one of their prayers. I do not think they will pray, “Lord, forgive us for dishonoring you and causing you much grief by prostituting your churches. We repent. Help us to honorably withdraw from our unholy alliances.”

I have touched on the main issue. Let me restate some of the above points and list some other matters. President Trump’s speeches and his executive order reflect Christian revisionist history. They:

- ignore the fact that churches are required to give up some of their First Amendment protections when they choose to become 501(c)(3) organizations who submit to the federal government as to certain matters;

- ignore the fact that churches voluntarily put themselves under 501(c)(3) with all the rules and regulations that accompany their choice ;

- ignore the fact that churches voluntarily give up much of their First Amendment protection when they place themselves under a law which commands them not to do certain things;

- ignore the fact that churches who incorporate and get 501(c)(3) status put themselves, for many purposes, under the Fourteenth Amendment;

- do not take into account that 501(c)(3) was a law implemented in 1954, 164 plus years after the adoption of the First Amendment;

- ignore the question of whether 501(c)(3) is even constitutional since the First Amendment religion clause says, “Congress shall make no law respecting an establishment of religion or preventing the free exercise thereof;”

- reflect a lack of understanding of the true history of the First Amendment;

- reflect the “Christian” revised history of the First Amendment;

- misrepresent what church/state establishment meant when the Constitution and First Amendment were adopted;

- misrepresent what Thomas Jefferson, for example, stood for (He stood for a secular state with complete separation of church and state); (See, Endnote 3 for links to an unrevised history of the First Amendment)

- disregard and go contrary to Bible principles concerning church, state, and the relationship God desires between church and state;

- ignorantly work for the end-time one world union of church and state under the beast;

- etc.

I wish to make one other point: I believe that freeing 501(c)(3) non-profit organizations to become active in politics will unleash liberal 501(c(3) organizations–atheist, secular, and religious–who will fight for liberal candidates, and that those organizations substantially outnumber and have much more money and power than the conservative churches who constantly attack the rule. Those liberal organizations include Planned Parenthood, Inc. (an organization that gets a lot of government money), the Church of Wicca, Inc. and many many other incorporated 501(c)(3) organizations and churches who will support liberal candidates.

In conclusion, I believe that President Trump is sincerely trying to help the cause of religious liberty. But he is being misled by certain religious persons and organizations who will use any means necessary to achieve their goals. Their false Biblical interpretations and goals hasten fulfillment of end time prophecies—religion and government will unify and bring in a 3 ½ year of peace followed by 3 ½ year period of great tribulation, and finally the appearance of our Lord who will crush the world powers who are coming against Israel and then establish His 1000 year reign on the earth.

Endnotes

Endnote 1: Links to some articles: Trump Vow: ‘Totally Destroy’ 501(c)(3) Political Activity Ban, February 3, 2017. President Trump vowed to He signed an executive order easing restrictions on religious participation in politics. See Trump signs executive order to ease restrictions on religious participation in politics, May 4, 2017. TRUMP RELAXES 501(C)(3) POLITICAL ACTIVITY RULES, May 5, 2017.

Endnote 2: 501(c)(3) and 508(c)(1)(A) tax exempt status not only come with five government imposed rules, such status also invokes a myriad of regulations. See, e.g., Publication 557 (01/2019), Tax-Exempt Status for Your Organization; Application for Recognition of Exemption; Exempt Organizations Treasury Regulations; Charities and Nonprofits A-Z Site Index (F-J); Exempt Organization Revenue Rulings; Pub. 1828, Tax Guide for Churches and Religious Organizations (PDF); Common Tax Law Restrictions on Activities of Exempt Organizations; Exempt Organizations – Ruling and Determinations Lettersr; Exempt Organizations – Private Letter Rulings and Determination Letters; Exempt Organizations Announcements; Annual Filing Requirements for Supporting Organizations; Exempt Organizations Notices; Public Disclosure and Availability of Exempt Organizations Returns: Copies of Exempt Organizations Tax Documents; Exempt Organization Revenue Procedures; Exempt Organizations Update; Exempt Organizations – Employment Taxes; The Truth About Frivolous Tax Arguments – Section II; Termination of Exempt Organization (“… Internal Revenue Code Section 6043(b) and Treasury Regulations Section 1.6043-3 establish rules for when a tax-exempt organization must notify the IRS that it has undergone a liquidation, dissolution, termination, or substantial contraction. Generally, most organizations must notify the IRS when they terminate. Among other things, notice to the IRS of a termination will close the organization’s account in IRS records. …).

See also, for analysis of 501(c)(3) and 508(c)(1)(A): (1) Questionnaire 2, I. Elementary Questions for Those Who Wish to Organize a Church under Christ Alone as opposed to either a Church under Man or a Church under Christ and Man, (2) Federal government control of churches through 501(c)(3) tax exemption; (3) The church incorporation-501(c)(3) control scheme.

Endnote 3: The History of the First Amendment; An Abridged History of the First Amendment; List of Scholarly Resources Which Explain and Comprehensively Document the True History of Religious Freedom in America.

Additionally, by mixing church and state, churches opened the door to the untenable situation where an earthly temporal civil government which has neither the authority nor the ability to understand spiritual matters is granted power over the church and put in charge of defining “church,” “religious organization,” “religious society,” etc. This mixing of the holy with the unholy has resulted in the inevitable consequences we see shaping up as a result of civil government definition of “church.”

Additionally, by mixing church and state, churches opened the door to the untenable situation where an earthly temporal civil government which has neither the authority nor the ability to understand spiritual matters is granted power over the church and put in charge of defining “church,” “religious organization,” “religious society,” etc. This mixing of the holy with the unholy has resulted in the inevitable consequences we see shaping up as a result of civil government definition of “church.”